Nicolai Tangen, CEO of Norges Bank Investment Management pressed IBM CEO Arvind Krishna directly on whether AI is a bubble (Save this).

And Krishna responded with what has become known inside financial circles as the $8 trillion math problem.

A single gigawatt of AI data center capacity filled with accelerators, liquid cooling, and power infrastructure costs roughly $60 to $80 billion to build and populate.

The industry has committed to more than 100 gigawatts of buildout globally.

That is $6 to $8 trillion in capital expenditure and because AI grade hardware depreciates on a five-year cycle, that entire sum must be effectively replaced and refreshed every five years.

To service the interest on $8 trillion in capital at a conservative 10% borrowing rate, the AI ecosystem would need to generate approximately $800 billion in annual profit, a number that currently exceeds the combined net income of every large technology company in the world.

Goldman Sachs estimates $7.6 trillion in aggregate AI CapEx between 2026 and 2031 alone, and Reuters Breakingviews has flagged that even if the capital is available, physical bottlenecks power permits, land, cooling infrastructure, and electrical grid connections mean that half of the planned data center projects are being cancelled or delayed before they ever go live.

Krishna also raised a second, structurally distinct concern that markets have largely ignored.

He argued that the largest foundation models, GPT, Gemini, Claude, Llama are converging toward commodity status.

When a product is a commodity, switching costs collapse.

When switching costs collapse, pricing power evaporates and margins compress regardless of how much capital was spent building the capability.

Morningstar's equity research team conducted a review of 132 technology companies in 2026 and found that AI had caused moat rating downgrades across roughly 40 major stocks concentrated in enterprise software, IT services, and SaaS with Adobe, Salesforce, Workday, and ADP among the companies whose competitive moats have materially weakened.

The implication is that the companies spending the most on AI model development may be building an asset that is simultaneously the most expensive to produce and the most difficult to monetize with durable margins.

This bear case is serious but it is also incomplete and that is what makes Krishna's framing so important to understand precisely.

When pressed further, Krishna explicitly said he does not believe there is an AI bubble in the technology itself only in a subset of the infrastructure capital that is being deployed against speculative assumptions rather than proven demand.

He draws the same analogy, the fiber optic overbuild of the late 1990s. Dozens of companies went bankrupt laying cable that nobody was using.

And yet that exact "wasted" infrastructure became the physical backbone of every cloud company, every streaming service, every mobile network, and every modern AI training cluster that followed.

The builders lost, the infrastructure won.

And the companies that were built on top of it, Amazon, Google, Netflix, Salesforce compounded for two decades.

The question, as Krishna framed it, is not whether AI is real.

It is which capital deployment earns a return versus which gets stranded and crucially, whether you own the stranded assets or the companies built on top of them.

On winners, Krishna was direct that distribution is the moat on the consumer side, and enterprise is wide open.

The data supports this, Meta with 3.3 billion daily active users across Facebook, Instagram, and WhatsApp is building AI into a distribution network that no startup can replicate at any cost.

Meanwhile, the productivity evidence arriving in real time is beginning to challenge the bear case's revenue projections.

Jensen Huang just showed on stage at Computex that GitHub commits, the universal measure of global software output nearly tripled in the first months of 2026, effectively converting $3 trillion in developer salaries into $9 trillion in productive output.

That is measurable, real time economic value already flowing through the system and it feeds directly back into token demand in a compounding loop that Krishna's static CapEx math does not fully capture.

Never in the field of human commerce has so much been promised to so many from so little.

My May column for @barronsonline . . .

https://t.co/eoV9tMZPwn

“I think we have more referees than we have risk takers. More lawyers and regulators and others saying ‘you can’t do that, that’s too risky’ than people willing to innovate.” — @WalterIsaacson in conversation with @lexfridman about @elonmusk

More builders, less hall monitors.

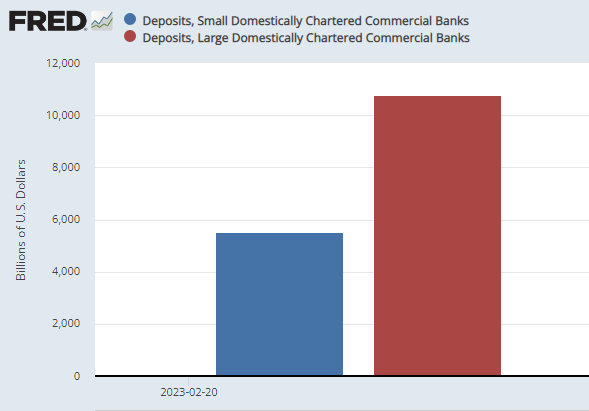

Fed/FDIC decisions on SVB determine whether they risk a bank run trillions of dollars in size.

1/3 of US deposits are in small banks and ~50% are uninsured. Haircutting SVB depositors will raise sensible questions about holding deposits at any small bank, risking a broader run.

