When do private companies need to approve SPVs?

As a major sponsor of venture SPVs, I thought I’d share some thoughts on this, particularly in light of all the chatter on this topic surrounding Anduril and Anthropic lately.

First, some reasons why I have good information on this topic:

1. In just over 2 years, starting in April 2024, we built an SPV business with over $2.1 billion in AUM (at FMV). We have learned a LOT along the way.

2. We manage both single-layer and dual-layer SPVs. Most of our SPVs, by value and number, are single-layer, but a substantial portion are dual-layer.

3. Our single-layer funds are DIRECT shareholders on-cap table of over 40 late-stage unicorns, including the likes of @AnthropicAI, @perplexity_ai, @cursor_ai, @Kalshi, @Polymarket, @LiquidDeath, @cerebras, @Apptronik, and dozens of other household names.

Now, do private companies need to approve SPVs? It depends on what you mean by that. Here are four different cases.

1. An SPV purchases a company’s stock. If the company has an approval right over transfers (they usually do), then YES, this purchase must be approved.

2. An SPV syndicates to investors instead of using pre-committed capital, in order to complete a direct primary investment. YES, an issuer has the ability, in the purchase agreement or subscription agreement, to require the investor to use pre-committed capital instead of syndicating to fund the investment.

3. An LP of a single-layer SPV sells to a new LP (the recent Anduril case). NO, this transaction almost never requires company approval, and neither the GP (@packyM) of the single-layer SPV nor the selling or buying LP (@ankurnagpal) typically seeks company approval (@mttgrmm). Company approval typically has no bearing on the validity of the investment.

4. A second-layer SPV invests into the primary issuance of a first-layer SPV. Unless the underlying primary investment documents prohibit syndication (we have rarely seen this), NO, this transaction does not require company approval.

One big misconception seems to be that the company can or should approve transfers between investors in an SPV that holds direct stock, or that the GP or LP should get the company’s blessing for such transactions (case 3 above).

This idea runs contrary to decades of private market practice. Hundreds of billions in LP stakes in private equity funds change hands every year. The underlying companies almost never approve such transfers, and in the rare cases they do, it’s usually because the GP is going to them out of deference, not because they are required to do so. It's only the explosion of SPVs in the venture space that has brought sudden attention to this question.

Happy to debate this topic if anyone has a different take.

