Everyone can access frontier models. Very few can create proprietary judgment data inside a clinical workflow.

That’s the moat.

Once you own the feedback loop, you can train the model on what actually will be useful.

I am betting Nvidia executive, former CRO of Groq knows more about AI cloud products than random "experts" on X. Ignore the noises.

I have full conviction in the best team with clear and focused vision. $NBIS

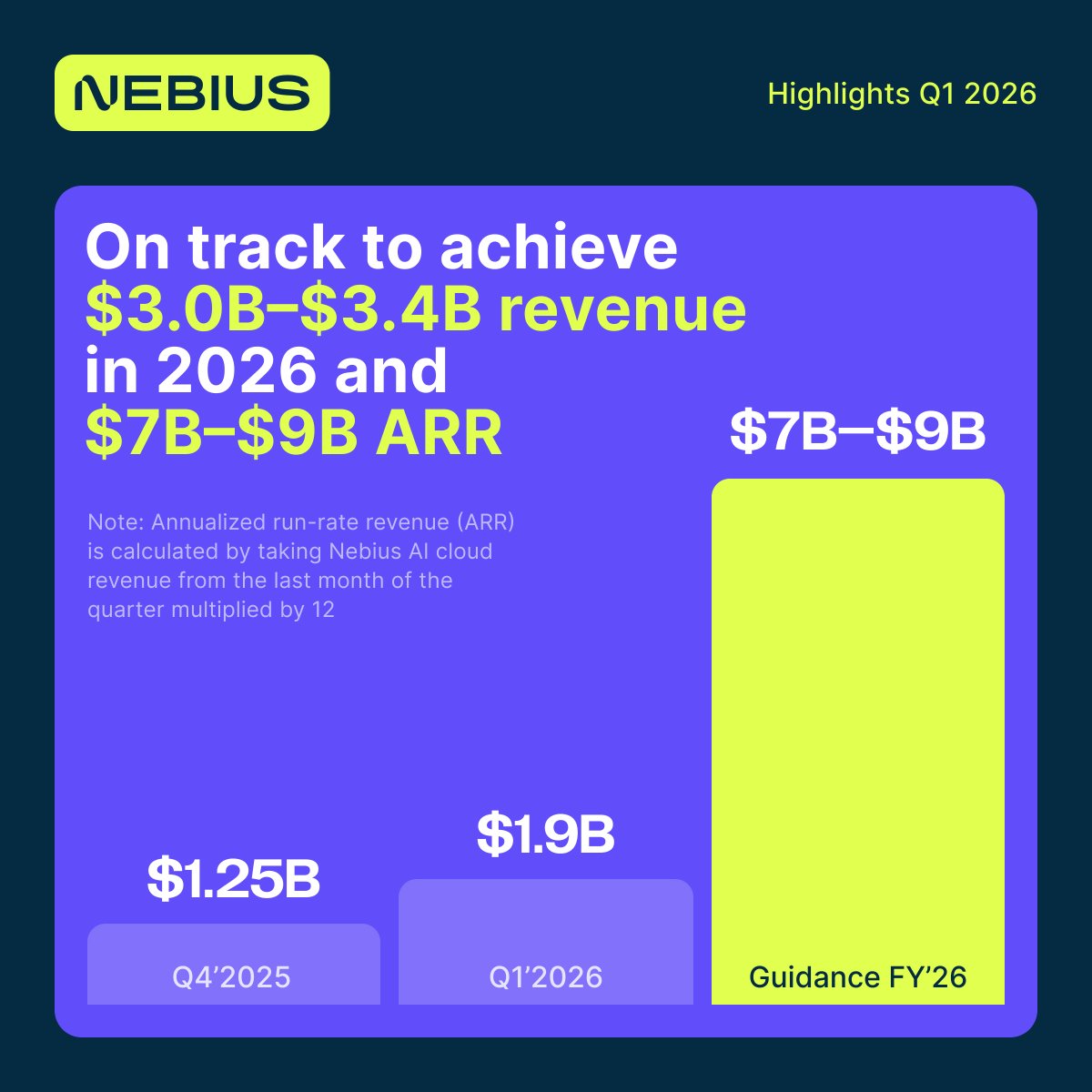

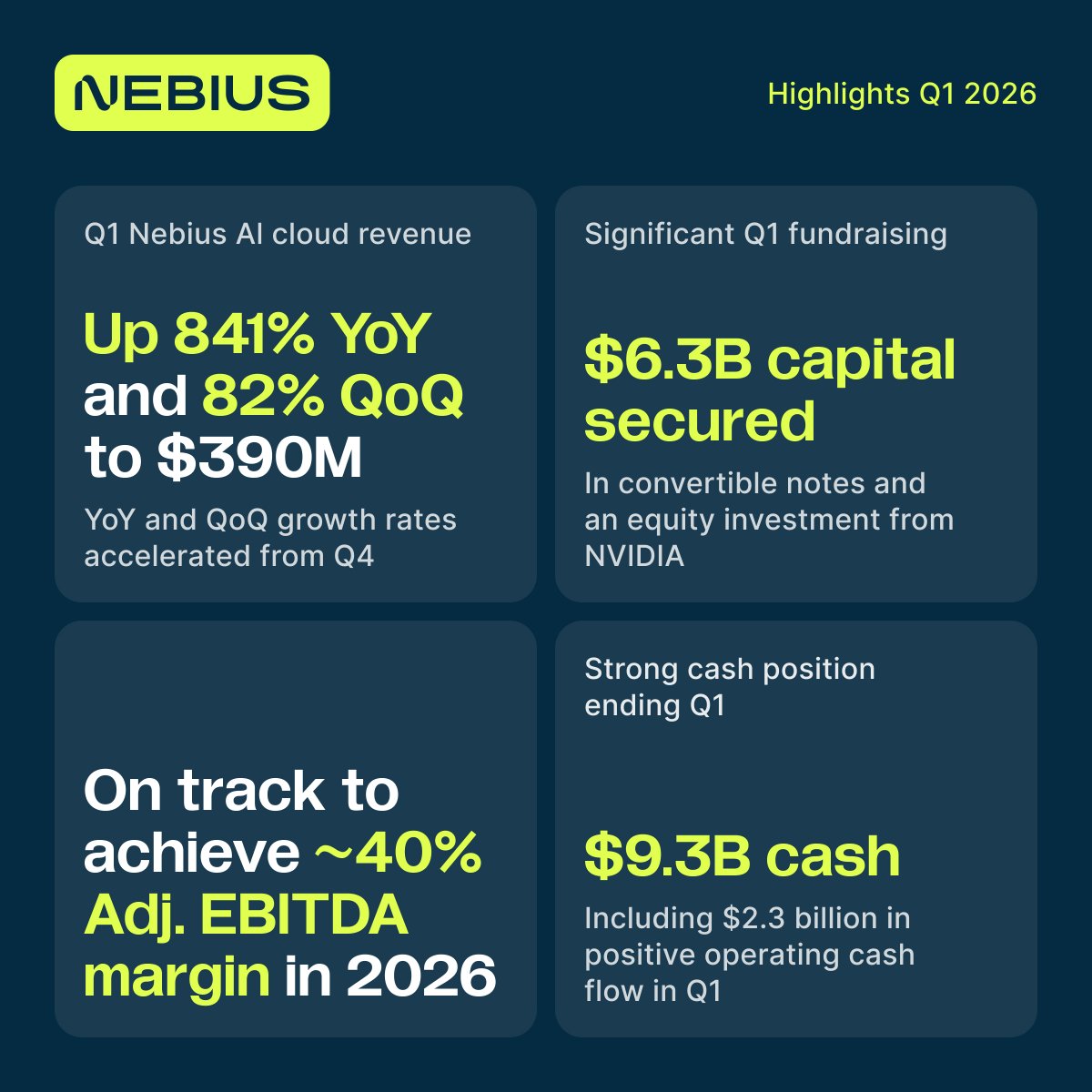

Today, we announced our Q1 2026 financial results. Here are the highlights:

- ARR grew 674% year-over-year; full-year guidance has been updated to ARR of $7-$9 billion and revenue of $3.0-3.4 billion.

- Adjusted EBITDA margin in our AI cloud business nearly doubled quarter-on-quarter to 45%.

