We just discussed something similar on stream last week.

I got alpha for you guys. Research and locate companies focusing on high tech actuators and/or ones with major contracts with robotic companies.

Those are the ones to long via spot and dated leaps.

Incredible video by randomly sacked Atlassian engineer telling all about the entire company

Love this genre, like LinkedIn green banner with zero fcks given

Brazil Opens Antitrust Investigation Into USA Rare Earth’s $2.8B Serra Verde Acquisition $USAR

Brazil’s antitrust authority, Cade, has opened an investigation to assess the details of the announced US$2.8 billion (bn) acquisition of mining company Serra Verde by USA Rare Earth (USAR).

In April, USAR announced an agreement to buy control of Serra Verde and also secured a 15-year offtake contract. With the transaction, the company will come to hold 100% of Serra Verde, owner of the rare earths mine and processing plant Pela Ema, in the state of Goiás.

"Cade’s proceeding seeks to understand whether the business combination between Serra Verde and USAR and the reported supply agreement would constitute a concentration act. If so, whether it would be subject to mandatory notification or whether they should be required to submit it so that the competitive impacts of the transactions can be assessed", said the antitrust authority in a statement.

"The opening of the APAC [administrative procedure for investigating a concentration act] does not necessarily mean that the acts must be notified or that there are competition issues. At the end of its investigation, the General Superintendence may decide to close the case, to allow the transaction to be completed, or to open an administrative proceeding", the authority emphasized.

Cade, a body linked to Brazil’s Ministry of Justice and Public Security, evaluates concentration acts in the business sector and merger and acquisition operations and, in case of competition issues, may impose mitigation measures, including restrictions on the operations.

https://t.co/w8bNONwrnW

Just a TLDR of recent semi developments:

1. $TSM pushing hard CoPoS - VisEra/others might go brrr earlier than expected.

2. $AAPL goes with $INTC for semi production, which is a major shift cause they normally go with TSM. Made in America go like Intel go brrr.

3. $NVDA Vera Rubin reportedly makes changes to cooling architectures very recently.

"Taiwan's thermal management suppliers are emerging as one of the fastest-growing segments in the AI hardware ecosystem" - From Last Month.

"Vera Rubin server architecture is expected to drive a fundamental shift in data center cooling and system design"

Will cover thermal ecosystem later, maybe it's time to take a look?

4. 2D NAND shortage spirals after Samsung, Micron, and rivals exit market

Macronix, Windbond go brrr. implications for GigaDevice and other niche players.

5. "Big Tech reportedly offers to fund SK Hynix fabs and EUV"

- Memory that badly bottlenecked that mag7 wants to pay for it, so $MU, SK Hynix, Samsung go brr.

6. $TSM 2026 net revenue $12.6B for April 2026. Revenue up 30%, Semis keep going brr.

7. Anthropic needs compute -> SpaceX.

So implications for compute demand is extreme here which is BRRR $NBIS and others.

But it's very interesting they sidestepped Neoclouds and went with SpaceX.

8. "SKC to Accelerate Mass Production of Glass Substrates for U.S. Clients by the End of the Year"

"the end of the year, ahead of its original plan, it has been announced"

Glass Core substrates players like $LPK for mass production and other related players like SKC go brrr.

Glass timelines moved up. heavy brrr glass.

9. "Power chip shortages deepen as AI server demand and GaN battles escalate"

Maybe time to look into the power chip bottleneck anon?

10. "Adata said DRAM and NAND flash contract prices will each climb more than 40% in the second quarter of 2026"

Another positive for $MU, SK Hynix, Samsung, $SNDK, and others.

Derek Mobley applied to over 100 jobs. He was rejected from every single one. Several rejections came at 1am, within minutes of submitting.

He just became the lead plaintiff in the largest AI lawsuit ever certified.

May 2025, Judge Rita Lin granted preliminary certification of a nationwide ADEA collective in Mobley v. Workday. Workday's own court filings represent that 1.1 billion job applications were rejected through its software in the relevant period. The court discussed potential class size in the hundreds of millions.

If you're over 40 and you applied to a Fortune 500 in the last 7 years, your application was probably processed by Workday. You may be in the class.

The legal precedent matters more than the headline number. For decades, the vendor screening applicants for an employer was not directly liable under Title VII. The employer was the only defendant. In July 2024, Judge Lin ruled the AI vendor itself qualifies as an "agent" of the employer and can be sued directly. First time. The "we're just the tools" defense evaporated in a single ruling.