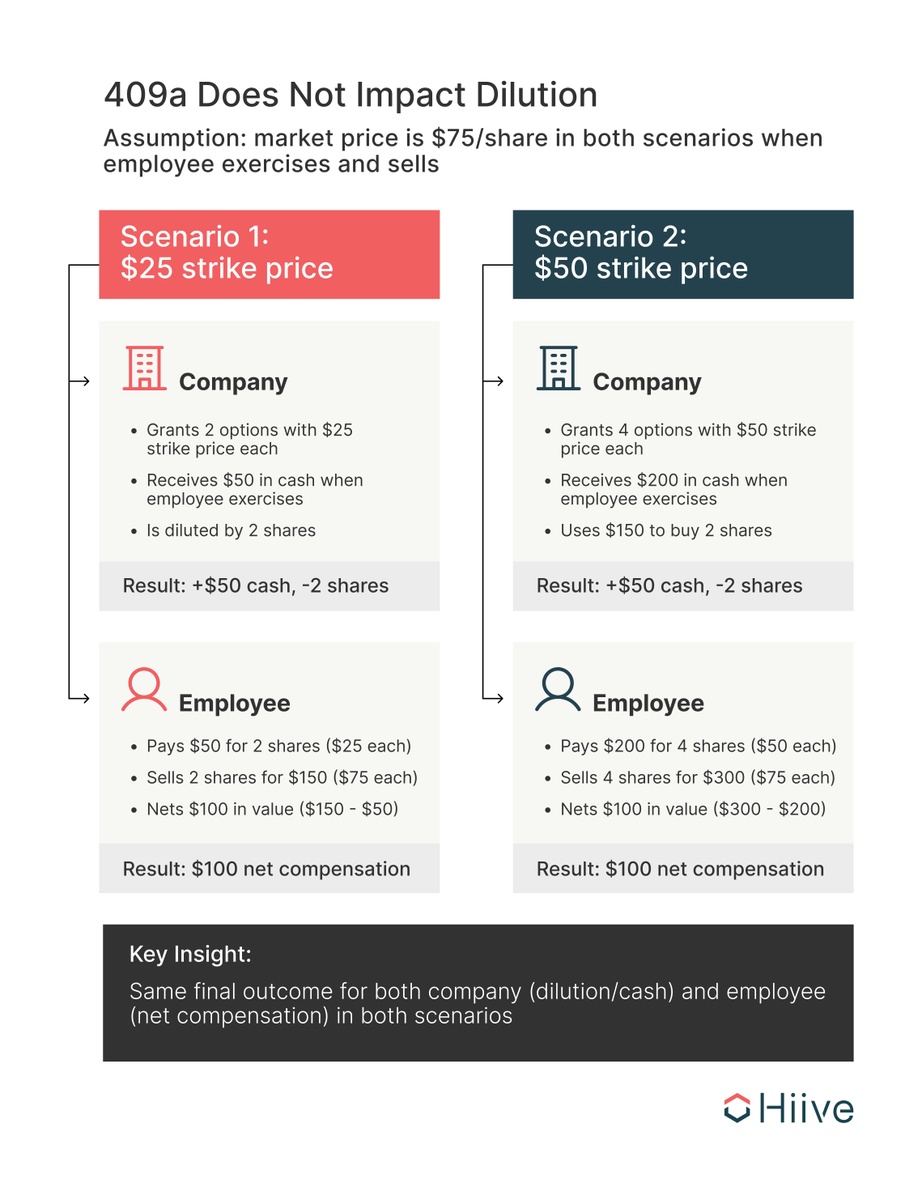

Company execs often justify prohibitions on secondaries based on concerns about the impact on their 409A valuation.

Because the strike price of option grants to employees is priced at the 409A valuation, some executives are obsessed with keeping it low. They believe that they can confer more value on employees, with less dilution, by keeping the 409A artificially depressed.

These fears are not well-founded for the following reasons:

1) Secondaries rarely impact the 409A valuation between annual re-assessments.

2) Even after 12 months, or in the rare cases where secondaries do impact 409A, the company should not fear greater dilution with a higher strike price because it is able to use the cash from option exercises to buy back stock at current market value (CHART BELOW ILLUSTRATES THIS POINT).

3) The fact that some of the largest private companies in the world (@cerebras, @krakenfx, @LightmatterCo, @Ripple, among many others) allow their stock to trade relatively freely gives evidence that these sophisticated firms are not concerned about this issue.

The bottom line: there is plenty of evidence that 409A valuations are NOT a reason to stop secondary trading.

Link to the full @Hiive_HQ BLOG POST on this topic in the comments below.

Let me know if you can poke holes in our argument!

