【布林肯:过去47年中,伊朗只妥协过2次,而此刻特朗普把自己逼近了“死胡同”】

这段CNN对布林肯的专访谈了5个重要的问题:

【1】 伊朗极少做出根本性妥协,美国现政府陷入了困境

在过去47年的历史中,伊朗只做出过两次根本性的妥协(结束两伊战争以及与奥巴马政府达成核协议);目前特朗普政府采取了某种“缓兵之计”,但已经将自己逼入了一个难以脱身的角落

【2】 美国若要重启战争,将面临两个核心掣肘

经济市场制约:包括对石油、天然气、化肥价格以及债券和股票市场的敏感性。

弹药库存不足:进攻性和防御性弹药的严重消耗,甚至削弱了美国在其他地区的威慑力(包括亚太)。

【3】 美国取得了战术上的成功,但面临战略上的失败

表现:行动结束后,伊朗政权依然稳固,且依然保留着高浓缩铀、可以重新启动的离心机,以及重建导弹生产能力的基础。

【4】霍尔木兹海峡的底线被打破,伊朗获得了巨大的谈判筹码

过去,美伊双方都在霍尔木兹海峡问题上保持克制,以避免引发关乎存亡的危机。但现在这种默契已经被打破,导致伊朗在僵局中获得了巨大的筹码。

面对这种情况,美国总统必须做出抉择:要么重返高风险且代价高昂的战争;要么进行谈判,而谈判势必需要给伊朗一些好处,比如允许其在霍尔木兹海峡收取通行费或解除制裁。

【5】 铀浓缩问题上存在“保全面子”的妥协空间

特朗普政府主张伊朗“零浓缩铀”,而伊朗则坚称作为《不扩散核武器条约》(JCPOA)缔约国拥有浓缩铀的权利。

根据过去伊核协议(JCPOA)的经验,双方完全可以达成一种务实的妥协:美国在名义上不承认伊朗的浓缩权利,但实际上允许伊朗保留极低水平、极小库存的铀浓缩能力。这样既能给伊朗保全面子,又能确保伊朗若想突破协议制造核武器,至少需要一年以上的时间。

FULL INTERVIEW: Former Secretary Of State Antony Blinken Weighs In On U.... https://t.co/9BQbteHY6a via @YouTube

With collapse US-Iran talks & new US naval blockade on Hormuz (stopping the little oil passing), where is this all heading?

Obvious next US move: ground ops to seize enriched uranium soon. 10k troops on ground for weeks, minimum

Stage 3 of Escalation Trap on horizon

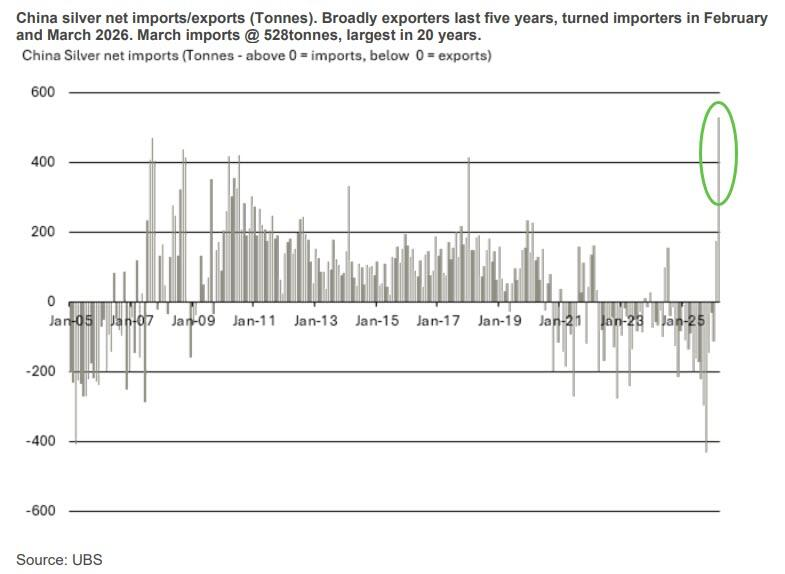

China is banning sulfuric acid exports starting May 1, 2026.

