@chigrl I have recently ordered 7 lbs. beef from @RattlesnakeMeat (Starter box) in Kansas and 9 lbs. from @ParkerCoBeef (individual cuts) in Texas. Rattlesnake shipped in 1 day, better dry ice packaging. Parker shipped in 2 weeks, yet beef a bit more tender. Both fantastic family farms!

The precursor to the investor immigration program to the one proposed by President Trump as the “Gold Card” for $5M today has been in place since 1990, introduced by President Bush Senior. President Trump effectively raises the price by 5x.

Under the current EB-5 Program, investors invest $1,050,000 in a U.S. company and create 10 full-time jobs for U.S. workers in exchange for a Green Card.

Friend of mine got his Green Card that way in 2003, as his parents set up the U.S. branch of their German medical devices company in Florida and created 150 jobs near Jacksonville.

https://t.co/LXsvvpT245

Grok 3 is pretty incredible! I was genuinely curious if there was a way to recreate dinosaurs, and learned that starting from a Southern Cassowary, we could reasonably get to a docile Velociraptor in 3-6 years.

@xai team, you have truly outdone yourself!

https://t.co/ldVTlTCdxj

@badcharts1 And if you are looking to baseline, Patrick, DOGE publishes aggregate and department level federal workforce stats for the U.S. executive branch, incl. headcount plus salary histograms and averages that may be of use to you.

https://t.co/StkaT2qd2N

@TheKingCourt And isn’t it funny how coincidentally a week after the original ban of the TikTok app in the US went into effect, we got a new Chinese app topping the app stores that users are racing to install on their phones to expose their hearts’ desires?

@chigrl Informative article, Tracy, thank you! I had no idea that nuclear control rods use above 1 million ounces of silver per year.

While only 1/1000th of global silver production p.a. (going by Silver Institute), every ounce counts.

https://t.co/A9Zd66O5pl

https://t.co/4SebWNwZ4s

@dailydirtnap@donnelly_brent That’s quite the Economist cover the week before the BRICS Kazan summit!

Might be time to brush up on the UNIT white paper (https://t.co/wKah0dgNQx) over the weekend that lays out a 40% gold, 60% local currencies basket that its Russian/Chinese authors see a BRICS+ use case for.

@badcharts1@Cole73James On linear scale: Looks like miners just broke out vs. gold

On log scale: Looks like miners still need some time to break out vs. gold

@badcharts1, did I do this right?

Unfortunate for the West, China front running uranium as another commodity category, similar to gold recently: in past 2 years, China added 85M lbs, US 2M lbs, EU less than 2M lbs of uranium inventory (UxC data). 47% H1’24 Kazakh uranium sales went to China.

FYI @hkuppy@TgMacro

👨🏫This weekend I was asked by a Wall Street #investing guru, who has a large global following of institutional investors & fund managers, to provide my updated take on the #Uranium bull market case as it stands today.📄🐂 ICYMBI, here's my submission:👇

The World #Nuclear Association's annual symposium has just wrapped up in London. The event was sold out for the first time, making it the largest Nuclear and Uranium industry gathering in the WNA's history.😃 Meetings and presentations were focused on how to best harness the rapidly growing global support for Nuclear #energy in order for the Nuclear industry and supply chains to fulfill the COP28 pledge to triple Nuclear capacity by 2050.⚛️🏗️🌏 Global decarbonization goals coupled with greater emphasis on achieving 24/7 #CarbonFree #EnergySecurity are driving a resurgence not seen since the 1970's.🌞

Demand Signals

China just approved construction of another 11 reactors for a total of 46 new builds approved in the past 5 years. Most of the 46 reactors in China's construction pipeline(55GW) are identical copies that can be built in under 5 years thanks to the forethought of an expanded supply chain and workforce capable of building multiple identical reactors simultaneously. By 2030 China will have the world's largest nuclear fleet of 102 reactors producing over 113GW of zero-emissions electricity, consuming more than 56 Million lbs of Uranium per year, a near doubling of their current consumption in just 6 years. China told the WNA symposium that they plan to accelerate their build-out by approving up to 12 more reactors in each of the next 4 to 5 years. Their ultimate target is 150 operating reactors, tripling their uranium demand to 90 Million lbs per year.

