$OUST compared to $ASTS

Deep sell 17 candlesticks after the local bottom for $ASTS. We bottomed about a month after $OUST - can we learn anything?

Weirdly, $OUST also had a nice sell on the 17th candlestick. Both tested the daily 8ema on this candlestick. Both had just roughly doubled from that low point. Not as bad a sell or as catalyst-driven for $OUST, but semi-notable.

$OUST then flopped around for another 12 candlesticks, including retesting that local high, before establishing a higher low at more/less the 78.6% fib level (30 to 23.6). We're another 14 candlesticks past that and still making new highs. $OUST hit basically a triple from the original low in question today.

10 more candlesticks brings us to SpaceX IPO Friday. It is feasible we go test low 130s again on Mon-Tues and then have a grindy sell down to the same 78.6% fib level. That would be around (you guessed it) 105. Maybe we go lower idk. And, given today's price action, maybe we already hit that higher lower and can just keep going full steam ahead! No 12 days required. That would then bring us to roughly 190 as the "triple" target off the original low in question. That's a pretty big overshoot of the ~$170 implied by my purple channel, but not outlandish imo.

Does this hold water? Honestly, probably not, but it seems eerily applicable.

I've been fascinated with the staggered symphony of chart breakouts amongst laggards and last year's favorite. Would like to apply similar thinking for $UUUU, $QS, etc. If it works, I'll be looking for other fuzzy situational applications.

$LNZA holds a 8% stake in this JV.

That part is worth $75M currently.

Lanzatech market cap: $65M.

Not to mention the 50% stake lnza got in lanzajet.

Many millions behind the curtain.

$LPTH Adding this to the list of news that could lead to a meaningful tailwind for Lightapth's industrial coal furnace cameras.

https://t.co/3mJPQ6E8l5

https://t.co/cy7sbxEYDl

Winners for most egregiously surprising charts that I have no/minimal exposure to at the moment are $UUUU and $LDOS. No idea why they are where they are. I'm hoping to roll gains into those names if things play out.

Taking out the 8ema on hourly charts one by one. It's slowly letting averages come down to provide support on the way back up.

99-101, then 109-111, then ?????????

Finding extreme value in NOT jumping around names when I am already quite happy with my core stable of names

Conviction pays! You don't get shaken out and you learn how to pinch you nose and do the thing.

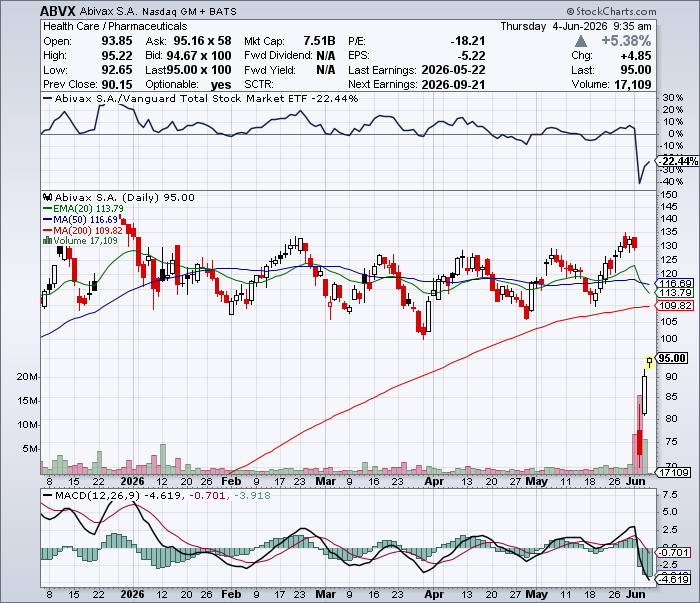

Passing on $ABVX at this valuation is equivalent to passing on buying it at $55 in the post-market following the induction data readout.

The market is getting a second chance at the same mistake.

Here is the question the market will answer over time: what is the right value for what may be the best UC drug ever developed? Obefazimod appears to be a safe, once-daily oral therapy with no pre-prescribing burden, no meaningful ongoing monitoring burden, a unique mechanism of action, and exposure to what should become a ~$20B IBD TAM?

The answer is likely more than ~$7B.

