Thank you @money2020!

The last 48 hours have been a whirlwind.

We caught up with our partners, made hundreds of new connections, and shared key WalletConnect Pay milestones.

So much more to come.

There are two distinct quantum x crypto market opportunities.

1. Post-quantum security for digital assets. The goal here is to offer security guarantees for *existing* 2.6T of crypto assets. Yes, one cannot do this without upgrading chains. But you can try to offer as much added security as possible.

2. Quantum-native blockchain. Quantum compute is actually a value-creating technology: NISQs, even with just hundreds of noisy qubits, can be used for optimization problems, and as logical qubits emerge & gate fidelity improves, there is the possibility of quantum one-time programs & quantum cryptography. Even just a PoQW (proof of quantum work) L1 blockchain as the baseline is extremely interesting from a new "post-quantum" non-sovereign SoV asset standpoint.

There have been quite a number of teams building 1 (pq security), but 2 (quantum-native chain) is quite overlooked, and where most of the value creation will happen.

April fee data from the 1kx Onchain Revenue Report (1,000+ protocols tracked). Aggregate fees are down (-11% MoM, -20% YoY) as market volatility decreased both vs. March (Iran-uncertainty calming) and vs. last year’s Trump tariff-related moves, causing DEX and MEV-related fees to drive most of the declines.

It's a mixed picture on the category and protocol level, though.

• DeFi/Finance -11% MoM is a mixed bag:

--> Perps lost, e.g. @HyperliquidX -15%, though other markets gained, e.g. @Polymarket >3x in fees (largest gainer overall)

--> Lending markets gained in fees, led by @aave (due to utilization increase - see here: https://t.co/D5dzBCmy6w)

• L1 fee dispersion is widening. @ethereum 2x, @Zcash and @trondao up, while MEV-driven builders like @titanbuilderxyz give back March’s gains. Mostly a vol-compression unwind from March’s Iran-uncertainty spike.

• Middleware 7% growth driven by @chainlink and @CatFeeio

• DePIN 18% Fee decline almost entirely caused by @AethirCloud

• Wallet sector down 17% in fees, mainly due to interfaces like @AxiomExchange (-24%), @tradexyz (-18%). Even @phantom’s fee decline is mostly from their perps-trading interface

• Consumer overall flat-ish -4%, though bifurcation in Launchpads: @fourdotmemezh, @bonkfun, @farcaster_xyz with 50-80% declines in fees vs. @Pumpfun, @BagsApp positive. @printr as a new entrant

So what for 1kx: the decline in trading activity is in line with the compression in market volatility. Continuous growth in emerging DeFi categories like RWA is consistent with our Onchain Finance overweight. Prediction markets entering a fee-generating phase (Polymarket >3x) is consistent with our Frontier Applications thesis. Launchpad bifurcation tells us the consumer category is sorting itself.

Meet Event Rush, provided by @42space! Opinions are now tokenized.

Buy and sell event tokens on sports, news, crypto, and more.

Changed your opinion? Change the token.

Start now on Binance wallet ⤵️

https://t.co/9BYjElGKCh

Last week, 1kx Founding Partner @lalleclausen joined the "In Stablecoin We Trust: The Future of the Dollar" roundtable at the @MilkenInstitute Global Conference. A few takeaways.

Stablecoin payment volume (excluding bot activity) averaged $49B per day in Q1 2026, up 110% year over year and compounding at 50% CAGR over the past five years. That puts daily stablecoin payments above Visa (~$44B) and Mastercard (~$30B). Supply outstanding crossed $273B by quarter-end, up 28% YoY.

The growth is structural, not cyclical. Stablecoins are lower-friction payment rails picking up where the decline in correspondent banking has left off, and they offer better payment experiences for companies and individuals than the existing system delivers.

One of the most interesting threads of the discussion was about trust. The trust that US institutions and the dollar generate is, in effect, expressed through market adoption of USD-backed stablecoins worldwide. It is very hard for any other country, currency, or political system to replicate that. Whether a jurisdiction can produce a stablecoin that earns free-market adoption is becoming a useful signal of institutional credibility.