China is also pressing ahead with plans to mass produce its 210MW HTR-PM "pebble bed" Small Modular Reactor that was recently tested to successfully confirm that it's "meltdown proof". It's designed as a drop-in replacement for coal-fired burners in China's 1,100 power plants that could be converted from coal to uranium fuel. HTR-PM SMR's are also being planned to replace coal-fired district heating plants that produce hot water that's distributed to homes and businesses in northern cities.

Nuclear fuel consultants UxC just released the 5th edition of their Global Nuclear Fuel Inventories report. It revealed that China is front-running Western fuel buyers, adding 85 Million lbs of inventory in the past 2 years as they look to secure Uranium fuel in advance of approving new reactor builds. Over the same 2 year period, US utilities saw a net increase of only 2 Million lbs, the EU less than 2 Million. Kazatomprom also just reported that 47.3% of Kazakhstan's Uranium sales in the first half of this year were purchases by China. Western fuel buyers have been asleep at the wheel while China has been buying up as much U3O8 as possible.

Russia just released a draft 2042 Energy Plan which calls for the construction of another 34 Nuclear reactors that will more than double Russia's Uranium requirements over the next 18 years, adding 18 Million lbs per year of new demand.

India's Minister of State has confirmed plans to triple India's Nuclear capacity from 8,180MW to 22,480MW in just 7 years by 2031-2032, aiming for 100,000MW by 2047. They now have 21 new reactors of 15,300MW in their construction pipeline. That's a 3-fold increase in Uranium requirements by the start of the next decade, a 12-fold rise by 2047. In addition, India launched a plan in its 2024/2025 Budget to deploy dozens of 220MW Bharat Small Modular Reactors under a new public/private partnership program. One of the world's largest steelmakers, Tata Steel, wants to make green steel using as many as 200 carbon-free Bharat SMR's that will produce hydrogen to replace coking coal.

In the USA the Nuclear Regulatory Commission has approved 20-year life extensions for 4 US reactors of 4.3 Gigawatts, adding 20 years of 2 Million lbs per year unanticipated Uranium demand. Upgrading and extending operating reactors has become the norm (excluding Germany) with life extensions approved this year in Canada, Spain, China, Japan, Belgium, South Africa, as well as for California's Diablo Canyon. For the first time in history, the US is working to restart a decommissioned Nuclear power plant with Holtec on track to bring Michigan's shuttered Palisades Nuclear plant back online by October next year. Plans are also underway to restart Three Mile Island in Pennsylvania and Duane Arnold in Iowa. Japan is in the process of restarting a 13th reactor that’s been offline since Fukushima.

Recent passage into law of the bipartisan ADVANCE Act has set the stage for the US to triple its Nuclear capacity with the addition of another 200 Gigawatts of advanced reactors. The expansion plan in the DOE's recent Liftoff report foresees an additional 110 Million lbs of US Uranium demand to 160 Million lbs per year versus US domestic mined supply currently sitting at less than 1 Million lbs produced in the past few years. Delegates at the WNA Symposium in London were told to expect announcements of new US reactor builds in the coming months.

Currently, the World Nuclear Association shows 439 operable reactors (396GW), 64 units under construction (71GW), 88 more ordered or in advanced planning (85GW) and another 344 reactors (365GW) proposed. The WNA estimates that operating reactors will consume 67,517tU (176 Million lbs U3O8) this year. Nuclear fuel consultants push that figure up to over 200 Million lbs when taking initial reactor coreloads (3X annual), inventory restocking and secondary demand from physical funds and other financial players into account. The most recent Uranium production figures available are for 2022 in which 49,355tU (128M lbs) were produced, meeting only 74% of basic consumption requirements.

