Good chart by @topdowncharts@Callum_Thomas. US cyclicals vs defensive performance (when tech is stripped out) is close to 2011 peak but trends with ISM. Adding tech pushes ratio beyond historic range. My take: Watch this chart for tilt in market leadership when rates tightens. https://t.co/16svGYDpBQ

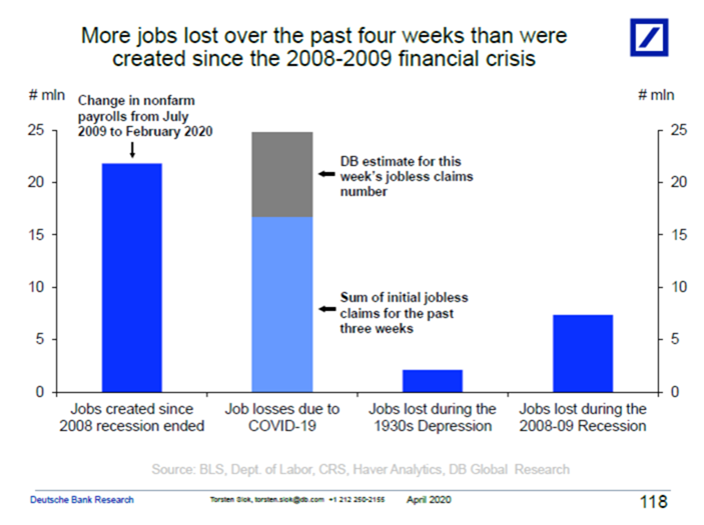

The US economy created 22 million jobs since the end of the 2008 financial crisis. Deutsche Bank thinks we may have lost 25 million jobs just over the past month... In other words, a decade's worth of gains unraveled in four weeks.

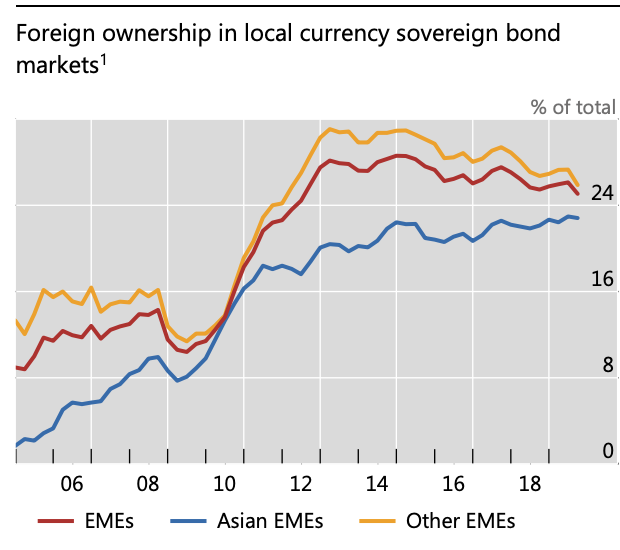

Active bond funds procyclicality with EM bond spreads - liquidity outflows= FX weakeness= risk premia/yield spreads widen esp w higher foreign share. FX reserves mostly to support fundamental CA/FX issues. Global risk off fx/bond sell down unlikely to warrant CB intervention imo.

Escaping original sin?

Lesson of 1990s debt crisis seemed to be to develop domestic currency bonds. But if you have large foreign ownership current crisis shows that it buys you little protection. Great paper by

Hofmann, @ilhyock_shim and @HyunSongShin

https://t.co/3GPywVLP2J

WB projections - uptick in almost all mkts. China growth est 5.9%, ASEAN boosted by low inflation, robust inflows and infra. India FY19 5% growth to accelerate to 5.8% in FY20. Pretty much sanguine forecasts penciled albeit hedging on 'fragile outlook/substantial downside risks'.