The build-out is happening in two layers. First, companies that handle the friction of integrating stablecoins into existing payment flows and treasury operations. Second, new banks being built that will flatten that friction into everyday treasury and payment work. Both layers are where we have spent the past several years deploying.

The closing analogy stayed with us. Stablecoins are to blockchains what email was to the early internet. Email was foundational, but it was never the point. Today, stablecoins are how we send a digital dollar back and forth. Blockchains will enable programmatic trading, clearing, and settlement of every existing financial instrument, plus financial primitives that weren't possible before.

Payments first. The rest is coming.

#MIGLOBAL

The European Commission literally just dropped a research on how to collect more taxes without making you angry enough to leave.

TLDR: higher wealth taxes, inheritance taxes + exit tax is coming

1kx will be at the @MilkenInstitute Global Conference in Los Angeles, May 3 to 6, where @lalleclausen joins the roundtable "In Stablecoin We Trust: The Future of the Dollar."

Milken brings together the CIOs, allocators, bank and asset-manager leadership, policymakers, and market infrastructure builders shaping the next decade of capital markets. This year, stablecoins and tokenized cash have moved from side panels into the core agenda: treasury, settlements, collateral, and liquidity.

We published our Cost of Trust thesis in 2019, arguing that blockchain reduces the cost of establishing trust to near-zero. What we're seeing now is institutions actually paying for that trust reduction at scale, in stablecoins, tokenized cash, and the settlement infrastructure underneath them. That these questions sit at the core of Milken's agenda rather than its periphery shows how concrete the shift has become.

The winners will be the structures institutions can actually hold, regulate, and plug into existing workflows. If you'll be at Milken and are thinking through what onchain finance means for your role as an allocator, issuer, or operator, our team would be glad to connect while in LA.

https://t.co/IgCENluzzh

#MIGLOBAL

The stablecoin market has 200+ issuers. Most won't survive contact with institutional capital. A few are already building for it.

At the 2026 @rwasummit in Cannes, our Founding Partner @HeyChristopher moderated Stablecoin Wars: What Structure Will Win with @peterlih (@AllUnityStable), @Benjamin918_ (@CapApp), and @MartindRijke (@maplefinance).

Three builders, three fundamentally different architectural bets:

→ AllUnity is issuing MiCA-regulated euro and CHF stablecoins under a BaFin e-money license, 100% backed, legally redeemable, and designed for businesses outside the crypto ecosystem

→ Cap is targeting pension fund capital directly, arguing smart contracts can allocate credit more efficiently than human-led underwriting, at structurally lower cost

→ Maple has shifted its primary KPI from AUM to ARR, betting that fee income matters more than scale

Our read: yield efficiency and credit automation only matter if institutions can legally hold the underlying asset. Regulatory structure solves for that first.

The stablecoins that matter will be the ones connected to the productive economy. The rest will remain infrastructure for crypto, not for capital markets.

Full panel below.

https://t.co/mmLVJySlaX

A highlight of @1kxnetwork investments within our thesis on threat-resistant & compliant onchain privacy.

- @0xMiden: chain designed from the ground up for programmable privacy (ZK)

- @zksync: private & customizable prividiums (ZK)

- @inconetwork: user-friendly privacy layer for existing chains (TEEs)

- @SeismicSys: privacy-enabled EVM-based fintech L1 (TEEs)

- @ligero_inc: private account layer for all chains, custom-built for businesses (ZK)

- @0xPredicate: programmable policy infra, for privacy protocols, defi, & beyond

- @fiber_evm: private EVM wallet infra w/ a slick mobile app (ZK)

Here's the exciting bit: (at least) five of the above projects are about to go live this year!

2026 is the year for onchain privacy.

-----

At 1kx, we put our money where our mouth is.

We develop theses and partner with the best founders to realize the shared vision.