The last time China did something similar, it was silver and it moved from $30 to $83 in 3 months.

In October 2025, China announced export restrictions on silver. The ban had not even started, but the market reacted immediately.

Now compare that to sulfuric acid.

This is not a tradable metal or a niche commodity. This is one of the most critical industrial inputs in the world.

It sits at the center of:

• Fertilizers that support global food production

• Copper extraction used in electrification

• EV battery manufacturing

• Semiconductor processing

• Oil refining

• Pharmaceuticals

If sulfuric acid supply tightens, it does not hit one sector. It hits multiple supply chains at the same time.

The sulphur was already under stress before this ban.

The Middle East produces 44% of global sulfur, which is the key input for sulfuric acid.

When the Iran war escalated and flows through Hormuz were disrupted, sulfur shipments dropped.

Prices reacted immediately.

Sulfur prices went from around $101 per ton in mid-2024 to over $600 per ton today. Sulfuric acid prices are already up more than 200% since the war started, and over 500% in the last two years.

This is not a new shock. The market was already tight.

Some copper producers are now operating with just 30-60 days of sulfur inventory.

There are already warnings from industry leaders that production cuts may begin if disruption continues.

China just removed the last stable supply source.

China is the largest exporter of sulfuric acid globally.

In 2024 alone, it exported around $349 million, more than any other country. A large portion of this comes as a byproduct of copper and zinc smelting.

Now, starting May 1 exports are being restricted. This is important because:

- The Middle East supply is already disrupted.

- Now China is stepping out at the same time.

Two major supply sources are being hit simultaneously. This directly impacts core global production.

Sulfuric acid is not optional in many processes. Around:

• 20% of global copper production depends on it.

• 45% of DRC copper output relies on acid based leaching.

• 50% of global uranium production uses it.

• 30% of global nickel production depends on it.

Chile, the largest copper producer in the world, imports over 1 million tonnes of Chinese sulfuric acid every year.

Estimates suggest around 20% of its copper output is now exposed to disruption. This is not a small part of the supply chain. It is a core dependency.

THE BIGGEST RISK IS FOOD.

Around 60-70% of sulfuric acid production goes into fertilizers.

And China has already restricted phosphate fertilizer exports through 2026. Now it is restricting the acid needed to produce those fertilizers.

That compounds the problem.

- Phosphate exports are expected to drop from 5.4 million tonnes to 1 million tonnes.

- Urea prices at U.S. ports are already up more than 25% since late February.

This is starting to move into food supply, not just industrial metals.

There is no short term solution. Sulfuric acid capacity cannot be replaced quickly.

New systems take 2-3 years to build.

Transport is complex and limited. It requires specialized tankers and infrastructure. Alternative suppliers do not exist at the scale needed.

So the situation is clear:

- Middle East supply disrupted

- China supply restricted

- Demand unchanged across multiple industries

The last time China restricted exports of a key commodity, the market moved 150% before the ban even took effect.

This time, the commodity being restricted is far more deeply embedded in the global system.