@joe_litt@darioperkins@francesdonald Buy/sell forecast US late cycle/softer global growth (barring few EMs-Brazil/India/Russia) & no inflation story. Main inflation views are US wages and margins. An EM OW push requires $ weakness/EM/China multiples expansion/trade risks off but that's rare. Most are tactical and ST

Equity Strategy in a Low Rates World = BlackRock is bullish on Asian telecom for 2020, says it bought stocks it had 'not touched in years' https://t.co/EP91StVd9n

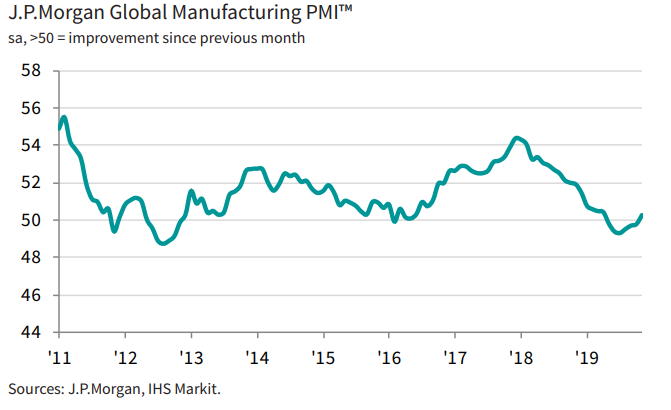

Main takeways - Global PMI New orders index turn +ve for first time since April 19 - key markets US and China saw PMI edge up over prior months. PPI subdued. Manufacturing bottoming along accommodative monetary policies = positives for growth, earnings and equities. #PMI#rates

Global manufacturing edged back into expansionary territory for the first time since April in November, with gains in output and new orders. The slight improvement in operating conditions was largely centred on the consumer goods sector. More here: https://t.co/9pVJtPmYWI

Nice table on monetary trends across DM and EM. Generally subdued inflationary pressure in EM and already negative real rates in DM provide more room for cuts if need be in the EM space. Couple that with positive growth momentum, easing trade tensions, inexpensive valuations. #EM

Major central banks balance sheet tapering on pause and #reversed. Loosening liquidity conditions across major markets provide upside for markets/upgrades.

#liquidity#rates

The combined balance sheet of the Fed, ECB, PBOC and BOJ rose in October by the most since last December: @TheTerminal's Daybreak. Perhaps this is what's driving the melt-up in equities more than anything else....

“The total drag on GDP from the two waves of trade tensions (the black solid lines) is expected to increase through early 2020, cumulating to an impact of just above 1 percent. The effects are similar across the United States, the AFEs, and the EMEs. “

One of the more obvious hit to the HK economy near term would be tightened liquidity - lowered earnings, profits, aggregate financial balances + risks of fund outflows and speculative positioning for Fx weakness. #hk#liquidity#fx#hibor

HSBC raises mortgage cap in HK on HIBOR based mortgages today. This is very interesting as US rates headed lower, HK mortgage rates heading higher? What happens to economies (and RE markets) at maximum leverage when rates go higher? #hk

Preventive policy moves are preferable to reactive moves. Low inflation trends helped bolster latest Fed cuts with some room to spare. But don't expect DXY to fall much on global growth weakness/CB cuts as current risk off lingers. EM fx should continue to stay soft near term imo

Market disappointment as the #Fed favours a preventative cut over a fresh easing cycle: Chief Investment Strategist David Riley gives his latest views on #US rates https://t.co/H38bE3v7br

China's real effective exchange rate has traded more around a band post 2015 as economic slowdown took hold. Expected to stay on the lower/weaker end as US trade tariffs/threats continues, US rate cuts notwithstanding. Also reflects global growth weakness and flight to safety.

@tashecon Peg with some form of capital controls not impossible. Runs the gamut from ban on offshore trading of Lira to temporary or longer term capital flows control in selected transactions. In more direct control cases, similar to Malaysia in 1998.

Not a difficult decision for BI if 1) global economy continues to soften 2) inflation under control 3) US rates and yields continue to fall. Current Indon bond yields, spreads and policy rates provide room for cuts as with recent months' FX built up. #EM#BI#easing#FX

Indonesia’s central bank is discussing the possibility of cutting interest rates but is waiting for the right time, says its deputy governor https://t.co/6qdcwZcYC2