Need help building some conviction in your AI names during this market downturn?

Read this post. Bookmark it. Come back to it.

Let Paradis guide you:

In my view, AI names are broadly down for a few reasons:

1. The market viewed $AVGO earnings + guidance as decelerating growth.

2. Hawkish turn from the Fed.

3. A cluster of AI bubble commentary at the end of June.

Please note what's not on that list:

1. Hyperscaler capex cuts.

2. Cancelled orders.

3. HBM oversupply.

4. Collapsing GPU rental pricing, etc etc.

Broadly speaking, absolutely nothing negative has happened on the demand side.

If you strip the whole AI trade down to first principles, it mainly boils into two layers that the market always confuses:

1. Financial stuff e.g. equity valuations, financing loops, neocloud debt stacks, where scepticism is warranted and where some pullbacks are healthy.

2. Physical stuff e.g. wafers, HBM, CoWoS capacity, optics, where demand > supply essentially everywhere.

Nothing's changed on the physical layer. So in my opinion, this sell off is just a reset before hyperscalers guide capex in their upcoming earnings.

But, for the case of this post - let me just stress test the bear case for the AI trade:

Basically everyone's desperate for compute rn.

Total hyperscaler capex guidance for 2026 is near $725B across $MSFT, $GOOGL, $AMZN, $META and $ORCL. Plus the OpenAI and Anthropic compute commitments layered on top.

I think that capex guidance has been revised up by every credible institution over a dozen times this year so far. From Goldmans, to MS, to BofA.

And I am sure that during earnings coming up soon, pretty much all of them will revise their capex forecasts up for 2026 remaining.

It was just a week or so ago, but remember how everyone felt about the $MU earnings? Pretty good, right? HBM sold out...LTAs...growing volumes of locked in demand/pricing.......I could go on and on.

But I feel like the bear case I see most often lately is to do with $NVDA's ecosystem commitments. E.g. their ~$124B spider web of investments + POs across areas like LLM labs and neoclouds.

I'll look at that a bit below, but they exist because fronteir demand is outpacing everyone's balance sheet + ability to fund it.

But first, you MUST realise that the structural driver has shifted in a way that "bubble" doom posters miss/ignore:

- The 2023/24 phase was a training-led capex cycle with lumpy and cancellable revenue.

- The 2025/26 phase is inference and agent led with reliable recurring and usage based revenue.

Inference demand compounds with deployment = so do financials.

This is the transition dark fibre never made in 2000 where telecom infra was built ahead of a demand curve that took something like a decade to actually arrive.

Compared to AI compute that is being built behind a demand curve aka shortages. Shortages are not bubbles!

In 1999-2000, telecom capex was funded by companies burning cash. In 2026, the marginal dollar of AI capex is funded by 5 of the largest cash generation machines ever. They're so well insulated from the capex they're spending that it won't matter in a few years time.

Now, I think we all know that AI names are super crowded.

I've noticed that since joining X where I get people commenting things like "What happened to $AAOI?" and "Do you like $SIVE?" when the names drop 10% in a day from volatility.

But on top of that, you look at data like BofA Fund Manager Survey that shows >80% of managers naming long-AI/semis.

That's a record high for any trade or thematic in the survey's history.

So crowding of this level mechanically deepens drawdowns because everyone's stop is behind everyone else's...it can become a vicious cycle on red days. And it explains why an >10% air pocket can arrive on no company or sector news at all.

Then you've got idiots posting online and going on podcasts saying that the AI trade is just like the internet trade back in 1997.

But as we all know, those internet names like Pets dot com had literally no cash flows and most had fugazi financials.

You just have look at the financials for companies like $SNDK which people also say is a bubble. They seem kinda fine to me? And will be fine going forwards. (Understating it slightly, their earnings will largely all be fantastic)

That being said....

Let me actually give you signals to look for that'll actually change my mind on whether I have conviction or just blind faith in the AI trade:

1. Capex cuts from hyperscalers rather than a deceleration in growth.

2. GPU rental spot pricing declining sustainably rather than plateauing.

3. HBM contract pricing rolling over while supply agreements get renegotiated.

4. Neocloud credit spreads gapping to distressed levels.

5. Fronteir labs like Anthropic/OpenAI seeing MRR's decline or stall.

These are probably the big five "tripwires" + none have been triggered so far. I don't see any being triggered for the forseeable future.

But all you need to know for a TLDR bull case for the AI theme is:

- demand for compute remains supply constrained.

- hyperscalers funding the capex are cash flow generative machines.

- valuations for high quality names from $SNDK to $MU to $AVGO to $NVDA are stupidly low.

On top of everything else mentioned here (I could keep going but I'll save you from reading more of my ramblings/rants).

That being said, in my view, there's certainly a case to rotate into higher quality names rather than random upstream shitcos.

I've mentioned this many times over the past couple of weeks.