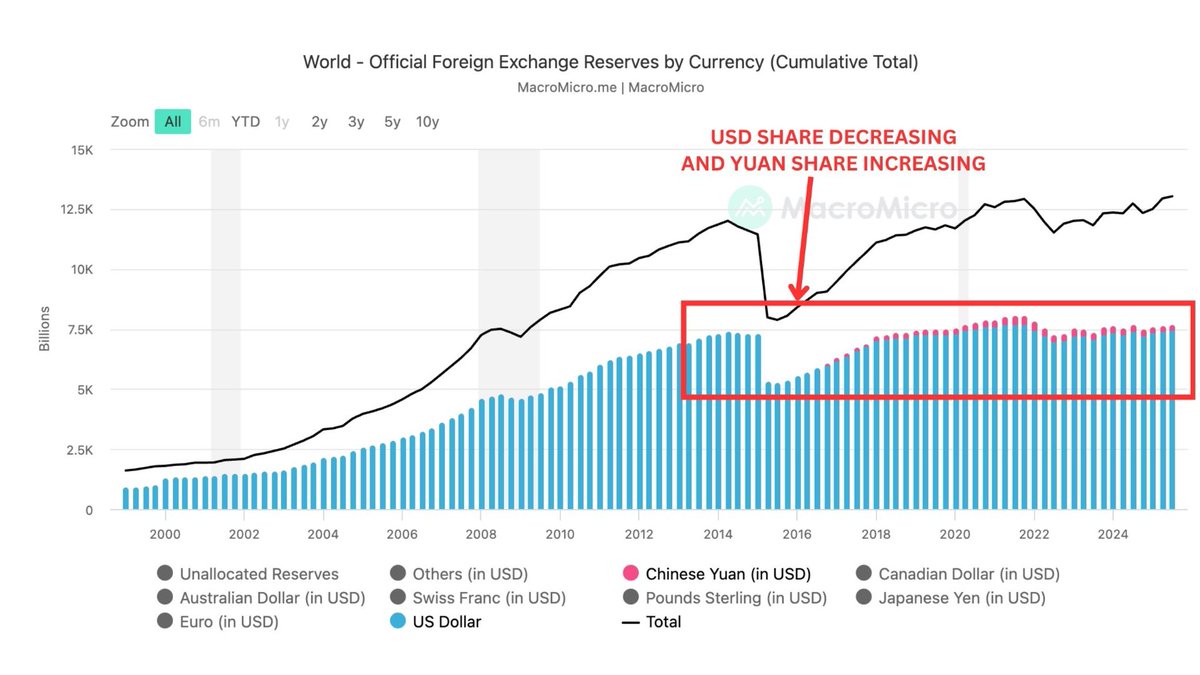

BREAKING: The world's largest banks, sovereign governments, and multilateral institutions are quietly abandoning dollar debt and borrowing in Chinese yuan instead.

The numbers are too large to ignore.

In March 2026, foreign issuance of Panda bonds tripled year on year to 27.8 billion yuan ($4 billion) in a single month.

Total yuan denominated financing by foreign borrowers hit a record 218 billion yuan ($31.6 billion) in just the first weeks of 2026. The entire full year of 2025 saw only $167 billion raised through yuan notes and loans combined.

Look at who is actually doing this.

- Deutsche Bank issued the largest single panda bond by a foreign bank in history, 5.5 billion yuan, oversubscribed 1.55x on the 3-year and 1.63x on the 5-year

- The Asian Infrastructure Investment Bank issued 3 billion yuan the same month, with 58% of allocation taken by overseas investors

- Indonesia sold 9.25 billion yuan at roughly one full percentage point below what it paid on its euro denominated debt issued the same week

- Morgan Stanley and Barclays both became repeat yuan bond issuers in 2026

- Hungary issued sovereign panda bonds

- The Asian Development Bank raised a record 8.3 billion yuan in March 2025

The reason comes down to one number.

China's 10-year government bond yield is 1.82%. The equivalent U.S. Treasury yields 4.46%. That is a spread of 260 basis points, the widest gap since August 2025.

Borrowing in yuan is approximately 60% cheaper than borrowing in dollars right now. For governments and institutions that trade heavily with China, that calculation is straightforward.

Now look at what is happening to the dollar at the same time.