Let’s put this in perspective: ~$7B is roughly what Pfizer paid for etrasimod before the Phase 3 UC data read out, which was a second-in-class S1P modulator behind ozanimod, with weaker efficacy, QT-related considerations, ECG screening, monitoring burden, and a less differentiated commercial profile.

So what is capping the stock today?

Outside of the cancer debate, based on conversations with market participants, the current pushback appears to be that there is “no catalyst.” They appear to have missed there is a major safety update expected by the end of this month that should nearly double the total patient-years of obefazimod safety exposure.

I know pods have short-term thinking, but three weeks does not seem that far away when the next dataset has the potential to directly address the central bear case.

That matters because the current bear case is safety. If the upcoming dataset continues to show that the malignancy rate is in line with UC background risk and non-JAK UC comparators, it should materially reduce the central sentiment overhang on the stock.

That is the broader setup. The market appears to be treating the June 1 safety update as a structural impairment. That interpretation is wrong. These data now establish obefazimod as a potential frontline “prescribe and forget” oral therapy in UC which is a profile often hoped for and talked about in IBD and I&I more broadly, but rarely realized.

The concern around non-NMSC events reported on June 1 is overblown. The June 1 data update should strengthen, not weaken, the core $ABVX thesis. The 50 mg safety concern is best understood as a red herring when evaluated against pooled exposure, the elevated baseline cancer risk of a refractory UC population, and malignancy rates observed with other UC therapies that do not carry black box warnings. The more important signal is efficacy. The 50 mg dose remains highly effective, with potentially best-in-disease endoscopic remission data, while the 25 mg dose provides meaningful flexibility for chronic maintenance, labeling, and physician adoption.

The market reaction materially over-discounted safety-related risk, underappreciated the commercial significance of 25 mg / 50 mg dose flexibility, and failed to appreciate that the strength of the endoscopic remission data supports potential earlier-line use in UC while materially increasing the probability of success in Crohn’s disease. UC supports the base case. Crohn’s is the key upside driver for valuation.

The reported 50 mg obefazimod malignancy data should be evaluated in totality by combining the pooled 96-week Phase 2b dataset, which used the same dose and similar NMSC surveillance, with ABTECT Maintenance Part 1. The right question is not whether there were headline malignancy events. The right question is whether the rate looks out of line for a refractory UC population that is already at elevated risk of cancer, and whether it looks out of line versus other UC therapies that do not have black box warnings. On the totality of the data, it does not.

By construction, per regulatory convention, and consistent with standard practice in clinical IBD trials, dysplasia should not be counted as a non-NMSC malignancy event. Dysplasia is pre-malignant and, by definition, is not cancer. Such findings are also not uncommon against the background risk of longstanding ulcerative colitis. Including dysplasia as cancer distorts the safety interpretation and makes the 50 mg dose look worse than the data support.

There were two non-NMSC events reported in ABTECT Phase 3 Maintenance Part 1. There was one non-NMSC event reported in the ongoing Phase 2 series of trials. It is unclear whether this event occurred during the 96-week portion of the Phase 2 series, but conservatively counting it against obefazimod still yields an event rate of approximately 0.58/100 patient-years. This places obefazimod in the middle of the range across UC comparators, including ustekinumab, vedolizumab, etrasimod, ozanimod, and mirikizumab, none of which carry black box warnings for malignancy, and ahead of black-boxed JAK inhibitors, including upadacitinib and tofacitinib. That is not what a broken 50 mg safety profile looks like.

The safety debate is distracting from what should be the dominant interpretation of the update: the efficacy data are exceptional. Obefazimod has produced what may be the most impressive endoscopic remission dataset observed in ulcerative colitis, particularly after adjusting for how refractory the ABTECT population was. This was not an easy-to-treat biologic-naive UC trial. The study included substantial advanced-therapy inadequate responders and prior JAK inhibitor inadequate responders, yet the 50 mg dose still delivered a level of mucosal efficacy that appears best-in-disease or near-best-in-disease on a refractory-adjusted basis.

