After a market correction is over, don’t be too quick to sell the stocks that rally first and show the strongest relative strength.

That is not always “risk management.”

In many cases, it actually increases the risk of missing a potentially massive winner.

Even today, I still make this mistake sometimes.

Why?

Because the stocks that recover first after a correction are often not just random bounce plays.

They are usually the names where money is flowing back first.

They show relative strength before the crowd fully realizes the market has turned.

They may be the next leaders of the new uptrend.

Real risk management is not selling a strong stock simply because it has gone up.

Real risk management is managing position size, knowing your invalidation level, and watching whether the price action actually breaks down.

If a stock remains strong, money is still flowing in, and the fundamentals and narrative are still intact, selling too early can actually be poor risk management.

So the key is not “never sell.”

The key is:

Don’t sell the strongest market leaders too easily just because you are afraid of giving back existing profits.

Many times, what truly changes your trading return curve is not taking small profits again and again.

It is whether you can sit through the right leaders long enough during a real market uptrend.

I can't believe people do not know you can build hedge fund level trading strategies using AI completely from scratch.

This paper shows exactly how top quants combine AI with real market data to build strategies that actually prints. Bookmark this before someone takes it down.

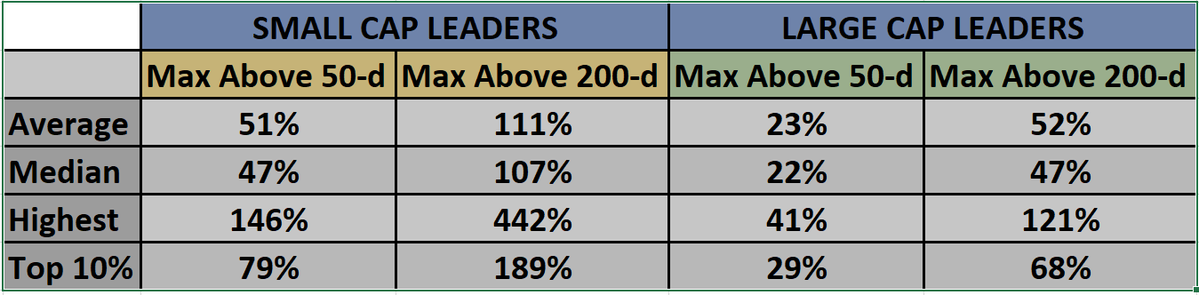

Have shares these stats @dennisc230 gave me years ago....maybe a little outdated without exact parameters but have always found the top 10% zone to be helpful....Bracco good info below

The secret of Hedge Funds is revealed in 21 page PDF.

Two Sigma & Citadel run billions through ARIMA & GARCH time series models everyday. A researcher just released complete framework behind how it works for free.

Bookmark & read the article below before someone takes it down.

This 9-minute lecture by Nassim Taleb on "Probability Distribution" will teach you more about prediction trading than 2 months as a Quant intern at Jane Street.

Bookmark it & give it 9-minutes today. It’ll be the most productive start for your week. Then read article below.

Two Sigma pays $450K/year for a quantitative researcher.

This 1-hour workshop by a two-sigma AI engineer will show you how they use deep learning in quant trading.

Bookmark it & give it 1 hour today. It will change the way you build trading systems. Then read post below.

QUANT BIBLE - MIT Sloan Business Club... Okay, if you want to mistake quant interview prep for becoming a quant, this is your "holy grail" 😬

Link in the comments 👇👇

You've heard of 101 Dalmatians but have you heard of 151 Trading Strategies? https://t.co/3BVCH24eIZ

Pretty cool btw, neatly ordered, alpha is there for sure when you start tweaking the strats.