#liquidity

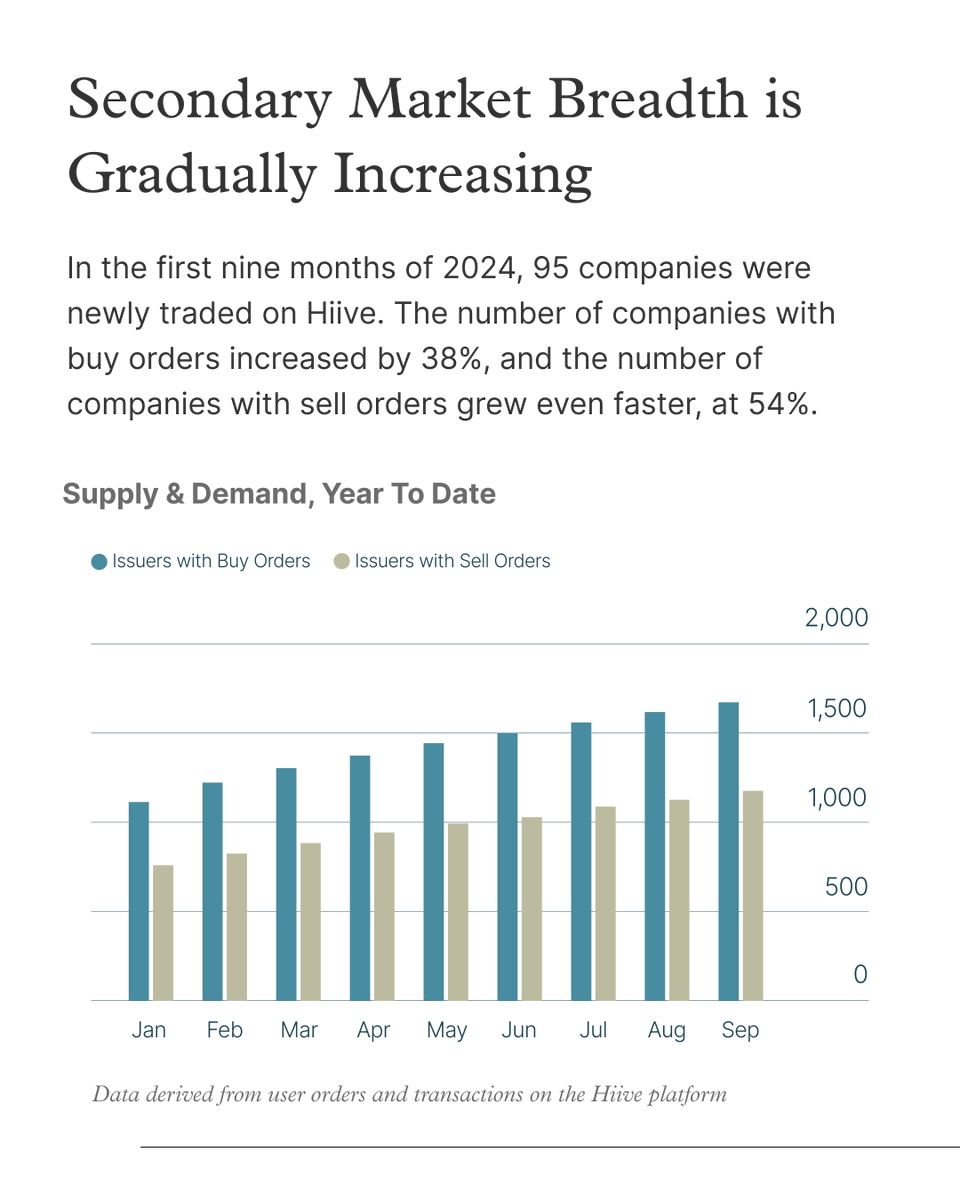

Employees and early-stage funds seem to decreasingly be waiting for natural exits, as these traditional liquidity events have become less frequent.

We’re seeing this trend reflected directly in Hiive marketplace data.

Read the full report on our website. See disclosures in the first comment.

#liquidity #preipo

We're excited to announce that Sarah Huggins, our Co-Founder, COO, and GC, has been recognized by Parity in this year's Top 100 Women in FinTech report. This honor highlights Sarah's leadership and dedication to driving innovation in the industry. Congratulations, Sarah!

The mechanisms of the private market have long been considered a black box. The founders of Hiive recognized that technology could unlock its potential and bring transparency to issuers, investors, and sellers. Find out how they did it.

This marks an important milestone in Hiive's mission to unlock the value of the private market. We are now closing over $100 million in transaction volume per month. Congratulations and thank you to everyone who helped make this possible.

The Hiive50 index is a broad indicator of the direction and momentum in the pre-IPO market, bringing even greater transparency to startup investing. Welcome to a new era of liquidity. https://t.co/r6xdBRZjfN #Hiive50#PreIPO#VC

A trading platform allows certain investors to buy and sell shares of pre-IPO unicorns. @SimDesai, CEO and Founder of @Hiive_HQ joins @KellyCNBC to discuss trends in the space.