As you know, the other wildcards on the demand side that have not yet been added to global demand models are the massive new demands for 24/7 reliable carbon-free electricity to power the AI revolution and giant data centers being planned in the US and worldwide, or the transition to electric cars, trucks, buses, and cargo shipping. Further to that, wind and solar can make no valuable contribution to decarbonizing heavy industry or producing green hydrogen. The 400GW of Nuclear electricity produced today is just the tip of the iceberg in the global decarbonization drive that is opening up many new applications for advanced Nuclear technology, fueled by Uranium.

Supply Signals

Uranium mining is hard. This year has seen several small mining operations restarting in the US, Australia, Namibia and elsewhere but they do little to correct the deep structural supply deficit that exists today. There's only one greenfield uranium mine under development right now, and it's facing delays and construction/financing challenges given it's situated in junta-controlled Niger in Africa.

Kazakhstan, where 39% of global Uranium supply is produced, has over-promised and under-delivered for the fifth straight year, slashing its 2025 production guidance by 17%, trimming output by circa 14 Million lbs below previous guidance, which reduces 2025 global supply to nearly 10% below expectations. Since peaking in 2016, Kazakhstan has produced >126 Million lbs LESS than fully permitted levels. They have no willingness or ability to flood the market with new supply.

And if that wasn't enough, they're seeking to LOWER permitted production levels for 2026 and beyond. Ongoing challenges in securing adequate quantities of sulphuric acid, and unforeseen wellfield construction delays, are making it impossible to achieve even -20% below permitted levels at some mine projects, so they are cutting them back in a "lower for longer" outlook. China accounts for over 47% of Kazakh Uranium sales in H1/2024 as they continue to fill their 60 Million lb secure warehouse at Alashankou on the border with Kazakhstan. On top of that, the government of Kazakhstan forced a deal on Kazatomprom that gives Russia 100% of production until 2027 from the only major new mine in development.

But that's not all..

On 10 July Kazatomprom announced sharp increases to Kazakhstan's Mineral Extraction Tax (MET) paid by Kazatomprom and its foreign Joint Venture partners for Uranium produced at the nation's 14 mining operations. A recently introduced 6% MET for 2024 will rise +50% to 9% in 2025 then double again to as high as 18% for the largest JV mining operations in 2026 and beyond PLUS an additional tax of up to 2.5% that will be added on top that is tied to the Spot price of U3O8.

In Kazatomprom's H1/2024 Half-Year Financials:

All-in sustaining cash costs up +45%

Capital expenditures up +64%

Corporate income tax up +81%

Mineral Extraction Tax (MET) up +104%

Other taxes & payments up +60%

The era of cheap lbs coming West from Kazakhstan is over! Cameco is now saying that the lbs they receive from their Inkai JV in Kazakhstan are no longer cheaper than mining those lbs in Saskatchewan. Any additional supply coming out of Kazakhstan is going straight into China and Russia anyway, leaving little for those Western utilities in the US and EU that have failed to build up sufficient inventory while waiting for the Kazakhs to ramp up production.. which hasn't and won't materialize.

Niger revoked the mining permit for French Orano's 550 Million lbs Imouraren, Africa's largest Uranium mine project that was expected to produce 13 Million lbs per year for 35 years to fuel reactors in France, the EU and USA... dead!

Niger also revoked permits for Canadian GoviEx's Madaouela mine project that was planned to begin production in 2025 of 51 Million lbs at up to 2.7 Million lbs per year for 19 years... dead!

In Australia, the termination of ERA's license for Jabiluka cuts nearly 300 Million lbs of potential future Uranium supply.

France’s $1.6 Billion Uranium mining deal in Mongolia is also in limbo, as the government has delayed moving forward as it debates protection of its strategic resources.

We're now approaching 1 Billion lbs U3O8 in cancelled Uranium mining projects this year that were expected to feed Western Nuclear reactors.

The new US law H.R.1042 - 'Prohibiting Russian Uranium Imports Act' took effect on August 12th as US customs agents began blocking shipments of low-enriched Uranium (LEU) into the US from all Russian entities, as well as from any other LEU supplier known to be a recipient of Russian LEU that may have been swapped or exchanged for Russian LEU in an attempt to circumvent the imports ban. To date, only 1 waiver is known to have been issued. It is a partial waiver to Centrus Energy allowing some imports into the US from Russia for orders already placed for delivery over the next 16 months up until 31 December 2025. From 2028 to 2040 a total ban goes into effect with no waivers to be granted.