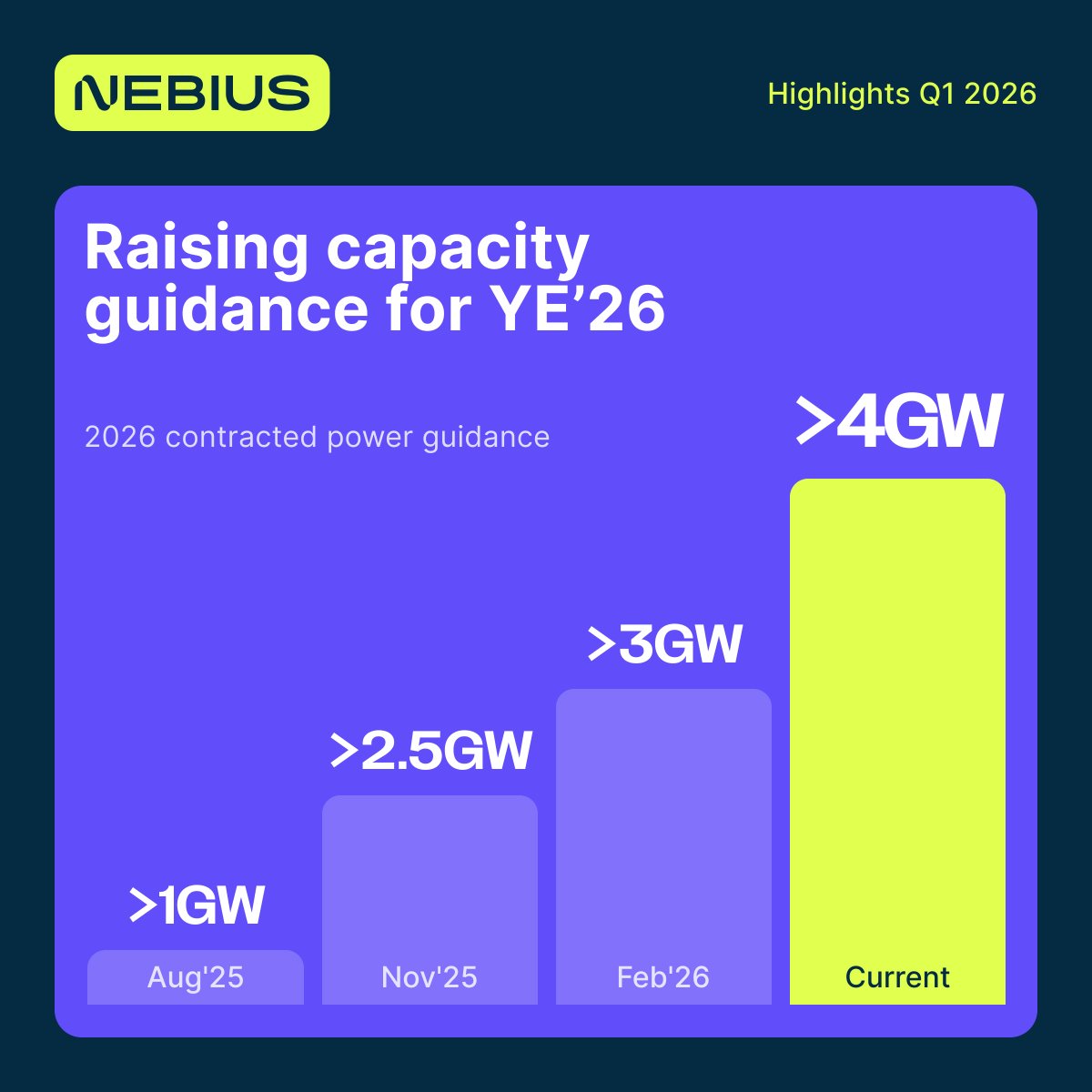

- Contracted capacity now exceeds 3.5 GW, surpassing our 3 GW target; we now expect to have more than 4 GW of contracted capacity by the end of 2026.

