And with services wage growth below, showing the clear divergence in late 2010s when corporates absorbed higher costs to protect market shares, resulting in stubbornly low core inflation, fuelling the @ecb's negative rates.

Dear @ecb, it looks like we won't get the usual Excel files with the staff projections anymore, will we? We can download the whole dataset (https://t.co/vOjKVnFeDA, but the xls file was way more user-friendly and some data are missing (eg, contributions to GDP deflator).

and the euro area imports 2x as much from China as it now exports.

the post pandemic recalibration in imports from China also looks to have run its course, with imports now stable at EUR 400b/ likely to grow from here

tis a big shift over the last 3ys

2/2

The latest services ESI points to 3.7%ish wage growth in the services sector in Q2 and is trending down. The ECB assumed >4% for the whole economy in 2024.

In an idle moment (🤓) I've had a look at whether the Bank of England MPC has ever changed rates at the meeting before a general election.

Short answer is 'no', but the slightly longer answer may be more interesting... 🧵

@thomdvorak Hi, @thomdvorak ! The download link (inside the link you posted) is leading to another report: "Working age population will decline in many metros"

Since this week's #AutumnStatement there's been a lot of talk on the central paradox – taxes were cut, while taxes are still going up.

But we wanted to touch on five other important points that risk getting lost amid the row...

A quick thread 📈🧵⤵️ https://t.co/JB0E3SZrsT

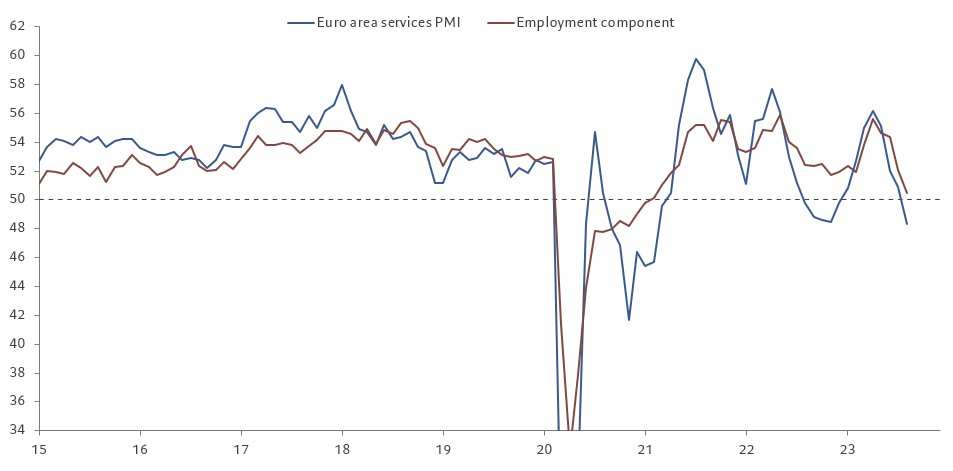

🇪🇺 Four takeaways from euro area PMIs.

1. Services sector contraction led by Germany, with early signs of labour market weakening. A sign that monetary policy transmission is working.

A useful bit of data for those trying to gauge the impact of possible Chinese Treasury sales on the market --

about 30% of official holdings have a remaining maturity of less than 2ys, and just over 60% a remaining maturity of under 5ys.

(table A12)

https://t.co/Lneaut6XJL