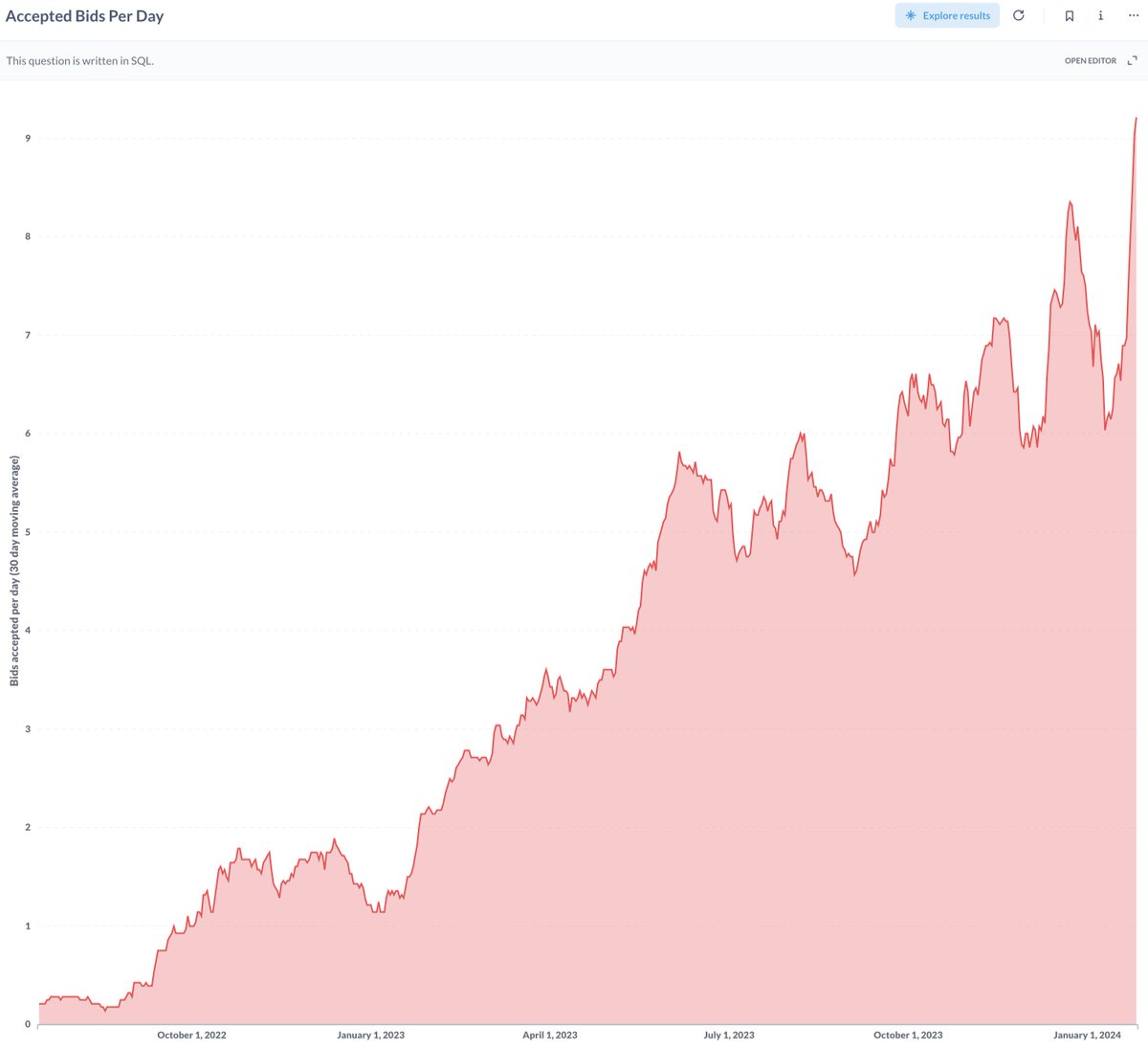

New charts launched: You can now dive deeper into our 2,500 open orders in the private markets to see things like different transaction types, share types and a smattering of all our market activity.

Check them out and see what insights you can find!

How's this for transparency into the private market?

This is the 28-day moving average of the number of bids accepted per day (including weekends) by sellers on the @Hiive_HQ platform since launch in July of 2022.

We actually submit about 60-65% of these matches to the company for approval. The remaining 35-40% are either cancelled by us or the parties before being submitted to the company for a range of reasons, OR are indirect deals that don't involve an actual share transfer and therefore don't need to be submitted. Overall about half of all accepted bids result in closed transactions on the agreed terms.

Any questions?

#privatemarkets #stockoptions #secondarymarket #venturecapital #unicorns #marketplaces #liquidity #privatemarket @SpaceX@Reddit@databricks@OpenAI@stripe@flexport@rubrikInc@Chime

It’s been 10 years since the original unicorn analysis (when we accidentally coined the term)🦄

So, our @CowboyVC team dug into new data. The tech industry has changed a TON!

