Very excited to share this. One of the big challenges in studying geoeconomics is measuring how firms respond to pressure. The new GCAP Geoeconomic Monitor uses earnings calls + LLMs to track firm exposure and responses to tariffs, sanctions, and export controls in real time.

Introducing the GCAP Geoeconomic Monitor, tracking how firms around the world are responding to tariffs, sanctions, and export controls in real time.

👉Explore the Monitor https://t.co/gGsiQXaMUF

👉User Guide https://t.co/vCw2I1RuTQ

1/4

Political economy of geoeconomics. In a comment on Clayton Maggiori Schreger, “Putting Economics Back Into Geoeconomics,” I argue we cannot understand geoeconomics without political economy. Now in the NBER Macroeconomics Annual 2026, available here. https://t.co/dFzZasZwIW

Very excited to share this. One of the big challenges in studying geoeconomics is measuring how firms respond to pressure. The new GCAP Geoeconomic Monitor uses earnings calls + LLMs to track firm exposure and responses to tariffs, sanctions, and export controls in real time.

Introducing the GCAP Geoeconomic Monitor, tracking how firms around the world are responding to tariffs, sanctions, and export controls in real time.

👉Explore the Monitor https://t.co/gGsiQXaMUF

👉User Guide https://t.co/vCw2I1RuTQ

1/4

So indescribably happy to see this in print in the May edition of the AER (and in good company)! Sincere thanks to everyone who helped along the way 👇🏼💡🎊🤩

Using fund-level microdata to show US holdings of Chinese Renminbi (RMB) bonds fell sharply after 2021, with a large decline in the share of US funds holding any Chinese RMB debt, from @brunocavani_, @chris_d_clayton, @_amandads_ , @m_maggiori, and @jschreger https://t.co/B1smjKcG1E

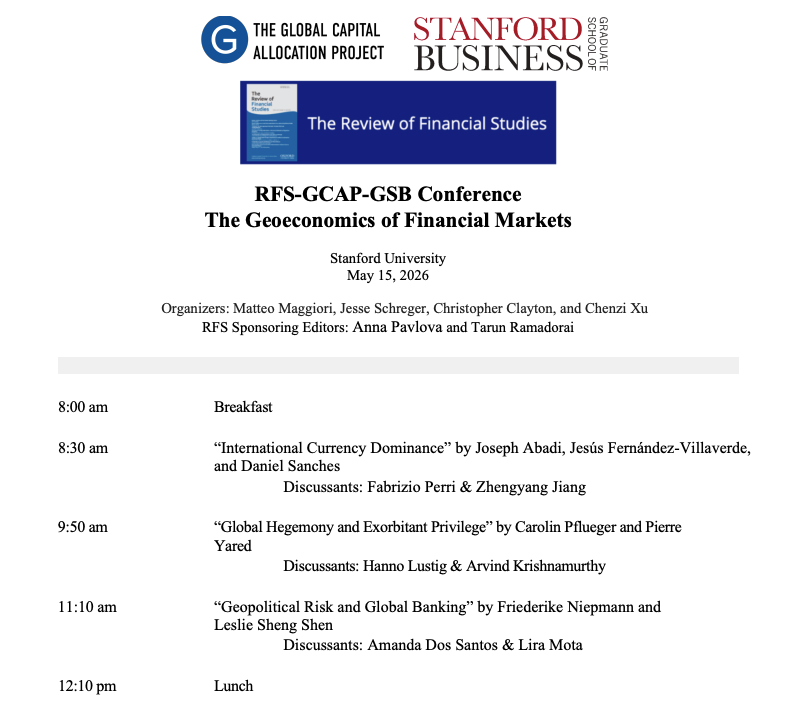

The agenda for the RFS-GCAP-GSB Conference on The Geoeconomics of Financial Markets on May 15 is now available.

View it here: https://t.co/ZieiaUTxt6

Organized by @m_maggiori, @JSchreger, @chris_d_clayton, @chenzix

Hosted by the RFS,@GCAProject, and @StanfordGSB

New working paper+data! With @kat_bergant, K. Teoh and @MartinUribeEcon, we study a new dataset on cross-border flow restrictions from the 1950s, from official text using LLMs. https://t.co/VlVPEyKlsh. Github: https://t.co/USmjR3egMz. Please RT if interested. Brief thread on it.

Here is our recorded AEA session https://t.co/AEtGmsO0w9 at #ASSA2026 on tariffs and the dollar w/ @itskhoki , @JSchreger , @krogoff , @MartinUribeEcon. Interesting conversations w/presenters, discussants and the audience on understanding tariffs' impact on the economy: what happened, can tariffs be good, models and reality, how countries compete, why the dollar went the wrong way and what the future may hold for the dollar and the U.S.

🎓 Call for Applications | JIE Summer School 2026

📍 Milan (Bocconi University) | 🗓 July 6–8, 2026

Lectures by Cécile Gaubert, Christoph Trebesch, David Hémous, Federica Romei, Christopher Clayton & Natalia Ramondo.

🗓 Deadline: Jan 25, 2026

👉 https://t.co/rXcgF6O1DX

🥳🎖️🥂🎈Hooray for my young coauthor @GBonfantiEcon (of @Columbia Econ, advised by @Columbia_Biz faculty), winner of

@EEANews@UniCreditEurope Best Job Market Paper

In his highly interesting JMP he uses impressively large bond holdings data to solve a puzzle of significant and immediate policy relevance - namely: "why is EU supranational debt not working as a Euro safe asset?"

We are hiring in the Economics Division @Columbia_Biz 🔥!

We are looking for two juniors, in any field. Apply here to join our community:

https://t.co/K3sShn3quG

Please send us your application (and letters..) ASAP, we are looking forward to start reading your work soon!

We are excited to release a public, research-ready dataset with complete holdings at the security level for U.S. mutual funds and ETFs each quarter, built from SEC Form N-PORT mutual fund filings.

👉 Access the data and code at the GCAP Data Hub: https://t.co/YzOyhwoPmE

1/3

Super interesting!

"Decoupling Dollar and Treasury Privilege" by Wenxin Du, Ritt Keerati, and Jesse Schreger.

"We document a strong decoupling between the convenience yield on the US Dollar and US Treasuries. We measure the convenience of the U.S. dollar using covered interest parity (CIP) deviations between risk-free bank rates, such as secured overnight rates since the benchmark reform. In parallel, we measure the convenience of U.S. Treasury bonds through CIP deviations between government bond yields. We find a pronounced divergence between the two convenience measures in recent years: while the U.S. dollar exhibits strong convenience post-Global Financial Crisis, the U.S. Treasury convenience has not only declined substantially but has turned negative, most strongly so at medium- to long-term maturities. We argue that the relative supply of government bonds between the US and other developed markets is a key driver of the U.S. Treasury convenience compared to other government bonds."

https://t.co/YILsF4CwMD