Onchain finance needs threat-resistant privacy

→ Real-world & institutional finance cannot move onchain without privacy

→ To prevent misuse (e.g. laundering of hacked funds), the only viable solution is to build threat-resistant privacy

More in my op-ed in Forbes 👇

EBC12 Speaker: Christopher Heymann (@heyochristopher) | Founding Partner | @1kxnetwork

Before venture capital, Christopher Heymann spent years building technology companies as a CTO. He co-founded 1kx in 2018, building it into one of the most active early-stage token funds in the market, backed by sovereign wealth funds, pension funds, endowments, and family offices.

The firm has backed over 150 projects across cryptoeconomic design, governance, and decentralized infrastructure. 1kx does not just provide capital, it embeds itself in the technical and strategic challenges founders face.

Join the leaders shaping digital assets in Barcelona on September 16-17: https://t.co/SS1oYoYh5J

Proud for @1kxnetwork to lead the pre-seed for @justinmujin to build @giggles_app, a new social network that explores the intersection between video discovery and financialization.

I first discovered Giggles organically on TikTok and immediately reached out to see how well Justin had already grasped the core affordances of crypto in reshaping relationships and communities with financialization.

We spent a lot of time over several months building a relationship and concluded that we should work together.

Today, I'm proud to share our partnership publicly and am incredibly excited to watch them execute in the near term with their launch.

We’re excited to share that 1kx led the pre-seed in @giggles_app - a new kind of social network where users can buy into videos early and participate in the upside as they spread.

We think Giggles opens up a compelling new design space at the intersection of social behavior, market design, and crypto-native coordination.

Congrats to @justinmujin, @itsedwinwang, and the whole team.

Big thanks to @TechCrunch and @asilbwrites for the exclusive: https://t.co/EtfJ0AAaDi