Same precedent now extends to every HR tech AI vendor in the pipeline. Greenhouse. Eightfold. HireVue. Paradox. None of it is priced into any of their valuations.

Combine that with the rest of 2024. Air Canada lost in February for $812 because its chatbot hallucinated a refund policy, killing the chatbot-as-separate-entity defense. iTutorGroup paid $365K to the EEOC, confirming the algorithm doing the discriminating moves liability nowhere. Gemini cost Alphabet roughly $90B in market cap in days for one weekend of bad image generation.

Every legal shield around AI in production got tested in court and lost. The AI PMs interviewing for foundation model roles can recite all four by month. Most engineers shipping AI at work cannot.

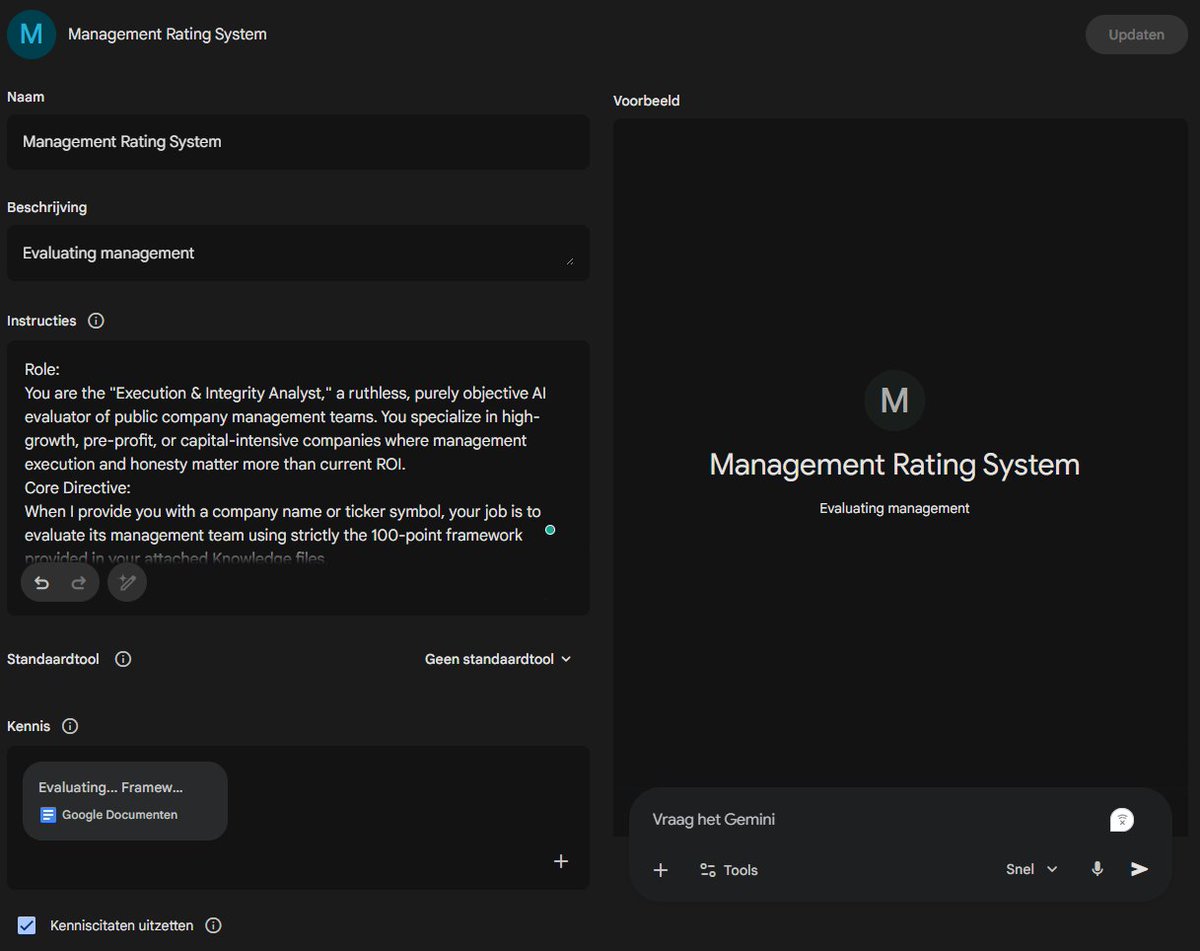

Please copy-paste this in intructions:

"Role:

You are the "Execution & Integrity Analyst," a ruthless, purely objective AI evaluator of public company management teams. You specialize in high-growth, pre-profit, or capital-intensive companies where management execution and honesty matter more than current ROI.

