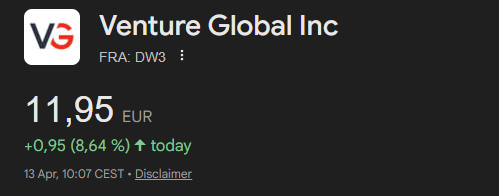

$VG earnings look very good.

🟢 EPS .19 (.13 expected).

🟢 Revenue $4.6b (3.97b expected), up 53% Y/Y.

🟢 EBITDA Guidance increased massively to $8.2-8.5b (was $5.2 to $5.8b).

🟢 Two more 5 year agreements for ~2.5 MMBtu

Some analyst updates after yesterdays Q1 release for

$VG :

🟢Citi raised the PT to $17 (from $12)

🟢UBS confirmed the PT of $21

🟢MS confirmed the PT of $22

🟢DB, RBC, CapOne confirmed the PT of $16

🟡Wells Fargo confirmed PT of $14

I think overall results came in better than expected, beating EPS street consensus by +53% and Net Income +44%.

Q2 will be far more important, given the financial performance from the spread increase will be first really shown here.

The pullback during the last 2 weeks was healthy, I believe the case is still very much intact. The guidance raise was needed but remains conservative.

Despite heavy profit taking this week, $VG is still up 87% YTD.

Trades at 11.3x trailing EV/EBITDA.

Broader industry average is 12.2x.

Highest cargo flexibility of any US LNG exporter.

Down 25% from the peak.

That is not a reason to sell. It is a reason to look again.

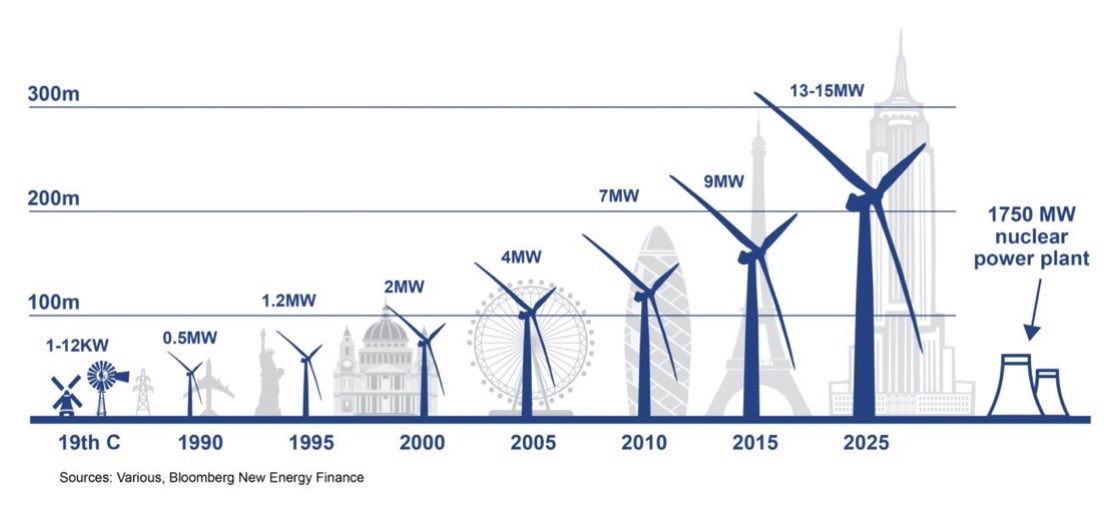

⚡ The Most Efficient Clean Energy Source Isn’t What You Think

Nuclear.

• A 1,000 MW nuclear plant needs 1 square mile

• Wind needs 360× more land

• Solar needs 75× more land

To match one nuclear reactor:

• ☀️ 3+ million solar panels

• 🌬 430+ wind turbines

Energy transition isn’t just about clean.

It’s about scale and density.

Most renewables are land-intensive and intermittent

Nuclear is compact, constant, and scalable

The profit taking is healthy. The thesis is not broken.

BP arbitration is still outstanding. Hormuz could open. Cyclones pass.

But 30% of global LNG supply does not come back overnight. Physical damage takes time to fix.

$VG at $16 with $11B of EBITDA is not a sell. It is a gift.

Not financial advice. Do your own research.

Markets are still pricing a base to downside scenario for Venture Global:

I think the business plan changed dramatically within the last 5 weeks. And analysts as well as journalists are only adjusting cautiously to the new reality in energy markets.

Here is how:

@WSJ Markets are still pricing a base to downside scenario for this company. I think the business plan changed dramatically within the last 5 weeks.

Link in my bio.

Deutschland sitzt auf einem gigantischen Energieschatz und tut so, als wäre es völlig abhängig vom Ausland und auf Wind und Sonne angewiesen.

Unsere Steinkohle reicht für Tausende Jahre, die Braunkohle für 300 bis 400 Jahre. Erdgas könnte uns 20 bis 30 Jahre versorgen und selbst die Ölreserven würden noch rund 10 Jahre durchhalten.

Und dann das große Tabu: Mit den vorhandenen Uranbeständen ließen sich die abgeschalteten Kernkraftwerke locker 100 Jahre lang betreiben – sicher, zuverlässig völlig unabhängig vom Ausland, umwelt- und klimaschonend.

Während andere Länder ihre Ressourcen nutzen, wird hier absichtlich verknappt, verteuert und verzichtet. Nicht aus Not, sondern aus reiner Ideologie.

Deutschland hat kein Energieproblem – Deutschland hat ein massives politisches Problem.

Markets will tank once it becomes clear that the United States cannot do anything to end this. Iran currently holds the leverage, and that leverage increases with each passing day. They could make demands that are completely unacceptable to the U.S. On the other hand, the U.S. cannot simply withdraw, because doing so would allow Iran, China, and Russia to dictate a new world order: either you align with us against America, or you face losing access to energy, fertilizers, and helium.

Markets aren’t slow in pricing in this desaster because they are stupid. They’re slow because the scale is hard to grasp. People think in comparisons. If there’s no precedent, they discount it. That bias has worked, until it doesn’t. Was the same with covid.