Most NRIs investing in India ask "which fund should I buy?" before they've asked where they're tax resident. That sequencing error causes real, expensive tax problems.

We've looked at the major things NRIs and OCIs don't think about before investing in India: tax residency (and why your Indian passport has nothing to do with it), which investment instrument is most tax efficient as per your current tax-residency jurisdiction, and what getting that wrong actually costs in practice.

The structure around your Indian investment often matters more than the investment itself.

If you have Indian money to invest, or have Indian money already invested, this piece by @avijeet_sen worth a read.

https://t.co/57HJKBZpVg

India is now a value stock

FIIs have been net sellers for several quarters, with substantial cumulative outflows. Domestic flows have held the market up, but the relative narrative is changing.

For fifteen years, MSCI India's (USD) underperformance against MSCI Emerging Markets (USD) was shallow and short-lived. Every dip was followed by a recovery. "Buy India when it lags EM" was a near-mechanical trade.

That pattern has broken. The latest reading sits at -54% points, more than twice as deep as anything before, and it has been deepening, not bouncing. This isn't a dip waiting to be bought. This is an asset that has been reclassified.

India is almost going from being priced as a growth stock to being priced as a value stock. This isn't necessarily bad. Value stocks compound too. They just compound on different terms.

The expectations are lower, the multiples are saner, and the room for upside surprise is wider. A market that's stopped paying for hope is a market where good news actually moves prices.

The US 30Y Treasury is above 5%. Japan's 30Y JGB crossed 4%. Japan's 10Y JGB, the bond that traded near zero for a decade, is past 2.7%.

Bond markets are repricing trust everywhere.

And India is being repriced too from a growth stock to a value stock, which is not a bad thing. Just a different one.

Same story, different registers. Read the full piece:

https://t.co/xWQaJekxiq

Your ESOP letter says one number. Your bank account will disagree.

Here's the bit nobody explains at the townhall: when you exercise, the gap between FMV and strike price is taxed as salary. Not when you sell. When you exercise. In cash. At your slab rate.

At ₹2 crore total income, that's roughly 39%. On a ₹2.1 crore perquisite, about ₹82 lakh leaves before you've sold a single share.

Add ₹10 lakh in strike price to exercise, and you're out ₹92 lakh while the stock is still in lock-in.

When you finally sell — assuming the price held — capital gains are calculated against FMV at exercise, not your strike. Often a small loss. Useful for set-off, not much else.

Net new wealth on a ₹1.9 crore ESOP? Closer to ₹98 lakh.

If you're sitting on ESOPs and a liquidity event is coming, read this first: https://t.co/X1eL8Hir4M

My guest today is Paul Tudor Jones (@ptj_official), one of the greatest macro traders of all time.

He correctly predicted the 1987 stock market crash and shorted the Japanese bubble in 1990. For over 40 years, his flagship fund has had a negative correlation to the S&P 500. 100% of his returns are alpha.

He says today's market has so many similarities to 2000, "the easiest bear market I've ever seen in my whole life."

He makes the case for going long dollar-yen, why Bitcoin beats gold as an inflation hedge, and why he was wrong about Warren Buffett.

But what I'll remember most from this conversation is Paul's zest for life. He's 71 and still wakes at 2:30 every morning to trade the London open. He works out for two hours a day. He walks with his wife every evening. He travels the country chasing peak spring and peak fall. He's so excited about the songs picked for his funeral that he wishes he could be there to hear them.

Paul has lived five lifetimes in one. He's one of the most entertaining and interesting people I've met, and the conversation will leave you searching to be as passionate about what you do as he is about what he does.

Enjoy!

Timestamps:

0:00 Intro

1:00 The Kindest Thing

13:19 Trading vs. Investing

17:33 Lessons from Warren Buffet

22:24 The Existential Risks of AI

29:54 The Nature of Trading

31:46 Bitcoin

35:55 Bubbles

42:08 A Day in the Life of PTJ

46:00 Information Overload

47:07 Passion for Markets

50:49 The Robin Hood Foundation

54:18 The Workless World

56:03 Journalism

1:00:00 Principal Components of a Great Life

1:05:06 Kill Them With Kindness

Learnt something last couple of days… appears vast majority of people think a PMS is only and only what you use to manage equity portfolios. World over one of the more prevalent use of PMS is to administer and execute advice for clients. A PMS which can allocate to direct plans of MFs and to REITs, InVITs, Bonds, Index Funds, ETFs et al can be a powerful structure for advisory practitioners. It can manage asset allocation and manager selection decisions with advice embedded in the PMS and a non clumsy formal mechanism of charging advisory fees. The fee might end up higher than direct plans of mutual funds but with advice embedded and it would be lower than regular plans of equity and hybrid funds on a full asset allocation basis.

Done right, PMS' can be one of the most effective ways to service HNIs with tax-efficient Mutual Fund baskets. At @capitalmind_in, our first such portfolios were offered for fees as low as 25bps.

Today, we offer 5 such investment approaches. And for each, our gross fees (including the underlying MF's BER) is < the basket's weighted average Regular BER.

And, we don't charge any performance fees on any of our MF baskets

Performance fees on top of a mutual fund portfolio - that too without a hurdle - is unusual, to say the least.

It's asking for a profit share for recognising someone else's skill. When the underlying isn't allowed to charge a performance fee, layers on top shouldn't be allowed either.

Most HNI portfolios have the equity part figured out. What they're missing is the sleeve that keeps them invested when equity does what equity does: drops 25-30% and tests every investor's nerve.

Shray sits down with @AkankshaMaulik and @iKrishnaAppala to talk about Capitalmind Anchor: a product that's been quietly in the works for a while. It's not a stock strategy. It's not chasing alpha. It's a rule-based basket of hybrid mutual funds designed to keep you invested when everything around you is telling you to run.

