Nassim Taleb: the richest man in the Roman Empire woke up every morning pretending he was poor.

Seneca had more to lose than to gain from his wealth - so he rehearsed losing it. Every so often he'd live on bread and water as if shipwrecked, just to make the downside familiar and harmless.

That's the whole game, Taleb says: arrange your life so you have far more upside than downside - then randomness stops scaring you.

"Make more when you're right than you lose when you're wrong - that's antifragile."

"Always keep more upside than downside from random events."

"The Stoics aren't unmoved by the world - only by bad events."

~70 min, free. the oldest trick for surviving a world you can't predict ↓

Basta con ver qué sectores lo hicieron bien hoy y el viernes pasado para ver hacia donde se va a producir una rotación las próximas semanas/meses.

No creo que haya una caída generalizada del mercado. Simplemente vamos a estar lateralizando, con sectores repuntando más que otros

Only thing the closed strait is making sure of right now is that everyone is selling treasuries.

Yields are exploding higher with the 30Y near multi year highs.

The amount of money this will cost the US via the treasuries that need refinancing via the roll is unreal.

Multi hundred billions to Trillion+.

Markets breaking out above the rates set by the FED.

Remember when the admin was screaming at Powell to lower rates to refinance… crickets

Del minuto 7 al 12 tienes a un señor que trabajó en el fondonde Soros y druckenmiller decirte que es un analista técnico y que no encuentra edge en las valoraciones. Su proceso es macro y estadístico (técnico).

Luego tienes a fontanero inversor decirte que el analisis técnico es una estafa desde un sofa en un pueblo de Gijón

Nice work

https://t.co/orDDJElVgp

Los que me seguís de hace tiempo sé que lo sabéis, pero para los nuevos, que sepáis que yo empecé con 30 años mi carrera laboral, totalmente fuera del sistema después de varios emprendimientos fallidos, en plena época covid.

En el World of Warcraft un tío me regaló un curso de Python en Udemy (él era su creador). Copié su estilo y con eso conseguí dar clases en la academia al lado de casa gracias al camarero del bar, que conocía al dueño y me metió. A 8€/h.

De ahí todo fue tirando del hilo trabajando mucho marca personal en rrss. Las clases fueron a más, me metí en finanzas cuantitativas, y sin ningún plan llevo más de 1.500 personas formadas en 7 años, de muchos países y backgrounds.

Hoy doy clase en varios de los mejores másters, hago consultoría con gente de primer nivel, llegué a tener una mención en el Financial Times, tengo un hustle que "va solo" aproximándose a las 4 cifras recurrentes.

Sé que es sesgo de supervivencia, pero no tiréis la toalla nunca.

Pero Gustavo, en condiciones normales de mercado, cuando un banco crea un préstamo, también crea un depósito y ese depósito se gasta. Mientras el préstamo no se repague, la cantidad de dinero en circulación ha incrementado, afectando potencialmente la inflación.

Un banco no crea un depósito si no se demanda previamente por la contraparte. ¿Son el Estado y el banco central los causantes de incrementar la demanda de préstamos debido a una relajación de las condiciones financieras como tipos de interés o inyección de dinero en la economía? Por supuesto. Pero el mecanismo de generación de inflación no es solamente ese.

¿Por qué el Estado español tuvo una inflación mayor a la media de la UE en el período pre-2008 si el Estado tuvo superávit en 2005, 2006 y 2007?

¿Hubiera Europa entrado en ese período de inflación casi nula en la era post-2008 si los bancos comerciales hubiesen prestado más? Probablemente no. El crédito de los bancos comerciales al sector privado (familias y empresas) estaba creciendo a tasas de entre el 20% y el 25% interanual. Sí, concentrado en unos pocos sectores, pero estructuralmente muy importantes para el país.

Y por no hablar de la banca en la sombra o el Eurodollar, que caen fuera del alcance de los Estados y bancos centrales.

Evidentemente, gran parte de la inflación está causada por lo que mencionas, pero creo que no hay que olvidar el papel de las entidades financieras.

Y esto lo puedes trasladar a la información. Cuánta más nos llega, mayor es el ruido, menor es la señal. Y nunca ha sido tan difícil discernir entre las dos.

Imagina a un tío que simplemente mira los datos ecónomicos una vez al año. Probablemente el 95% de esa información sea una señal, el 5% ruido. Pero si esa misma persona estuviera diaria o semanalmente mirando los datos, probablemente un 95% de esa información sería ruido y un 5% señal.

La oportunidad en LinkedIn no es publicar y hacer ver que "haces y sabes cosas", sino ser el pinguino que escribe 1 vez al mes una pieza interesante, y poder diferenciarte del resto del rebaño. Hoy más que nunca ser real y honesto es lo que está más valorado, pero antes tendrá que nadar un poco a contracorriente.