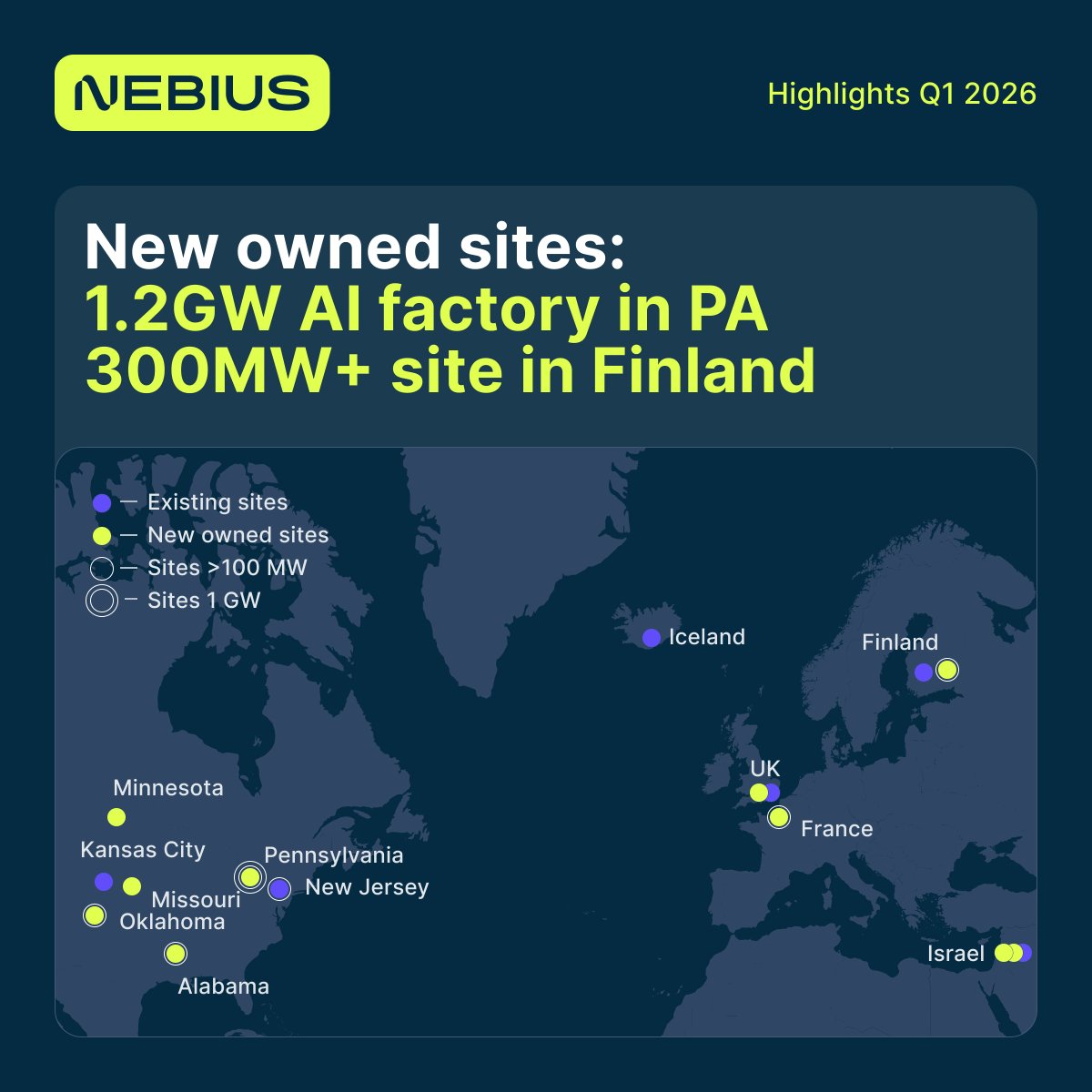

We also announced today that we have secured up to 1.2 GW of power and land for a new owned AI factory in Pennsylvania, bringing our total number of sites exceeding 100 MW to seven.

Read more in our press release: https://t.co/GJkNTg8RGG

If AI keeps scaling, where does the factory break first?

I built a public dashboard for that one question.