On June 27th DOE issued a US$3.4 Billion RFP for purchasing a stockpile of Low-enriched Uranium (LEU) under IDIQ base contracts. DOE says the stockpile will be an emergency backup supply that will be sold to US utilities at fair market value as needed to replace LEU imports banned from Russia. The closing date for submission of proposals is 9 September. The LEU offered by suppliers MUST be enriched in the US by expanding or building new enrichment facilities inside the US, and MUST utilize mined/milled U3O8 produced in the US or an allied nation or partner (Canada, Australia, EU). At today's fuel cycle prices, $3.4 Billion would enrich about 27 Million lbs U3O8 that can only be supplied by US and allied miners.

Last week under the headline "A Nuclear Renaissance", French Orano announced that they are working with TVA to build a new US Uranium centrifuge enrichment plant in Tennessee at an estimated cost of $5.5 Billion. It seems likely this is aimed at securing a major contract under the DOE $3.4 Billion LEU purchase RFP. This announcement towards providing a secure "Made in America" Nuclear fuel supply for US reactors, while also supporting the proposed 200GW tripling of US nuclear capacity, erases all lingering doubts about there being a Nuclear Renaissance in full swing.

Listen to the Price Signals

The industry average price for Long-term contract Uranium, which covers 85-90% of mined U3O8 purchasing by Nuclear utilities, rose again in August to a new 16-year high of $81/lb, UP +37% in 1 year in a solid uptrend with not a single price pullback in 2 years!

We saw the month-end price for Spot U3O8 manipulated down to $78/lb in August as a trader dropped their Ask by $3 about 30 minutes before UxC pegged their August closing Spot price. Spot has since recovered back to $80/lb as carry traders stepped in to buy the cheap lbs on offer that they can sell into medium-term supply contracts at far higher prices. The Long-term price is providing a floor for the Spot price as the carry trade comes back to life.

Leading price indicators for U3O8: enrichment SWU and Conversion, continued to soar to all-time industry highs in August, signalling incoming demand for mined U3O8 to fulfill the feedstock requirements in swelling SWU and Conversion contract books. Conversion hit a new all-time record high of $70 last week, a 4.5X increase from $16 in January 2022, just before Russia invaded Ukraine. Enrichment SWU prices have tripled over the same period, also hitting new all-time record highs.

But, as the accompanying Citi research chart shows, the price for Spot U3O8 hasn't kept pace with SWU and conversion. Utilities normally sign contracts for the manufacture of reactor fuel starting with fuel assemblies then working backwards thru enrichment SWU, Conversion then finally ordering the mined U3O8 needed to feed the whole cycle as the last domino to fall in the contracts signing chain. SWU and Conversion price signals tell us that this bull market has many more years yet to run, with far higher U3O8 prices to come.

Nuclear fuel consultants UxC note there are on the order of 2.1 Billion lbs of U3O8 requirements out over the next 15 years that have not yet been ordered by fuel buyers. With mined Uranium production at around 150 Million lbs per year at present and real demand over 200 Million lbs per year, there is already significant upward pressure on long-term Uranium prices that have hit a new 16-year high. As that SWU price wave passes through Conversion and finally arrives at mined U3O8, Uranium prices WILL go substantially higher. Cameco recently stated that new contracts they are negotiating are Spot market referenced with price ceilings of around $130/lb or higher.

In the latest Uranium Macro update from analysts at Cantor Fitzgerald, they raised their price deck to Spot/Term prices of:

$120/$110 for 2024

$130/$120 for 2025

Cantor's Updated Uranium Supply/Demand Model, with all potential future sources of supply included, now indicates a sustained supply deficit from 2024 onwards into the next decade as there just aren't enough new mine projects financed, permitted and in construction to meet even today's known demand. That's not even factoring in the potential mass deployment of small modular reactors or power hungry data centers to support the AI revolution.