✨ From 39 to 532 unicorns

✨ Pendulum swung HARD from consumer to enterprise

✨ Business types, founder backgrounds & geos changed a lot

BUT

🥺 Unicorns became way less capital-efficient

🥺 93% are ‘papercorns’ & 60% are ‘ZIRPicorns”

despite many fragile unicorns right now, we see many healthy ones too

And with AI, we expect 1,400+ capital-efficient unicorns by 2033, which will make tech even bigger and more important🌟

It’s a long read (sorry!) but pls check it out - would love feedback. What resonated, what did we miss? 🙏 🙏 🙏

Full post 👉 https://t.co/5DD8TPhbHq

Thinking of joining a startup and getting valuable stock options as part of your compensation package? THINK AGAIN.

You might know that those stock options will "vest" over time, typically four years. The idea is that you earn your way into ownership of these options and that the value of the options is a meaningful part of your compensation during that time. The company could terminate you at any time and you would only be entitled to the options that had vested up to the point of termination. The longer you work, the more you get.

After four long years, you now have "vested" stock options, which means you now have the right to buy a certain number of shares in your employer, and usually your purchase price (which was set at the time you joined) is cheap compared to what the shares are now worth. Once you "exercise" your options and purchase the stock, you are now the proud owner of a valuable asset, and you have the right to sell to someone else and cash out. Right?

WRONG.

There's something that nobody told you when you signed your employment offer many years ago and something you never realized all those years you thought you were earning stock in a valuable company. The company (and its Board of Directors) can arbitrarily stop you from selling the shares without giving you any reason at all.

But what if you wanted to buy a house, pay for your kids education or just diversify your net worth away from this one big asset? No dice. Found your own buyer? Doesn't matter. The company and the stuffy suits on its board will decide when, and if, you are allowed to sell, and could stop you from selling forever.

What if you don't need cash now? Won't your options be worth something when the company IPOs or is acquired?

GOOD LUCK.

There are hundreds of thousands of technology startups in the world and thousands of unicorns. Only a small handful of these companies went public in 2023. Meanwhile tens of thousands of startups go bankrupt every year. There is a high probability that your company will never go public. Or you could go through what happened to Instacart's employees: be one of the rare few companies to actually go public, only to find that your stock is trading 70% below what buyers were willing to pay you before the company went public.

Before you sign that offer, do yourself a big favor. Find out what is the company's share transfer policy. Better yet, get it in writing.

There are ways that companies can exert control and set limits on secondary trading. They can let people sell a percentage of their holding every year. They can limit selling to only those employees with 4+ years of tenure. They can work with marketplaces to pre-approve buyers.

But if they ban you entirely from selling, then I believe that they are depriving you of your valuable property rights.

Do most venture-backed private companies ban secondary share sales by their employees and investors?

