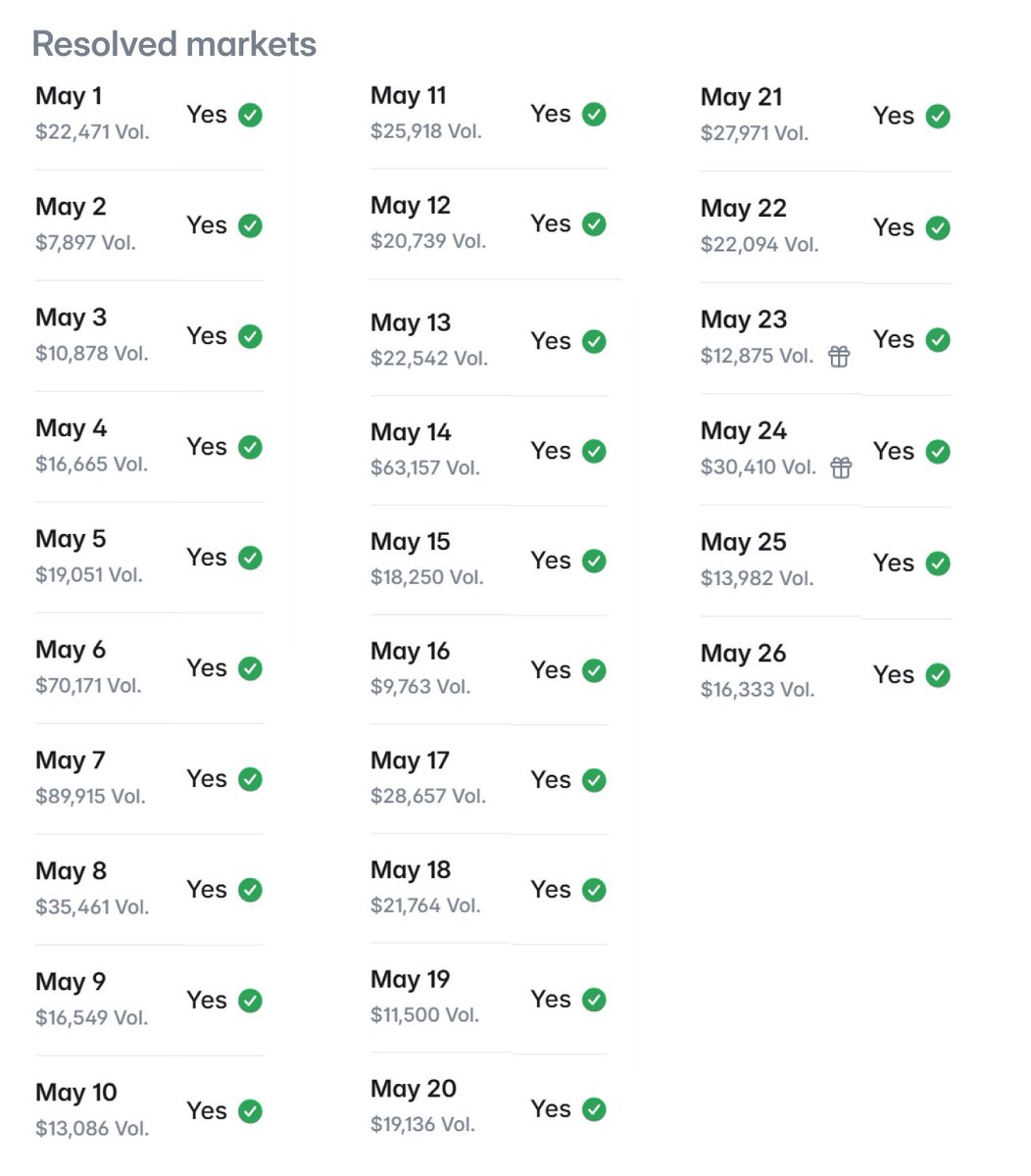

I'm not making this up

There's a market on which day Trump will insult someone

And every day in May resolved to "Yes" so far.

30 days of insults lol

literally the best investment you can make

back in April i bought $100 on each day

Pre Market Brief—Thursday, May 29

SPX −0.1% NDX −0.3% RTY −0.2% WTI $90.67 Gold $4,395 Silver $73.36 10Y 4.493% VIX 16.71

Yesterday the market spiked on a headline that Iran had received an unofficial MoU with terms for reopening the Strait of Hormuz. Trump refuted it within the hour. Oil finished near its session lows anyway. The market's reaction to the denial told us more than the headline did—the underlying bid for a deal is structural, not reactive, and it did not leave when the headline was walked back.

Overnight the script returned to escalation. The US struck Iranian military sites again, calling them purely defensive strikes to maintain the ceasefire. Iran's Revolutionary Guards responded by targeting a US airbase. US Central Command shot down four Iranian drones near the Strait and struck a ground control station in Bandar Abbas.

Brent crude added more than 3% to $97. WTI is up at $90.67 this morning.

KOSPI snapped its four day winning streak, falling 0.5% to 8,185.

NKY fell 0.5% to 64,693.

And yet the S&P futures are only down 0.1%.

The market has seen this pattern enough times now that it is treating fresh strikes as noise rather than signal—which is either sophisticated or complacent, and the difference between those two things is whether a deal actually comes.

The number from Japan that deserves more attention than it is getting—exports to the Middle East fell 55.8% in value y/y in April. Cars. Steel pipes. Industrial goods.

That is the SoH closure showing up as a concrete economic cost in real trade data. The conflict has been priced as a financial market event. It is becoming a real economy event and Japan is the first major economy showing it in the official data.

The session yesterday confirmed the Software rotation is real. Semis were sold— $SOXX profit taking after moves that included $MU +19.3%, $DRAM +14.6%, $EWY +10.2% in recent weeks. Software was bid post earnings.

It is too early to call the top in Semis— $AVGO reports next week and that print could provide another leg—but the RSI on Korean tech is at all time highs, levered Korea ETFs are showing concerning technicals, and the incremental dollar argument for adding Semis here is genuinely difficult after those moves.

The rotation from $SOXX into $IGV is not a bearish call on AI. It is a sensible expression of the same theme at better relative value.

Today's session has two things competing for attention.

PCE at 8:30am ET is the macro print—I expect core up 0.25% m/m, taking the y/y rate to 3.3%.

The 1Q GDP revision lands at the same time alongside Durable Goods and Jobless Claims.

The honest read is that today's PCE matters less than next month's CPI given where the conflict stands—what matters is whether the energy price surge from the past three months starts bleeding into core inflation in the May and June data.

The yield curve is bear flattening this morning with yields up 1 to 2 basis points, which is the technical headwind for Cyclicals and broadening—a steeper curve supports Discretionary and Financials—a flatter one pushes money back toward Tech. Watch the curve after PCE.

Earnings today— $DELL is the print that matters most for the AI infrastructure read through.

$COST gives the cleanest consumer signal of the group.

$ADSK, $MDB, $OKTA, and $PATH extend the Software earnings window that opened favorably last night. If Software keeps delivering, the rotation out of Semis into $IGV names accelerates through June.

Tomorrow's Tokyo CPI at 7:30pm ET is the next event risk nobody is pricing correctly. The Japan PPI shock two weeks ago broke global bond markets for three days. If Tokyo CPI comes in hot, that sequence repeats. That is the tail risk going into the weekend.

The position is still bullish. Trim Semis into strength—not a bearish call, a risk management one. The Hormuz reopening trade stays on in Cyclicals but the yield curve needs to cooperate. Copper is the structural long…