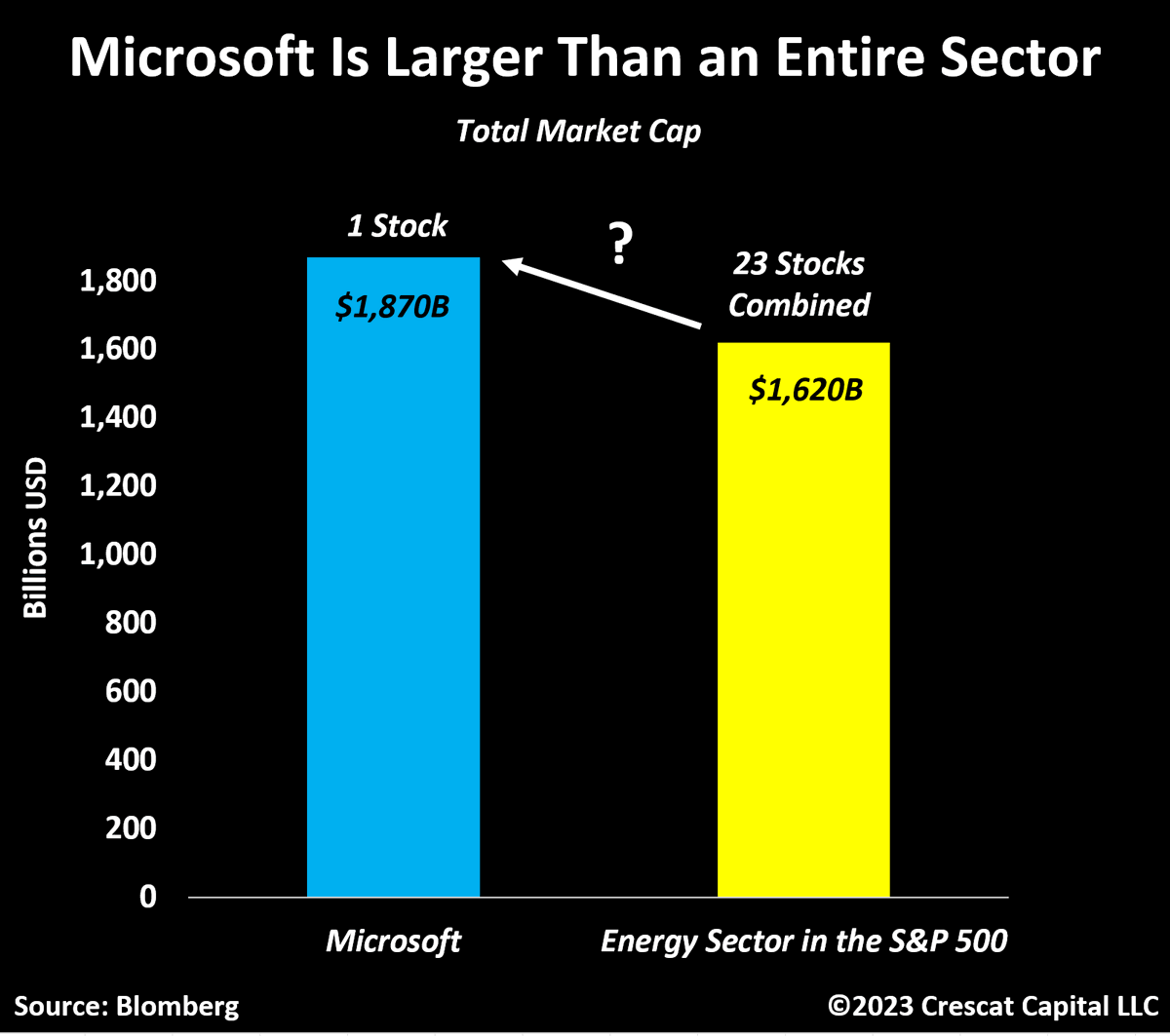

Microsoft still has a higher market cap than the entire Energy sector in the S&P 500 today.

Keep in mind:

Exxon *alone* produces just as much annual free cash flow as $MSFT today.

And no, this is not just a specific case with $XOM.

All the energy companies in the S&P 500 are profitable on a free-cash-flow basis today.

Either tech companies are still too expensive, or energy stocks remain a bargain… or both.

Here is the yield change in the UST market over the past 3 months:

Two Year: Down 54 bp

Five Year: Down 83 bp

Ten Year: Down. 71 bp

Thirty Year: Down 59 bp

Fed Funds: Up 75 bp

Message seems clear.

@LynAldenContact Incredibly insightful, many thanks. As stagflation seems to be here to stay, any reason why you’re not investing more in gold and gold mines? + any view on why gold hasn’t taken off yet?

@AlbertBridgeCap@Jack_Raines Reminds me of this bumper sticker we used to see everywhere (not anymore). Fact: Germany’s CO2 emissions per capita is about 10t/year vs just 5t for France (who derives about 70% of its electricity from nuclear energy).

@Frank_Giustra This is so true. Seems like 13 years of an unprecedented bull market led by growth stocks is making J Grantham warning fall on deaf ears. @Frank_Giustra, I’d be curious to hear about your latest views on gold, thanks!

@BoyanSlat@TheOceanCleanup I’ll watch them every week, just to remind me that some AWESOME people like you are are actually DOING concrete/innovative things to try to save our planet.