The long and short of it is that there no longer exists ANY pathway to a rebalanced Uranium market in this decade. A sustained structural supply deficit will lead to rising prices for many years to come. After a decade of severe under-investment in new mines, the glacial supply response cannot even hope to keep up with demand, no matter how high prices go.

Demand is rapidly outpacing supply. China alone is building large numbers of reactors in far less time than it takes to build a new Uranium mine to fuel them. Game.. set.. match.

@joshyoung China‘s oil piggy bank: their stockpiling of ~60M barrels oil works out to ~2 days of global OPEC production.

At China‘s ~17M bpd oil consumption, the stockpiled ~60M barrels equate to an extra 3.5 days of what China consumes.

https://t.co/IGNVhw6irQ

https://t.co/MOLFOK4QsG

Some points regarding the overnight Iranian missile attack on Israel:

1. Contrary to what pundits are saying, this wasn’t designed merely as “bells and whistles” with no damage.

When you shoot 350 flying objects timed to hit Israel at the same moment,

when you use three fundamentally different weapon types—cruise missiles, ballistic missiles and UAVs,

you’re looking to penetrate Israel’s defenses and kill Israelis.

2. The US administration is telling us: “This is a victory, you’ve already won by thwarting the missiles.

No need for any further action.”

No, it’s NOT a victory.

Yes, it’s a remarkable success of Israel’s air defense systems, but it’s not a victory.

When a bully tries to hit you 350 times and only succeeds seven time, you’ve NOT won.

You don’t win wars just by intercepting your enemy’s hits, nor do you deter it.

Your enemy will just try harder with more and better weapons and methods next time.

How DO you deter?

By exacting a deeply painful price.

3. It’s incorrect to say “nobody got hurt”.

There’s a 7 year-old Israeli-Arab girl called Amina Elhasuny fighting for her life.

That’s who coward Khamenei hit.

4. The Islamic Republic of Iran made a big mistake.

For the past 30 years it’s been wreaking havoc on the region—through its proxies.

A terror-octopus whose head is Tehran, and its tentacles are in Lebanon, Yemen, Iraq, Syria and Gaza.

How convenient.

The Mullahs send others to conduct horrendous terror attacks, and die for them.

Other people’s blood.

Israel’s strategic mistake for the past 30 years was to play along this strategy.

We always fought the Octopus’ arms, but hardly exacted a price from its Iranian head.

This should change now:

Hezbollah or Hamas shoots a rocket at Israel?

Tehran pays a price.

5. The enemy is the Iranian REGIME, not the wonderful Iranian people.

The Iranian regime reminds me of the Soviet regime in 1985: corrupt to the core, old, incompetent, despised by its own people, and destined to collapse.

The sooner the better.

The West can accelerate the regime’s inevitable collapse with a set of soft and clever actions, short of military force.

Remember, USSR collapsed without any need for a direct American attack.

Let’s do this.

6. Israel is fighting everybody’s war. In Gaza, Lebanon and Tehran.

We’re considered “the small satan” by radical Islam. America is the big one.

I’ll be clear: if these crazy fanatic Islamic terrorists get away with murder by hiding among civilians, this method will be adopted by terrorists worldwide.

We’re not asking anyone to fight for us. We’ll do the job.

But we do expect our allies to have our back, especially when it’s tough—and now it’s tough.

Be on the right side and help us defeat these horrible and savage regimes.

@Mike_Taylor1972@SusanGKomen@SimplifyAsstMgt@profplum99 Solid outperformance against the Healthcare sector benchmark, Mike!

Nearly 500 basis points above the benchmark so far, that means you added 36% higher ETF holder returns in the same sector. And all that for a good cause. Hats off!