@KobeissiLetter And sooner or later they will start buying again because they'll figure out the easy or hard way that they need an asset that is liquid and does not lose value in periods of distress. At least not as much as other assets.

@TheShortBear As the war continues, there's only one solution to that in the short-term. And it starts with the letter R.

However, in the mid/long-term, I wouldn't want to be the one who buys duration. At least for the next 5 years, the 60/40 portfolio is dead.

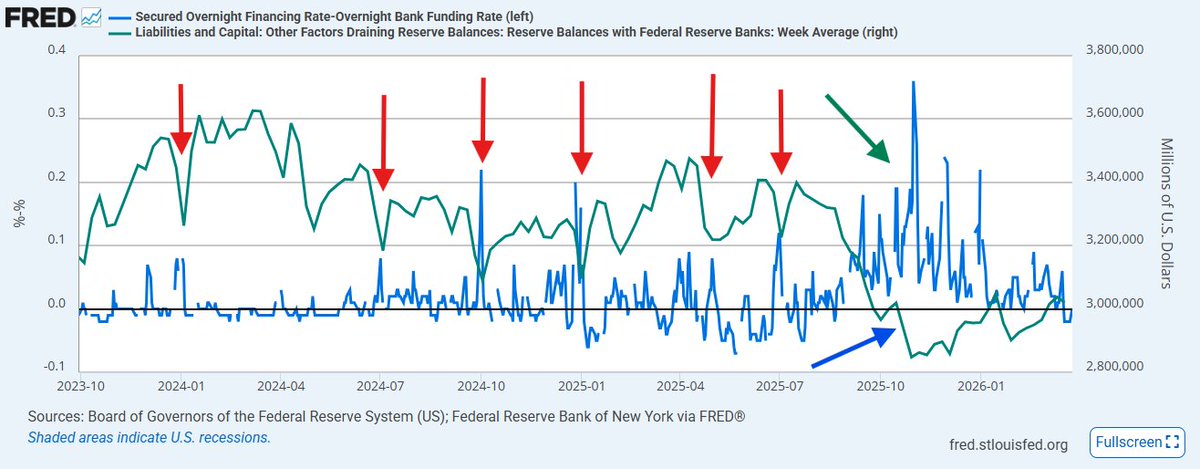

Rising Liquidity Risk into April Tax Season:

Historically, sudden declines in reserve balances held at the Federal Reserve, such as those driven by seasonal tax drains, have coincided with sharp increases in short‑term funding stress.

One of the clearest ways to observe this stress today is through the spread between the Secured Overnight Financing Rate (SOFR) and the Overnight Bank Funding Rate (OBFR). There are many ways to gauge liquidity pressure, but SOFR-OBFR stands out because it is simple, intuitive, and easily accessible through FRED at no cost.

SOFR represents conditions in secured overnight repo markets, whereas OBFR captures unsecured overnight bank funding costs. The SOFR-OBFR spread therefore provides a clean, market‑based measure of liquidity strain across the two core segments of overnight funding. When the spread widens, secured funding is tightening faster than unsecured funding—an early warning sign that reserves are becoming scarce and repo markets are starting to feel pressure. In the attached chart, the red arrows highlight these widening‑spread episodes.

Beginning in Q3 2025, reserve balances fell sharply following the federal government shutdown, reaching new local lows. At the same time, the SOFR-OBFR spread began rising steadily, indicating mounting tension in funding markets. This tightening may have been amplified by the effective exhaustion of the Federal Reserve’s Overnight Reverse Repo (RRP) facility, which previously held more than $2.5 trillion. The loss of the RRP backstop removed a major post‑pandemic liquidity buffer that had helped stabilize overnight rates by absorbing large volumes of excess cash. With the RRP facility now empty, changes in reserve balances feed more directly into night‑to‑night funding conditions, making the SOFR-OBFR spread a more sensitive and reliable indicator of strain.

This leaves the system in a vulnerable position ahead of the April 2026 seasonal tax drain. Reserve balances remain roughly 13% below their levels from a year earlier, and another tax‑related drawdown could trigger a renewed widening in SOFR-OBFR, signaling a re‑acceleration of short‑term funding pressure.

At the same time, money market fund balances have been flat throughout 2026, indicating limited incremental cash available to support repo markets or provide leverage to hedge fund strategies.

With both liquidity and balance‑sheet capacity constrained, hedge‑fund financing channels may come under further pressure in the coming weeks. This could prompt additional deleveraging, reductions in equity and macro exposures, and could amplify downside volatility in equity markets if funding stress intensifies.