From 2025 to early Q2 2026, you could basically long almost any name that had some sort of ties to AI and it'd go up 100% in weeks. $POET and $IREN come to mind.

I personally think being a little more selective going forwards will be more crucial, and financials will matter a lot more than going long a name that just falls in the AI bucket.

Sensing some market fatigue. Hopefully we get a brief period of healthy consolidation.

Sold a good chunk of $DRAM in this $66-$68 range. Could be a bit "early," but the memory run-up has been ridiculous and I wanted to add to the cash I built up from the space names. The narrative changing can also affect stock prices before the reality actually hits.

I've been increasing allocation into:

-CXL/NAND/HBF: $ALAB, $PENG and watching for a dip to add to Kioxia 285A. $SNDK if we get a big pullback.

-Photonics/CPO: $ALAB, added more $AAOI, plus smaller $XFAB and $SIVE; considering $SOI

-Power-semi/800V: added to $WOLF; have $NVTS, $IFX, $XFAB

-Testing: added to $AEHR; considering $COHU

-Token Factory: would add to $CRWV again in the $90s, bought back some $BRUN

I undersized some of these initially (lack of knowledge/confidence and a lot of capital was tied up in Space). Will look to add to any of these on a big pullback.

NFA, just my opinion.

Just some random notes about $AVGO earnings transcript

- Revenue target reiterated ($100B+ 2027, pretty sure markets wanted that to be raised this earning, hence the drop)

Remember $NVDA Jensen comments about $MRVL $1T company around networking/connectivity/interconnects?

- “So as the TPUs continue to accelerate, there’ll be pressure overall on margins.

But the connectivity side, the AI networking side of the business has very rich margins”

“Demand for … networking is simply insatiable”

Also very positive read through as well for the $LITE and the other players. But for TPU margins it goes down at scale, which is understandable.

- “they are placing orders in fairly huge demand, which basically gives us a lot more visibility.. runs all the way to 2028 right now”

positive read through on overall AI demand since it’s 2026 now… and orders are out in 2028

- The initial order for 1 gigawatt, which includes XPUs and our networking has been received and will start Delivery in the second half of 2027. for our other two customers, we expect shipments to begin late 2026 and accelerate into 2027.

$META custom AI program h2 2027 timelines

- “Our revenue, our content per gigawatt will increase. you start putting a lot, you start putting embedding CPU cores into the same XPUs and making those chips basically multi die with lots of hvm.”

Just for the GW modelers.

- “For OpenAI we have delivered silicon and we are on track for production late 2026”

OpenAI custom program timeline

- “If you ask about 27 or 28 that will continue to grow. We expect in fact 28 to be a substantial growth from what we are forecasting in 27.”

More about the demand ramp, go brrr

- “Google, that we expect a diversity of sources from them”

Mediatek (2454) primary beneficary, maybe $MRVL. Already expected though Google doesn’t sole source so they don’t get bottlenecked.

There’s quite a lot of AI demand visibility way until 2028, which is bullish on the AI sector as a whole. Regardless, Broadcom ends the week +0% lol.

TLDR: Strongly bullish AI demand, especially networking. Stocks don’t move in a straight line up, but demand curves 2026-> 2027 -> 2028.

@labubu_trader Agree to reduce leverages. Is it still risky to keep leaps since three vampires (Space X, anthropic, and Open Ai) are coming the second half of the year?

▶ Marvell CEO says copper wall is moving inside the rack, and copackaged optics is the only way through

• Marvell CEO Matt Murphy emphasized at Computex 2026 that the next bottleneck in AI infrastructure is not compute or memory but connectivity.

• The shift from copper to optical interconnect is already underway and is expected to trigger a large scale demand cycle within the semiconductor industry.

• He highlighted Marvell’s sophisticated engineering capability, integrating advanced CMOS DSP, fourth generation SiPh, and SiGe based broadband analog technology through its Coherent optical modules.

• Marvell’s first 102.4T switch dedicated to AI data centers, the Teralynx T100, is built on a 3nm process, draws under 1,000W, and delivers up to 25% lower power than competing solutions.

• The T100 routes signals through copper traces on the PCB to optical modules on the front panel, whereas a CPO switch connects optical fiber directly to the package and removes copper wiring entirely.

• The reach of copper cable is inversely proportional to bandwidth: at 100Gbps per lane it can carry signals about 5m, but at 200Gbps this shortens to roughly 2.5m, and at 400Gbps copper can no longer make connections even within the rack.

• Each time the “copper wall” moves one step, the number of connections that must shift to optical increases at least tenfold, which is expected to drive explosive demand across the optics industry, and the Taiwan supply chain is already expanding to respond.

• The number of connections inside a rack is roughly ten times the number of connections between racks, so conventional pluggable optical modules alone cannot address the power and space limits; CPO solves the connectivity problem by integrating the optical engine directly into the switch and compute package.