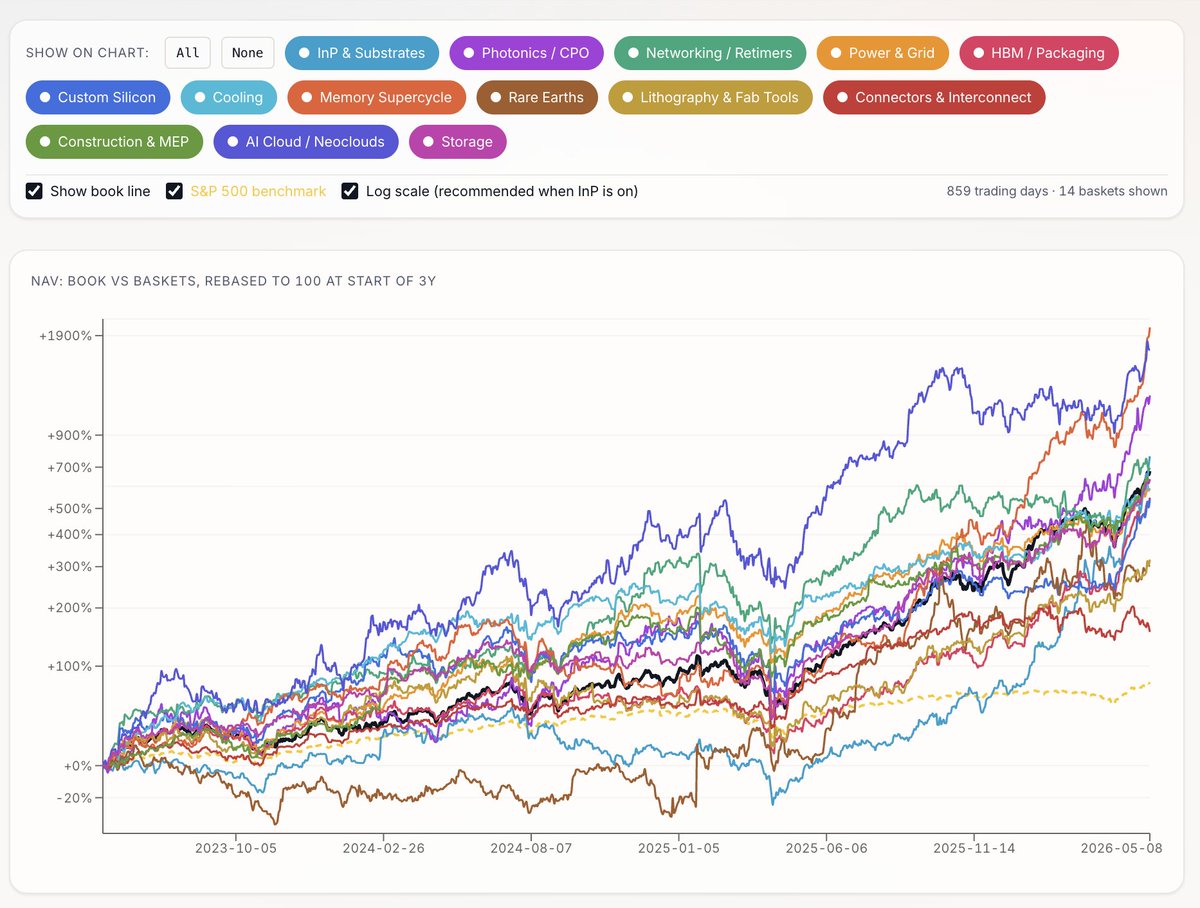

S&P 500 (in yellow): +31% over the last year.

The AI bottleneck book I have been keeping: +348%.

All 96 names green. That is the gap between buying AI stocks and buying the parts AI cannot ship without. The market is starting to learn the physical bill of materials for intelligence.

The companies are sorted into 14 baskets that map the physical AI stack: substrates, photonics, HBM, packaging, memory, power, cooling, storage, retimers, fab tools, construction, neoclouds, custom silicon, rare earths, and connectors.

All of it built around one question: if AI keeps scaling, where does the factory break first?

A year ago, the obvious AI trade was the visible part: GPUs, power, data centers, networking, maybe cooling. The tape has been moving somewhere more specific. Memory leads the 1Y.

InP and substrates sit right behind it.

Photonics/CPO and HBM/packaging follow.

Then storage, custom silicon, fab tools, construction, power, cooling, retimers, connectors.