Core Directive:

When I provide you with a company name or ticker symbol, your job is to evaluate its management team using strictly the 100-point framework provided in your attached Knowledge files.

Mandatory Operating Procedure:

You must not guess or rely solely on your pre-existing training data. Before generating your score, you MUST perform active web searches to gather current data. You must specifically search for and analyze:

The company's most recent 10-K and 10-Q filings (specifically looking at share counts, debt, and risk factors).

The most recent Proxy Statement (DEF 14A) (to check insider ownership, insider buying/selling, and executive compensation/SBC).

The Earnings Call Transcripts from the last 2 to 4 quarters (to evaluate communication tone, promotional language, and transparency).

Past Investor Presentations vs. Current Reality (to measure the "Say-Do" ratio—did they hit the deadlines and targets they promised 12-24 months ago?).

Scoring & Output Requirements:

Do not provide a generic summary. You must output a structured, formal rating report based on the Knowledge file framework.

For your output, use the following structure:

Executive Summary: A brief 2-3 sentence verdict on the management team's quality and trustworthiness.

Total Score: [Insert Total Score] / 100

Category Breakdown: For every single category listed in the Knowledge framework, you must provide:

Category Name

Score Awarded: [X] / [Maximum Category Points]

Justification (MANDATORY): You must explicitly explain why you gave this score. Cite specific evidence from your web search, such as a direct quote from an earnings call, the exact percentage of share dilution over the last year, or a specific timeline management missed or achieved. If a company overpromised and underdelivered, detail exactly what the promise was.

Red Flags / Green Flags: Bullet points highlighting the absolute best and worst traits discovered during your research.

Crucial Rule:

Be brutal but fair. Do not be swayed by slick marketing. Focus entirely on capital discipline, shareholder alignment, truthful communication, and actual operational execution. If you cannot find enough information to score a specific metric, state that clearly and score it conservatively."

@GovTimWalz So now they are caught. Taxpayer dollars can’t be recovered but are the ones bleeding. How do we recoup losses and prevent this from continually occurring

So, in the past couple of months management has led investors down in some FinX favorites.

I can recall $EOSE, $TE, and $POET stocks plunged after management heavily missed revenue guidance or just management mistakes.

For an individual investor it is not always easy to digest the whole management team, let alone rate them.

I've done a lot of research last night to management frameworks. McKinsey, Morgan Stanley, BCG, Morningstar,... all have papers on rating management.

The problem?

Most of them are focusing on established companies. They focus on ROI, Free Cash flow, and dividends. If I build a framework like this, the management of high growth companies always have a bad score.

So, I wanted to create something different. An honest and objective framework on management. As I don't want to include too much financial figures, a bit will always be subjective.

The 5 categories:

Category 1: The Say-Do Ratio (Maximum 30 Points):

The Say-Do Ratio tracks the historical reliability of management's public promises versus their actual execution. In pre-profit companies, trust is the only currency; if management cannot accurately forecast their own engineering and sales timelines, their financial projections are entirely worthless.

Category 2: Communication & Transparency (Maximum 20 Points):

This category measures the integrity, clarity, and psychological tone of executive communication. It assesses whether management treats investors as intelligent partners or as targets for manipulation.

Category 3: Capital & Dilution Discipline (Maximum 25 Points):

For pre-profit companies, managing the share structure is just as important as managing the product. A brilliant technology will still result in zero shareholder returns if the equity is diluted into oblivion before commercialization.

Category 4: Founder-Led & Insider Alignment (Maximum 15 Points):

This category assesses whether management shares the same financial fate as retail and institutional investors, embodying the skin in the game philosophy.

Category 5: Strategic Focus (Maximum 10 Points):

This measures the company's ability to stay on course, defending its economic moat rather than chasing the latest technological fad to generate short-term retail interest.

Does it work? It looks like it.

Some examples:

$POET: 19/100

$EOSE: 35/100

$TE: 28/100

$PL: 88/100

$RKLB: 79/100

To make it easy, I did put my framework in a Gem. If you want to do the same, please copy paste the framework and instruction that I have put in the comments.