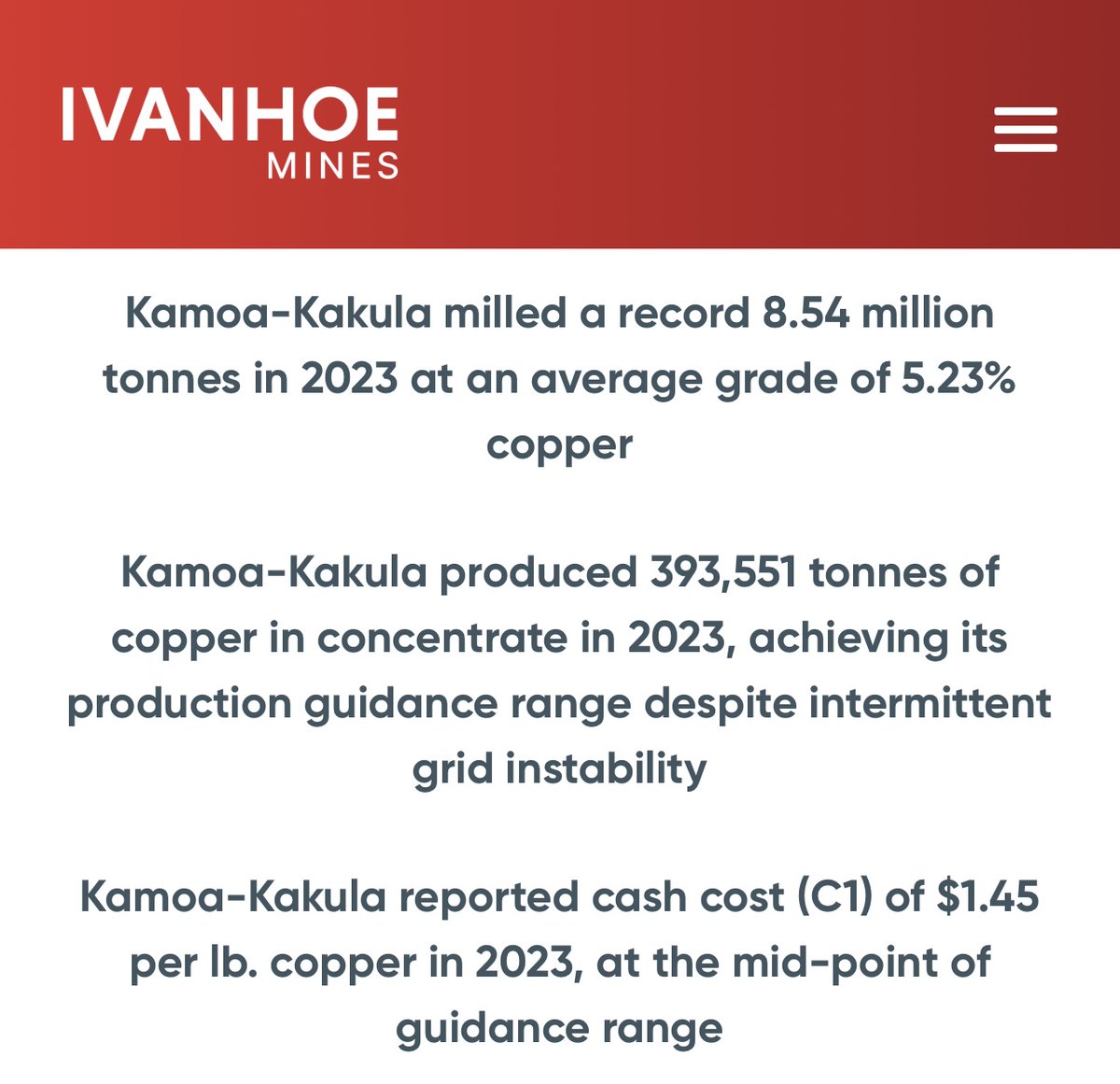

@robert_ivanhoe Each 1 GW of data center capacity requires 0.2% of global annual copper production. By 2030 the copper demand from data centers alone could rise to about 10% of global annual copper production.

Ivanhoe’s Kamoa-Kakula yearly output could supply 8 GW.

Does that roughly compute?

@joshyoung@FoundersPodcast@CorneliaLake @AlexVergeJOY Agree on Mr Verge.

You’ll love Ep 149: “In 1981, they realized eventually the market was so depressed, the best way to buy oil was not by drilling for more but by buying a company that was undervalued because you could buy the company for less than their oil was actually worth.”