The order matters more than the return. The market is no longer buying "AI infrastructure" as a single theme. It is ranking the layers that can make the AI factory late. That is the difference between AI beta and what is starting to look like bottleneck beta.

AI beta asks: who sells into AI. Bottleneck beta asks: if this layer is late, does the factory stop. The first question fits a pitch deck. The second fits a route card.

A month ago, the clean version of this was InP. GPUs need optical transceivers. Transceivers need lasers. Lasers need indium phosphide substrates. The substrate is a small physical disc sitting underneath one of the largest infrastructure builds in history.

That was why $AXTI worked. Tiny disc. Huge system. Real bottleneck. But $AXTI did not stop mattering. It stopped being lonely. Over 3 months, InP led the tape. Over 1 month, InP is still leading, but memory, photonics, custom silicon, and HBM/packaging have clustered right behind it.

The market is no longer only buying the raw ingredient. It is buying the stations that turn the ingredient into throughput. That is not a rotation out of InP. It is a rotation into the route card. Substrate to epi. Epi to laser. Laser to optical engine. Optical engine to package. Package to HBM. HBM to system. System to tokens.

$AXTI is the substrate station.

$VECO is the laser-tool station.

$LITE, $COHR, $MXL, and $AAOI are the photonics layer.

$MU, $SNDK, and SK Hynix are memory.

$TSM is base dies and advanced packaging.

$AMKR, ASE, and KYEC are OSAT.

$ONTO and $CAMT are inspection and metrology. $BESIY, $KLIC, and TOWA are bonding, attachment, and molding.

$ALAB and $CRDO are the retimer fabric that lets all of it talk.

These are not separate stories. They are one object moving through the factory. The next layer is probably not just HBM. Everyone has found HBM. The next layer is what makes HBM usable. A stack of memory dies is not memory yet. It has to be bonded, molded, inspected, cooled, and tested. It has to survive heat, pressure, warpage, microbumps, underfill, substrate flatness, and burn-in. Before HBM becomes bandwidth, it has to become a manufactured object.

That is where the watchlist is moving next. ABF substrates. T-glass. OSAT capacity. HBM base dies. Hybrid-bonding metrology. Bonders. Molders. Dicers. Thermal. And eventually EUV.

The scarce thing keeps getting more specific. First the chip. Then the package. Then the memory. Then the optical link. Then the substrate under the laser. Next, the mold around the memory stack, the metrology tool checking the bump, the glass that keeps the package flat.

The market is not walking from InP to HBM. It is walking with the part. Station by station.

Dashboard is public, link below.

(not financial advice)

What is the smallest object that, if it stopped being made tomorrow, would freeze the entire AI industry by Friday?

Not a chip. Not a GPU. Not a model.

A polished piece of indium phosphide the size of a coaster, grown in a furnace over two weeks, made by exactly two companies in the world that are not Chinese.

I learned that around 4 a.m. one night about two years ago. I have not really stopped thinking about it since.

To understand why a coaster of crystal can hold up a trillion-dollar industry, you first have to understand that almost nothing about modern computing is normal.

A leading-edge AI chip travels through roughly a thousand process steps over three to four months. The cleanroom it lives in is thousands of times cleaner than a hospital operating room. The fab itself draws as much electricity as a small city. The single lithography machine that draws the circuits has five thousand suppliers of its own, spread across six countries, and not a single nation on Earth could build one alone. By the time a finished chip pops out the other end, more humans have had a hand in its production than live in most American towns. Most of them will never meet.

From the highway, a TSMC fab looks like a beige warehouse with a parking lot. Inside, it is the closest thing humans have ever built to alien technology.

I find that genuinely moving. And I find it terrifying. Because a miracle that complicated has a lot of single points of failure, and almost nobody in mainstream coverage is mapping them.

Two years of pulling on this thread keeps bringing me back to the same conclusion. The 2026 to 2030 AI buildout is gated by four physical constraints, and almost nothing else.

1. Indium phosphide wafers. Two credible non-Chinese suppliers in the world.

2. Advanced packaging. Four companies on Earth that matter.

3. Power. Industrial gas turbines sold out into 2030. Three vendors at scale.

4. Critical minerals. China's pause on gallium, germanium, and antimony export controls expires November 27, 2026.

By the time a chokepoint is on the front page, the move is largely over. The prize goes to whoever was patient enough to map the chain when it was boring.