If you're 100% in equities and have never thought about what happens to your goals when a bad market shows up at exactly the wrong time, this one's worth your hour.

https://t.co/pgxsDfi0Xx

Sequence risk is the one risk nobody prices in.

Year 1: +18%.

Year 2: +22%.

Year 3: markets crash, -30%.

Now you need the money.

Your long-term average was great. Doesn't matter. The crash landed at the worst possible time.

The investor who made lower returns in years 1 and 2, but only fell 12% in year 3? They walked away with 11% more money.

This is the whole idea behind Anchor IA. Built to keep you invested when it matters most.

I sat down with @AkankshaMaulik to talk more about it.

https://t.co/CR8NhnhiJm

Observation: Generally, market leaders from the previous bull market don't participate in the next one.

Why? Because by the end of the cycle, there's nothing unknown left.

a) You have understood the actual potential of the industry.

b) Margin profile is known (40% margin kaise kar sakte bhai, 25% hi peak hai).

c) You know each company's management potential.

d) The entire value chain is dissected.

e) Every analyst covers each percentage point, leaving little room for any positive surprise.

So new bull markets need new stories. New unknowns. New "yeh toh phodne wala hai yaar" theme. The next big thing.

But what's happening now is interesting.

Power utilities have been in a bull market since 2021. Took a break. And almost all of them are coming back. Same with defence, semiconductors, and energy.

The story moved from "India energy independence" to "AI needs more power."

In my view, this is actually a positive sign.

Markets genuinely believe in the overall sector's growth story. Even though there is nothing unknown left.

Rational exuberance?

We just finished our first financial year at @CapitalmindMF !

500+ cr. AUM

4 funds - Equity, Debt and Hybrid.

11,000+ investors, 1300+ cities/towns.

3,400+ distributors empanelled.

Started with 45 cr. in the NFO, 8 months ago. We're still small - tiny, in fact. Which means we have to work hard to grow. Our team has grown to 48+, with our HQ at HSR Layout in Bangalore and offices in Baroda, Chennai and Hyderabad; they've done an incredible job getting this in shape.

Thanks for your support, and looking forward to a productive year ahead!

Visit https://t.co/HTuaYb44Po for more.

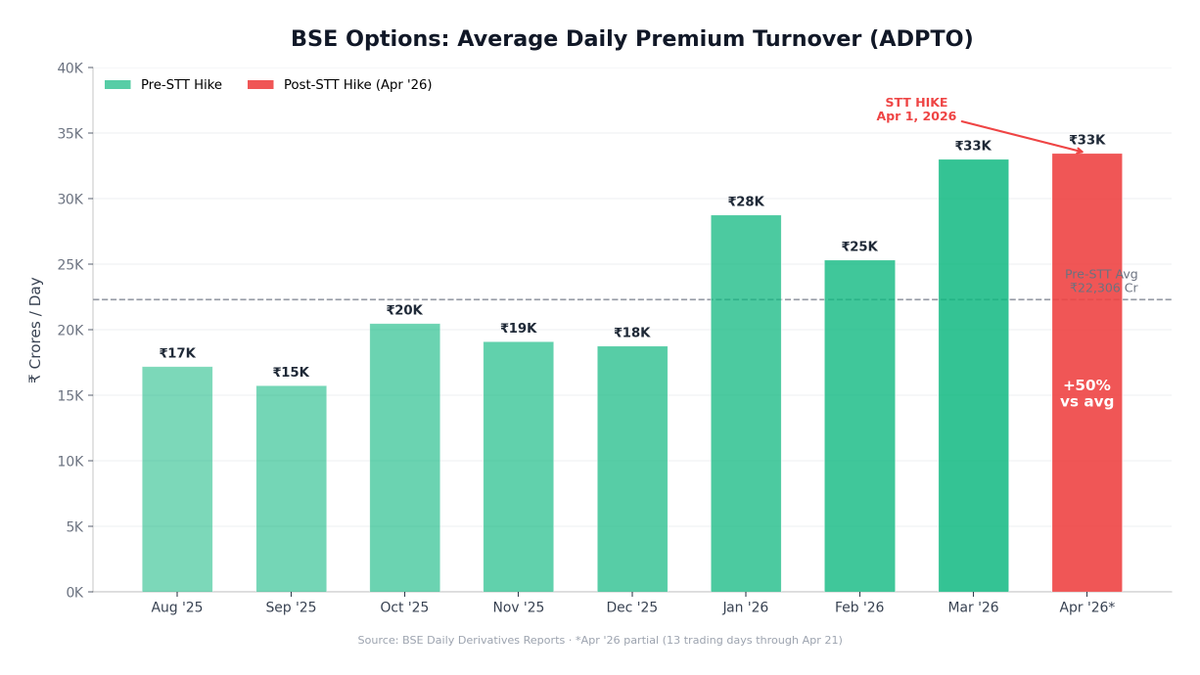

BSE's Options Premium Turnover: No major impact post the STT hike

Pre STT hike (Mar 2026 ADPTO): ~33k Cr per day

Post STT hike (Apr 2026 ADPTO, till date): ~33k Cr per day

Volumes have actually increased marginally, not dropped.

Disc: Holding BSE in Capitalmind PMS strategies. Not a recommendation.

Your mutual fund's Total Expense Ratio (TER) can be very misleading because they are required to "annualize" even transaction costs - so don't be alarmed when you see 50% TER!

@uptickr explains in an article in @livemint .

Strait of Hormuz: open, close, open, cloopen.

The more this cycle repeats, the less sentiment it carries & the faster markets will discount it.

At this rate, the next closure will be a non-event before it even happens.