The short answer is no

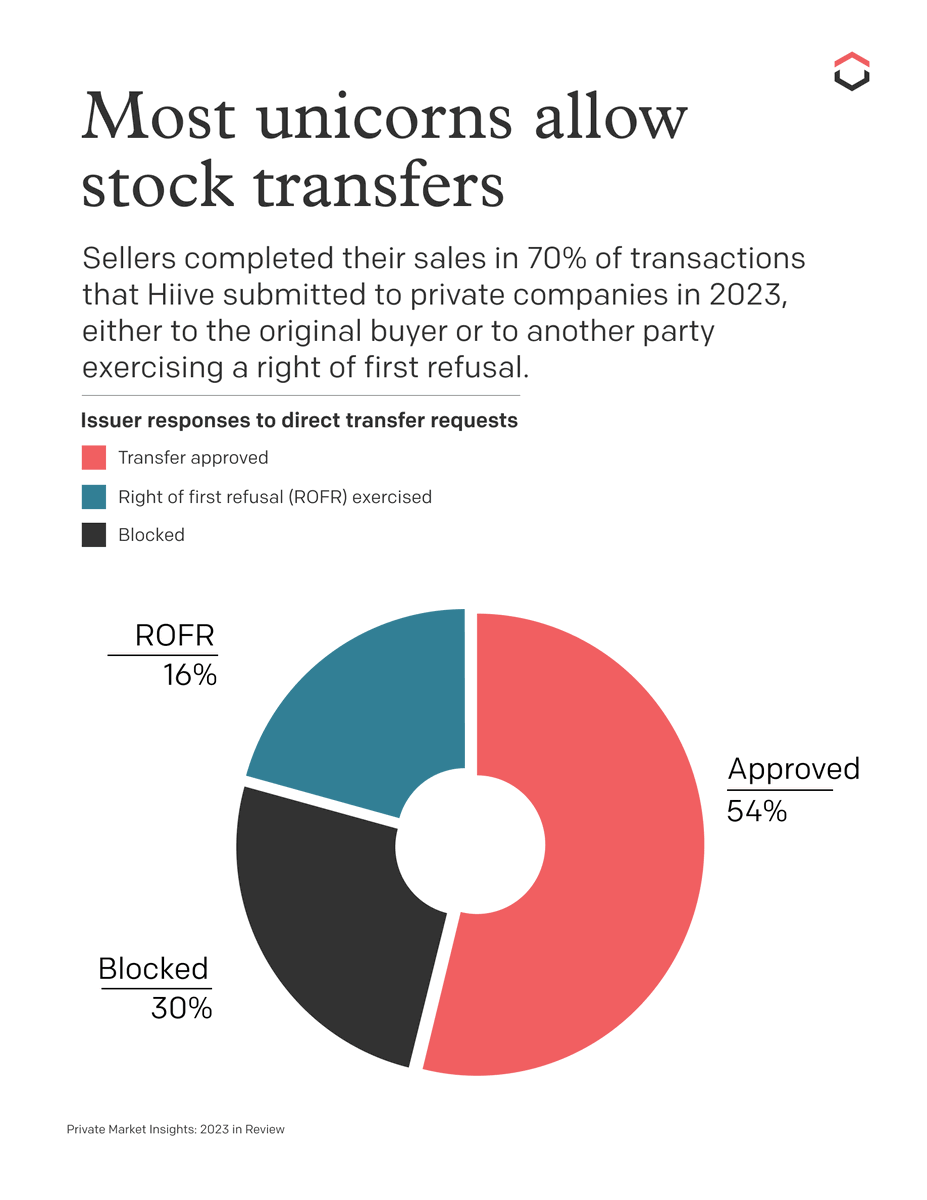

According to Hiive data for the full year of 2023, issuers (the companies) approved 54% of the direct transfer requests we submitted to them, and they or their investors exercised a right of first refusal (ROFR, a right to substitute themselves for the initially proposed buyer) another 16% of the time. They blocked the transaction in 30% of cases.

Therefore, 70% of the time, sellers who found a buyer on Hiive completed their sale.

But there are a number of factors at play

First, the board of directors almost always has a right to block transfers of common shares (those shares held by employees, founders, and pre-seed investors) but usually do not have the right to block preferred share transfers (those held by investors). Preferred share transfers would be included in our 70% number but would be the minority of them, since the vast majority of sellers, by number, are employees.

Companies also sometimes restrict transfers based on how long you have been an employee, whether you are currently employed or not, and how long you have held your shares. Companies will also sometimes control the % of your holding that you can sell within a given year because they want you to keep some skin in the game.

Issuers are also sometimes sensitive to the price of the transaction. Sometimes they don't want the price to be too low because they are worried it will impact future fundraises (I disagree with this concern but will save that for another post). Sometimes they don't want the price to be too high because they are worried about pushing the 409A valuation of the shares higher (I believe that this concern is also overblown).

Overall, companies are becoming more permissive

We are seeing companies increasingly recognize the value of having a liquid stock, both to the company and to the shareholders, and they are allowing relatively free trading, with reasonable controls (for example, we work with some companies on closing batches of sellers every 3 months or so, so that it doesnt become a part time job for the legal, finance and equity management departments).

I do believe that the trend toward greater liquidity and freer trading is inevitable; it's just a reality of capital markets. We are working feverishly to make the secondaries transaction process as seamless as possible for issuers and their shareholders as this evolution takes place.

In the last few months, I have seen the demonization of founder secondaries.

This is BS.

Responsible and proportional founder secondary sales aligns incentives of founders and VCs effectively.

It can totally change downside protection mindset and enable truly going long.