So I built a dashboard

A free public dashboard. The chokepoints, the names that own them, the live prices, the catalysts, and the written thesis all on one screen. No login. No newsletter. Not a portfolio. Not a recommendation. A prism.

I wanted it free because the people I would have wanted to read this when I was younger could not have afforded a Bloomberg terminal. Students. Engineers. Journalists trying to understand what they are writing about. Retail investors tired of being sold someone else's conviction. Curious teenagers in countries where the local financial press is twenty years behind the actual frontier.

The chain deserves to be walked. That is the whole invitation.

links below 👇

Educational, not investment advice.

Interview with Nebius Co-Founder Roman Chernin

Please like & share this video so that all $NBIS investors on X will see it! :)

If you prefer watching on YouTube: https://t.co/lGwhArC8MS

Timestamps:

00:00 - Why AI Infrastructure Is So Hard to Understand

00:24 - Market Fragmentation and What Actually Differentiates Providers

01:30 - Consolidation, Segmentation, and the Future AI Cloud Landscape

02:56 - What Analysts and VCs Still Get Wrong About AI Infrastructure

05:34 - Nebius Cloud: Product Readiness and Customer Proof Points

07:42 - Why Inference Workloads Are Exploding

09:11 - Training vs. Inference: How AI Models Actually Reach Production

10:10 - Why Inference Market Share May Concentrate Around a Few Winners

12:36 - Customer Use Cases: Coding, Enterprise AI, and Real-World Adoption

14:01 - Why Integrated Training and Inference Matter Strategically

16:01 - Building Scalable AI Infrastructure With High Utilization

18:24 - Token Factory: Inference as a Managed Service

20:24 - Revolut Case Study: AI-Driven Product Enhancements

22:56 - Token Factory Performance Optimization and Competitive Advantage

25:07 - Scale, Capacity, and Efficiency as Growth Drivers

28:36 - Why Inference Capacity Could Become the Next Major Bottleneck

30:10 - How Nebius Benchmarks Performance Across Providers

33:14 - The Future Size and Shape of the Inference Market

36:38 - Value-Based Pricing: Moving Beyond Cost per GPU Hour

40:55 - How Nebius Wins Deals: Quality, Performance, and Customer Experience

44:53 - Autonomous AI Platforms and the Rise of Agent-Based Models

47:28 - Tavily, Agentic Applications, and the Next Layer of the AI Stack

50:45 - Strategic Trade-Offs: Scaling, Product Roadmap, and Customer Relevance

55:40 - Final Thoughts: Adapting to the Next Shift in AI Workloads

@nebiusai@romanchernin

$MU $SNDK Amazing talk where Dylan says memory prices will still double or triple from here. Here's the transcript -

"Memory can only grow capacity low double digit percentages a year - 20% to 30% a year - even less for NAND, a little bit higher for DRAM.

"Even though the demand signal was very strong at the end of 2025, and the memory companies immediately sort of started reacting, none of that incremental capacity really gets here until the second that they've decided to do in addition to the typical 20 to 30%. You know, they can stretch a little bit, but really the true incremental supply doesn't come till 2028, which is a very unique thing. Even if they wanted to build as fast as possible, it doesn't come till 28 uh early late 27 at best.

"And so the result is memory prices have, you know, gone through the roof. And guess what? They're going to double and triple again. Um, at least on DRAM especially, people are like, "Oh, the memory storage is overplayed. Everyone gets it." And it's like, "No, no, no. You don't get it."

"DRAM will double or triple from here still because that's that's how much capacity is required and they have to steal capacity from somewhere else. And the only way to steal capacity from somewhere else in a in a capitalist economy is demand destruction via higher pricing. We're not like rationing stuff here. And so ultimately, that's what's going to happen. And so margins continue to go up."

$NBIS More enterprises are finding out that you cannot use Claude for everything. You need to prioritize uses cases and let the rest run on open source to make the business model work. Nebius CBO Romain already told you this half year ago. It’s part of the Nebius thesis.