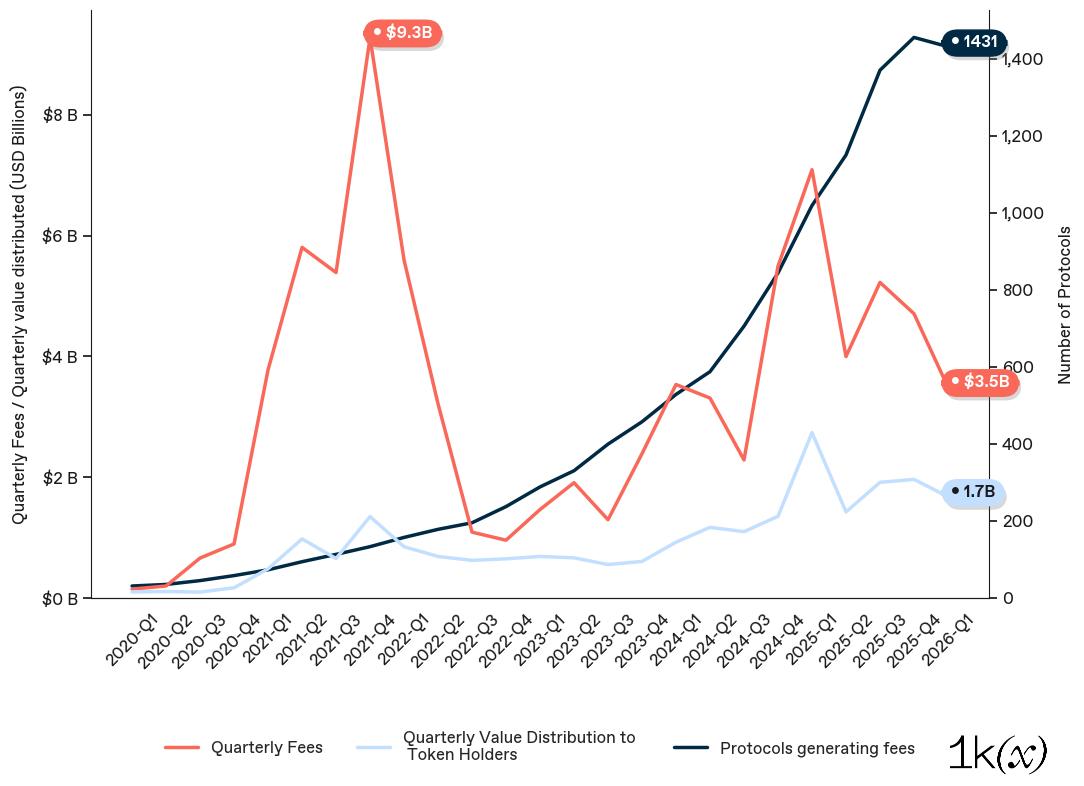

Mixed picture for onchain fundamentals in Q1 2026:

User-paid onchain fees are ~50% lower than last year, and 26% down QoQ. Value distributed to token holders remains stable, while the number of monetizing protocols has slightly declined for the first time.

Sector changes:

• Overall decrease purely driven by DeFi (-34%) incl. related infra, e.g. bridges -43%

• Perps hit hardest (-36%), Stablecoin issuance up driven by @SkyEcosystem

• Wallets -16%, Consumer -12%, though launchpads up 10%!

• DePIN the only positive sector, +13%

• Blockchains -5%, though @Zcash up 80% and @0xPolygon with +4x

Fee shares broadly in line with '25 avg: Blockchains 21%, DEXs 24%. Same for cohort view: protocols that first monetized in '24 or '25 still generate ~47% of all fees.

Protocol-wise: @Zcash climbed to #2, @Pumpfun fees up. Biggest mover: @BagsApp (+180 ranks), though the Jan fee explosion is fading. @farcaster_xyz now #25 after folding in @clanker_world fees.

Protocols that stopped monetizing: @level, @elixir, @mars_protocol, @EARNMrewards, @Lifinity_io (shut down/exploits). @kucoincom hasn't announced any burn yet this quarter. Some protocols had >$100k in fees last quarter and are now at $0 - Among them: @quanto@lava@rezervemoney

Shoutout to the data providers: @DefiLlama@tokenterminal@Dune@EigenPhi and many more 🙏

Featured charts: fee trends + token holder distributions / fee shares by sector / top protocols by fees Q1 2026 👇

The elephant in the room for onchain yield in crypto is Bitcoin 🐘

Most of our clients hold billions in BTC that generate no yield. Today, only ~1.6% of BTC (about $21B out of a $1.35T asset class) is productive, for a few key reasons:

→ BTC is not natively yield-bearing like ETH or SOL

→ Since FTX, centralized lending desks have largely disappeared (e.g. Genesis)

→ The “Bitcoin staking” narrative has lost momentum post-FTX

→ Bitcoin holders tend to be particularly cautious when putting their assets to work

We are addressing this with @railnet_org, in partnership with @monarq_mgmt, the asset management arm of @FalconXGlobal.

Led by @ShiliangTang and a team with backgrounds at @TowerVentures and @Point72Careers, Monarq has developed a strategy that takes BTC as input and allocates it across DeFi and RWA opportunities. The approach is multi-venue, risk-managed, and fully transparent, targeting up to 6% yield on BTC.

Railnet provides the orchestration layer: configurable risk controls, real-time accounting across positions, and fully auditable onchain execution. Allocators can see exactly where capital is deployed and how yield is generated.

Excited to help shape the future of onchain asset management and make billions of Bitcoin productive again🚶

More information: https://t.co/mluYeAyEAQ

PS: Tomorrow, we are releasing a Railnet Talks episode with Shiliang Tang from Monarq Asset Management. We go deeper into what an institutional approach to BTC yield really means, why it is difficult to execute well, and what the market is missing today.

Stay tuned 👀

@TweetsOfSumit Die Entfernung wie weit die Politiker in Berlin an der Realität vorbei entscheiden wird mittlerweile in Astronomischen Einheiten (AE) gemessen.