That is the point the market appears to be missing. RINVOQ likely remains the stronger acute induction/rescue benchmark, but upadacitinib’s pivotal UC trials did not face the same degree of prior JAK-exposed disease biology. For chronic maintenance, obefazimod appears highly competitive and potentially superior when adjusted for baseline severity, with particularly strong endoscopic remission and corticosteroid-free remission performance. A non-JAK oral drug delivering this level of mucosal efficacy in this population is not just “strong data.” It is a potential frontline-enabling efficacy profile.

This is what creates the frontline “prescribe and forget” opportunity. Community GIs manage many moderate UC patients before they become severe or refractory. A clean 50 mg profile would offer a rare combination: enough efficacy to keep moderate UC patients controlled, and enough safety comfort that physicians do not feel burdened managing the drug. Oral dosing, strong efficacy, no infusion logistics, no JAK-label discomfort, and minimal incremental workflow burden create a practical profile that community physicians can use earlier. The larger opportunity is not merely post-biologic / pre-JAK positioning; it is post-generics / pre-biologics use by physicians who want an effective, low-friction oral option.

The 25 mg dose further strengthens this profile. It is not a rescue thesis; it is a strategic advantage. It provides flexibility for chronic maintenance, labeling, and physician adoption, while preserving 50 mg for induction, higher-need patients, or flex-up dosing. A commercially viable regimen could mirror the established IBD treatment paradigm used with RINVOQ: higher-intensity induction followed by lower-dose chronic maintenance. In practice, patients could receive 50 mg obefazimod induction or JAK induction followed by 25 mg obefazimod maintenance, with the ability to flex back to 50 mg in selected patients who require additional disease control.

This preserves the key commercial attributes of the asset: potent induction optionality, a lower-exposure 25 mg maintenance backbone, oral dosing, dose flexibility, and strong mucosal efficacy. A potential 50 mg chronic-label limitation should therefore be viewed as a manageable dosing/labeling issue rather than a thesis-breaking safety problem. If the practical regulatory choice were between preserving broad 50 mg chronic dosing at the cost of a black box warning versus adopting a cleaner regimen of 50 mg induction and/or selective flex-up with 25 mg maintenance, the rational commercial strategy would be to prioritize the label that maximizes broad chronic use, physician comfort, and adoption.

Even if, for the sake of argument, obefazimod ultimately received a black box warning, the asset would still not be broken. RINVOQ is black-boxed and still represents a multi-billion-dollar IBD product. That creates a reasonable downside commercial anchor for obefazimod: constrained label, not zero. In that scenario, obefazimod could still have a role in the post-biologic / pre-JAK setting, and potentially as maintenance after RINVOQ induction or after 25 mg / 50 mg obefazimod induction. If obefazimod is viewed as safer and more effective in maintenance, it could still be used ahead of RINVOQ for chronic disease control in selected patients.

But the Crohn’s readthrough is the major upside driver, and the headline of the maintenance data should have been "Crohn's now appears largely de-risked".

Can anyone think of a therapy that produced this degree of mucosal efficacy in UC and then failed to work in Crohn’s?

Tofacitinib is the closest example, but it is not a close comp: inferior mucosal healing, a much easier-to-treat UC population, and a JAK mechanism with a very different safety and commercial profile.

The point is not that UC success guarantees Crohn’s success. It does not. The point is that a non-JAK oral drug producing this degree of mucosal efficacy in a hard-to-treat UC population should materially increase the prior probability of CD success. Above a coin flip certainly seems reasonable given prior UC to CD translational examples, and we would venture should be closer to 75%, but regardless, meaningfully above where the market appears to be underwriting it today.

That makes Crohn’s a real valuation driver today, not a free option worth zero.

Global peak obefazimod sales can be reasonably framed at approximately $3.5–5.0B in ulcerative colitis alone, with upside to $6.0–10.0B if Crohn’s disease is successful. On a risk-adjusted basis, assuming a high probability of UC approval and a 66% probability of success in Crohn’s disease, a reasonable underwriting range could be approximately $4.5–6.5B in global risk-adjusted peak sales across IBD. There is additional upside approaching or exceeding $10B globally if the safety profile remains benign and the drug moves into frontline or earlier-line UC/Crohn’s use.

The UC-only case is supported by a differentiated profile: oral once-daily dosing, strong maintenance efficacy, robust endoscopic remission, potentially cleaner chronic safety, 25 mg / 50 mg dose flexibility, and a refractory-adjusted efficacy dataset that compares favorably with leading advanced therapies.