• Nvidia’s Vera Rubin platform has already adopted Spectrum-X Ethernet Photonics, the first CPO based switch to enter mass production, a case showing that the CPO transition has moved beyond proof of concept into actual commercialization.

• As optical connectivity extends into the server itself, compute, memory, and network resources can be disaggregated and dynamically configured per workload, enabling a shift from a fixed server architecture toward operating the entire data center as a single integrated system.

• He stressed that the CPO transition is impossible without Taiwan’s manufacturing ecosystem, explaining that Marvell has accumulated high volume PAM4 production experience, field data, and supply chain infrastructure including ASE.

• Over the past decade Marvell has invested a total of $36 billion to acquire companies such as Inphi, Cavium, and Celestial AI, expanding its connectivity portfolio.

• He emphasized that Marvell is the only company able to address the full connectivity stack of an AI data center, from millimeter scale inside the package to kilometer scale between data centers.

$MRVL

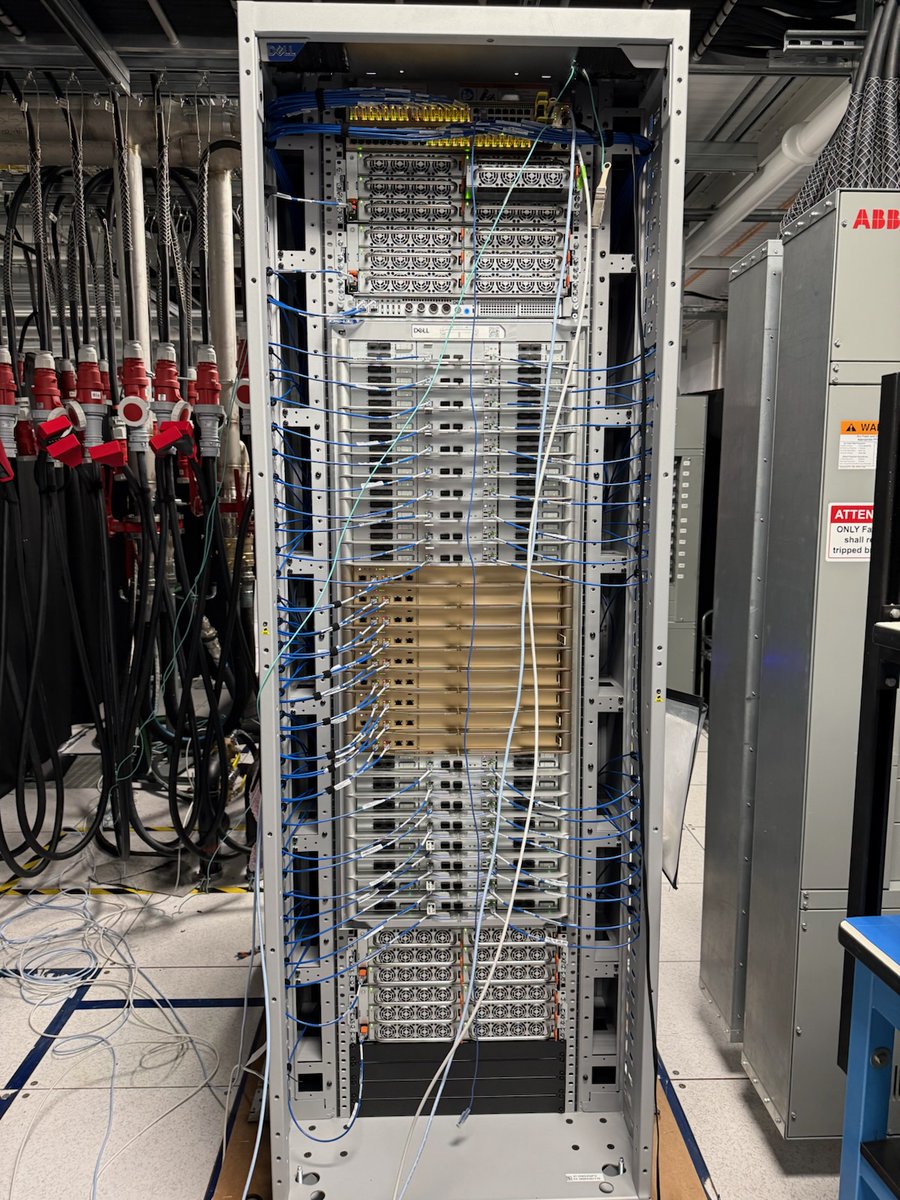

The world’s first @nvidia Vera Rubin NVL72 server rack is here.

We’re thrilled to deliver the first working, liquid-cooled @Dell PowerEdge XE9812 for @CoreWeave.

Built for the next era of AI infrastructure. 🚀🤝

An important warning - a small group of activists shut down clean nuclear power - and now they are trying to do the same data centers. It would plunge the country into a recession, high unemployment & risk our national security to China. 🇺🇸