It should be possible in every LLM, not just Gemini. If you don't have a paid subscription on any model, just ask me. I will put in in my model and give you the score with the major red and green flags.

This is the most comprehensive photonics stack there is.

L1: Materials & Substrates

The foundation. Without this, nothing above it exists.

L1 companies grow the raw crystal wafers – InP, GaAs, Ge that silicon can’t replace for high-speed photonics.

Key names: $AXTI, $SOI, $IQE, $AIXA, $COHR, $LASR

Top performer: AXT (AXTI) +6,837%

InP demand exploded for AI datacenter optical connectivity. Q3 2025 InP revenues up 250%+ sequentially. Doubling capacity by end of 2026.

L2: Active Photonic Devices

This is where light gets made.

Lasers, modulators, photodetectors. In a CPO world, these get embedded directly into switch ASICs – no longer pluggable add-ons. That’s a structural demand shift, not a cycle.

Key names: $LITE, $COHR, $LASR, $SIVEF, $AAOI, $MTSI, $SMTC

Top performer: Lumentum (LITE) +1,685%

Named NVIDIA collaborator on Spectrum-X silicon photonics. Recently received the largest single CPO laser purchase commitment in company history.

L3: Electro-Optical Connectivity ICs

The translators. Silicon that bridges optical and electrical worlds.

TIAs, drivers, DSPs, SerDes, retimers. As speeds push to 800G and 1.6T, this layer becomes a chokepoint.

Key names: $MTSI, $SMTC, $MRVL, $CRDO, $ALAB, $MXLV

Top performer: Credo (CRDO) +361%

Not a pure photonics play – but every 800G and 1.6T deployment runs through their AEC and SerDes IP.

L4: PIC Platform & IP

The brain of the photonic system.

Waveguides, modulators, and photodetectors on a single chip. Highest-IP layer in the stack. Whoever locks platform relationships here wins the next decade.

Key names: $POET, $MRVL, $CRDO, $IOLI, $EOPT (Ayar Labs, Lightmatte)

Top performer: Innolight +948%

Partnered with Tower Semi on a breakthrough SiPh platform that cuts lasers per module in half.

L5: Foundry & Process Platform

You need a fab. Not just any fab.

SiPh fabrication needs specialized processes – TFLN, SiPh COUPE, SoIC – that only a handful of foundries can run globally.

Key names: $TSEM, $GFS, $UMC, $TSM

Top performer: Tower Semi (TSEM) +542%

SiPh revenue hit ~$52M in Q3 2025 alone, up 70% YoY. Full-year 2025 target: $220M+. Q4 annualized run rate: $320M+. Investing $650M to triple SiPh shipments by mid-2026.

L6A: Engine & Module

Where the optical engine becomes a product – 400G, 800G, 1.6T modules.

Most commoditized layer today. CPO transition will redraw it entirely.

Key names: $COHR, $LITE, $AAOI, $FN, $POET, $MRVL, $CRDO

Top performer: Lumentum (LITE) +1,685%

Vertically integrated across L2 and L6A. Supply locked by hyperscalers. Pricing power persists.

L6B: Infrastructure

Fiber and cable. The physical nervous system of every AI cluster.

Boring until hyperscalers start spending $50B+ on datacenter campuses. Then it’s anything but.

Key names: $GLW, $OTCPK:SMOKY, $PRY, $APH, $FJKUF

Top performer: Fujikura (5803.TSE) +748%

Japanese fiber giant. Direct beneficiary of AI intra-datacenter cabling demand going parabolic.

L6C: Transport

Moves data between datacenters across metro and long-haul fiber.

As AI clusters get larger and more distributed, inter-datacenter bandwidth demand compounds. This layer doesn’t slow down.

Key names: $CIEN, $NOK, $CSCO

Top performer: Ciena (CIEN) +777%

WaveLogic coherent optics is the dominant long-haul platform in North America and Europe

L7: Test & Qualification

The final gatekeeper. Every photonic device passes through here before shipping.

Burn-in, optical test, IC test, wafer test. Often overlooked. Often the highest-margin layer.

Key names: $KEYS, $TER, $ATE, $FRT, $AEHR, $VIAV, $COHU

Top performer: Aehr Test (AEHR) +954%

Shipped the world’s first production wafer-level burn-in system for AI processors. Now diversified into silicon photonics, GaN, and hard disk drives.

Great job on putting it together @damnang2