- The DXY fell 9.6% in full year 2025, the worst annual performance since 2017

- In the first half of 2025 alone it fell 10.7%, the worst first half performance in over 50 years

- The U.S. dollar's share of global foreign exchange reserves fell to 56.32%, the lowest level since 1995, down from a peak of 72% in 2001

- China's U.S. Treasury holdings fell to $682.6 billion in November 2025, down from a peak of $1.32 trillion in 2013, a 48% decline over 13 years

- China has been selling U.S. Treasuries for nine consecutive months as of late 2025

Something more structural is also breaking down inside the Treasury market itself.

Research from the National Bureau of Economic Research found that U.S. Treasuries' convenience yield, the premium investors historically paid just to hold the safest asset in the world, has turned negative, currently sitting at -0.25% for 10-year maturities.

This premium used to save the U.S. government hundreds of billions in borrowing costs annually.

State Street confirmed that since early April 2025, rising Treasury yields now signal fiscal risk, not economic strength. That is the opposite of how a safe haven behaves.

During the global bond sell off in March 2026, triggered by geopolitical tensions and surging energy prices, U.S. Treasury yields spiked to 4.4055%, a nearly eight month high. UK, Australian, and New Zealand government bonds all hit multi-year yield highs.

China's 10-year yield moved from 1.80% to 1.84%. Chinese bonds were almost stable while everything else sold off.

Now look at what just happened today.

A ceasefire between the US and Iran has been announced. The Strait of Hormuz is reopening. But Iran is charging every oil tanker that passes through $1 per barrel of cargo, with payments accepted in Bitcoin or Chinese yuan.

A Very Large Crude Carrier carrying 2 million barrels pays up to $2 million per transit. Iran's National Security Committee has already passed legislation codifying this fee structure into law.

The system is specifically designed to bypass the dollar based financial system and U.S. sanctions. At least two vessels had already paid in yuan before the ceasefire was even announced.

The world's most critical energy chokepoint is now priced in yuan and Bitcoin, Not dollars.

The trade picture makes the shift more structural than it looks.

The yuan now accounts for 34.5% of China's cross-border goods trade settlements, up from just 10% in 2017.

China is the dominant trading partner for more than 120 countries. When your largest trading partner settles trade in its own currency, you eventually need to hold that currency as a working reserve and you buy yuan denominated bonds to do it.

The offshore dim sum bond market hit a record 870 billion yuan ($123 billion) in full year 2025, its eighth consecutive year of growth. Around 30% of global central banks are expected to increase their RMB holdings over the next decade.

UBS Asset Management said the yuan's share of global central bank reserves could rise to 10% over the medium term. It currently sits at 1.93%.

For decades, there was no real alternative to the dollar. That is what made it dominant.

What is changing now is not that the dollar is broken. It is that the world has stopped assuming it is the only option. Once that assumption breaks, it does not come back.

The Iran ceasefire is being called a “pause.”

It’s not.

It’s a revelation:

The U.S. used overwhelming force—and still could not control the outcome.

That’s a structural shift in power.