The base case is that obefazimod remains a multi-billion-dollar IBD asset. The downside case is a narrower 50 mg maintenance label, a 25 mg-centered chronic-use strategy, or even a constrained/black-box label, which remains commercially manageable and still anchored by a RINVOQ-like IBD revenue framework rather than zero. The upside case is a clean label, earlier-line UC positioning, community-GI adoption in the post-generics / pre-biologics setting, and successful Crohn’s development, which could support global peak sales toward the high end of a $6–10B range.

To sum it all up: The risk/reward appears highly attractive because the market is focused on a worst-case interpretation of the 50 mg safety signal while failing to credit the durability, mucosal efficacy, Crohn’s readthrough, and commercial flexibility of the 25 mg / 50 mg profile.

Layered on top of that is fast short money arguing there is “no catalyst,” despite a major safety update expected before the end of the month that should add a truckload of patient-years and directly address the only real bear case.

If that dataset is clean, the debate should quickly shift from “is 50 mg impaired?” to “why was a potential best-in-disease oral IBD drug, now post-pivotal UC data, ever valued below inferior IBD assets acquired before their Phase 3 readouts?”

Disclosure: May hold or trade securities mentioned, including $ABVX, and views/positions may change without notice. Not investment advice.

$AVAV 🚨The Drone War Went Global, and AI/ Autonomy Is the Future of Modern Warfare. Wall Street Cut Its Best Stock in Half. Why AeroVironment Is a Screaming Buy🚨

A $75B drone budget. Golden Dome. Lasers, swarms, counter-drones, and the AI that runs them. The Trump admin in talks to fund the makers directly. Down 50% From Its High.

🔥A KEYNES RESEARCH MEGA Deep Dive on How AeroVironment Becomes a $500+ Stock🔥

Here is the trade: the biggest shift in how the world fights wars in forty years is happening right now, the United States is about to spend generationally to win it, and the single public company that builds the entire arsenal of that new kind of war is trading 50% below its high on a one-quarter stumble. This thread is the case for closing this disconnect and why this stock is headed much higher.

AeroVironment $AVAV makes the attack drones, the kamikaze loitering munitions, the jammers that knock enemy drones out of the sky, the lasers that burn them down for a few dollars a shot, the cheap interceptor missiles that kill what survives, and the battlefield AI that ties all of it together. Ukraine and Iran have proved this is exactly how modern war is now fought, with cheap autonomous systems by the thousand, and the old world of exquisite jets and carriers cannot answer it economically.

With China as the biggest geopolitical rival ratcheting up the same capabilities, the Pentagon's FY27 budget requests roughly $75 billion for drones and counter-drones, the largest such investment in history and triple the prior year. Golden Dome, the biggest homeland-defense program ever conceived, runs through AV's lane. Executive orders mandate American-made drones and hand the domestic market to US suppliers. The Trump administration is in talks to fund the makers directly, with AV named in the reporting. National security is calling, and it is calling AV's exact phone number.

$AVAV is a profitable, scaled, number-one-or-two player sitting at the front edge of five inflecting markets at once: drones, counter-drones, directed energy, space, and the highest-margin prize of all, military AI and autonomy. It is the only public, profitable way to own the full kill chain.

So why is it 50% off? Because one quarter slipped. A government shutdown pushed orders to the right, a shipping snag shoved high-margin revenue into the next quarter, and the company took a non-cash write-down on a single space contract. The market read a miss, a guide-down, and an accounting charge in one print and hit sell. Meanwhile the things that actually predict the future got stronger: funded backlog grew to $1.1 billion, year-to-date awards hit a record $4.6 billion, and management says it has 98% visibility to its guidance and a record fourth quarter coming. The demand underneath the stock accelerated.

That is the setup I have been waiting for on this name. Over the next sections I will run the geopolitics, break down the full weapons stack layer by layer, make the case that the AI and autonomy story is the most underrated part of the whole company, flush out the space business and Golden Dome, stack AV against above $500. The stock was already at $418 last October on a smaller base, so a recovery to those levels is a return to recent ground, and the path beyond is incredibly bullish.

Let's GO 🧵