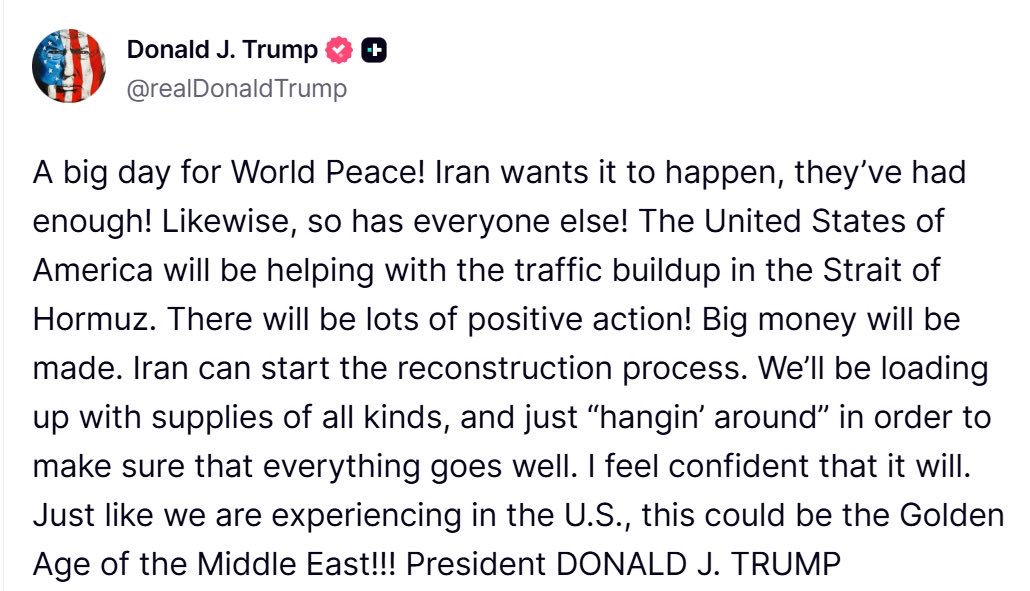

BREAKING: The United States Navy is about to provide security escort for commercial vessels passing through a toll booth that charges in Chinese yuan.

Read Trump’s post again. “The United States of America will be helping with the traffic buildup in the Strait of Hormuz.” Now read AP’s confirmation of the ceasefire terms. Iran and Oman will charge fees on ships transiting the strait. Iran’s parliament pre-approved the Hormuz Management Plan on March 31st with rial-based tolls and coordination with Oman. Bloomberg and Lloyd’s List confirmed that at least two vessels have already paid in yuan through IRGC-linked intermediaries using secret safe-passage codes.

The ceasefire that Trump announced does not prohibit the toll. It does not mention the toll. The post that promises American logistical support for the traffic buildup does not reject the toll. The carrier strike groups that will be “hangin’ around” to make sure everything goes well will be providing the security umbrella under which Iranian military personnel collect yuan from every tanker that passes.

The United States fought a 39-day war that destroyed 85 percent of Iran’s weapons-chemistry capacity, dismantled 130 air defence systems, severed the transport network, struck Kharg Island, and killed the IRGC intelligence chief. The campaign cost billions in munitions, fuel, and deployed assets. And the ceasefire that concluded Phase 1 created a toll booth at the chokepoint the war was fought to reopen, denominated in the currency of the nation that applied last-minute pressure to make the ceasefire happen, collected by the military force the campaign was designed to degrade, and protected by the navy that prosecuted the war.

The Gulf states see it. Saudi Arabia, the UAE, and Bahrain are alarmed. AP reported their concerns about Iranian gatekeeping, economic leakage, and the precedent of charging fees on what was previously a free international waterway under UNCLOS transit passage rules. Oman is co-charging, which fractures the GCC response. Kuwait and Qatar are quiet, prioritising energy security over confrontation. The Gulf is paying the toll. America is providing the escort. China is collecting the currency benefit. And Iran is funding its reconstruction with the revenue.

Deutsche Bank called the war the inception period of the petroyuan. That phrase was published before the toll booth was formalised. Now the toll booth exists, it is legislated, it is operational under the ceasefire, and the world’s most powerful navy is positioned to ensure the traffic flows smoothly through it.

Trump’s strategic logic is sound at the bilateral level. The campaign achieved its military objectives. Hormuz is reopening. Iran is at the table. The tools remain available. Islamabad begins Friday. But at the systemic level, the architecture the ceasefire created is a yuan settlement layer embedded inside an American security guarantee. The molecules that flow through the strait will be priced, insured, and tolled in a framework that did not exist six weeks ago, and the precedent does not expire when the ceasefire does. Iran’s parliament legislated the toll. The legislation does not have a sunset clause.

The Golden Age of the Middle East may arrive. The petrochemical reconstruction will take years regardless. The centrifuges are still spinning. The ghost fleet is still sailing. And the toll booth that the US Navy is about to protect charges in yuan.

Full analysis on Substack.

https://t.co/0fIdGsM5qH