WHY DID BRENT DROP TODAY? BRENT JUNE (COM6) FUTURE EXPIRY

I see many people citing "June future expiration" as the reason for today's price drop without clarifying further.

They may find it interesting that exactly the opposite happened on the expiration of the previous - May 2026 future (on March 31st).

On the 2 graphs below:

- green line is expiring contract (May 26 on the top one, June 26 on the bottom one)

- white line is the front spread (May/June for the top and May/June for the bottom)

- orange line is 2nd futures contract (June 26 on the top, July 26 on the bottom).

Brent futures settlement is based on "Brent Index".

Full description is in the document below

https://t.co/XsFY3udeIv

But in broad terms the way the future settles is calculated by averaging 5 observations (volume weighted minute markers) - 2-3 minute periods around 10.30 , 12.30, 14.30, 16.30, 19.30 GMT/BST

AND 3 computation methods.

First two methods are based on the 2nd future contract (so this is what is averaged in the minute markers) and the third - on actual physical cargo trades - for the "First month" (i.e. the month of expiring contract - June 2026 today). There is also EFP involved, but it is a very small piece, so let us ignore it.

This is important - the 2nd future contract plays the key role in settlement of the 1st contract on expiry.

In the first two methods the value for the expiring future (June today) is implied by adding the front spread (June/July today) to the 2nd future (July).

This is the Cash BFOETM (Brent/Forties/Oseberg/Ekofisk/Troll/WTI Midland) front month to second month spread.

I described briefly the cash BFOETM forward in my note on Dated Brent below -

https://t.co/faEDaapUNB

... Normally cash BFOETM is close to the futures price for the same month; however it may not hold when the contract is expiring.

So if we go back to the graphs, we see that on expiry of May contract on 31st of March, 2nd contract (June 2026, i.e. COM6) was stable until 5.30pm (around 107).

But the spread between 2 contracts started to explode after the first sampling period reaching $12 by 5.30pm.

At the end of the day (17.30-19.30) COM6 dropped - so the spread with expiring COK6 increased further (since COK6 was 80% fixed at that time).

Today the spread behaved in exactly the opposite way - it was very high before the first fixing ($9-12, although $12 was reached - it seems - during some liquidation at night time), then dropped to $6 and is not around $4.

So what was going on - why did Brent drop today?

I am not sure :), but I would decompose the problem into 2 parts

1) why did July (2nd contract - CON6) drop

I like the theory linking it to yen carry trade unwind, suggested by @CRUDEOIL231, who I again strongly recommend to follow:

https://t.co/W3UQNsI72y

2)Why did the spread between June and July drop instead of going up like on previous expiry? I do not have a definitive answer, however here are some considerations

- At the end of March physical market was getting stronger and stronger, with physical premiums ultimately reaching as much as $23+ for certain BFOETM grades during the first and 2nd week of April.

So clearly there was strong demand for physical + as @OilCfd pointed out - it is quite possible that traders pushed the premiums higher in the Dated Brent window, similar to what reportedly happened with Dubai crude in March, when Total bought record amount of physical cargoes, achieving mind blowing physical fixings (allegedly making money on the derivatives, that were linked to those fixings).

This time around Dated Brent premiums were weaker and were weakening for last couple of weeks - due to more WTI Midland coming from the US and Chinese buyers reselling the cargoes that they bought in March (possibly expecting to get crude from SPR) - again thanks to for color.

I myself - after seeing what happened with June contract was thinking to take by June positions into expiry, but as the futures (COM6CON6) spread went above $7, while Dated Brent was not as strong as a month ago, decided not to bother and just rolled them into July ....

I could be wrong - as I do not trade physical oil (although I learned quite a bit about it and briefly oversaw a small physical business a few years ago and have friends in the industry) - so if any actual physical traders care to chime in, it would be great.

BEAT THE PODS: A 7-POINT RECIPE FOR SINGLE MANAGERS

There has been some fun discussion here recently about the trend from single manager hedge funds (SMs) to multi-manager hedge funds (MMs or "pods"). Which is very sensical after a year like 2022 where there was a big performance differential between most pods and most SMs. With many SMs well below high-water marks, a year like '22 can also accelerate talent flow to MMs.

In my career, I had the really educational experience of both working at a very well run single-manager fund as well as three well run & well known multi-PM funds. In my role now at Fundamental Edge, I have the pleasure to work both with many top multi-PM funds and single-PM funds. Nothing here will be specific to any of these funds, but simply my high level observations & personal opinions.

I had a friend at a SM fund a couple weeks ago ask me "Brett, you've worked at both, what advice would you give to SM's to compete against MM's?". I also listened to Vinny & Porter's podcast talking about using their learnings from Citadel to accelerate their family office investing returns. Both got me thinking, and I'm in the process of developing a 100+ page deck with some structured thoughts to do some consulting with funds working through this change in the investment ecosystem.

The way I usually use twitter (X) is as a "first draft" of my thoughts. These is my napkin scratch, and I will refine this over time - in that vein I highly welcome your feedback since it helps me improve the thinking.

So, here we go, a recipe for single manager hedge funds to compete when "pods are eating the world".

1) KEEP YOUR TALENT.

Be honest, you expected point 1 to be "leverage time arbitrage" right? I'll get to that point. But in the SM vs. MM market share game, the foundational job as a SM GP/CIO is to keep your team.

The hedge fund world is unique in that even large, well-known single managers might only have investment teams of 6-15 people. And if you've lived in the world, you know that there are often 3-5 truly special investment professionals in that group who have that "nose for money" and are consistent money-makers.

I've seen plenty of SM funds gutted by losing talent to MMs. If the firm has a good culture & internal training & development, a "next person up" approach can work. But turnover of your A+ talent in the ultimate human capital endeavor - investing - is costly & risky.

My advice? Practice preventative maintenance with your talent. The old paradigm of "you should be lucky to work here and I'll pay you whatever I decide to pay you" for a talented 4-7+ year proven money maker just doesn't work anymore. The pods will give that person a $500m-$1bn+ portfolio, 15%+ payout, usually some nice up-front money and the autonomy and alignment that money maker desires. The pitch is compelling, and lots of the top SM talent is biting. (what shines is not always gold, but we will get to that part).

How do you compete?

Money is an obvious vector here. But very few SMs will compete with the bull case for a PM at a MM (i.e. if you build a portfolio to $2bn and make 5% on that you are consistently taking home $10m+ as the PM). And by the time that person has accepted the MM seat, more money isn't likely to sway them (and can set a bad precedent).

What I think matters more is alignment, visibility & a sense of partnership & shared mission. If you have an investment team of 12, who are the 3-4 on that team you absolutely don't want to lose (CIOs, you know who those are). Maybe make them a partner in the fund. Give them a contractual share in the management fee. Give them a 3-year comp plan with P&L contingencies. Your job is to try to create more visibility & confidence in compensation outlook so that the analyst view the SM seat as a higher multiple, more durable comp stream that that person can build a nice life around, even if that comp level falls short of the MM bull case (which it will).

Also, the soft stuff is the big stuff. Celebrate your team's life events, encourage them to bring their kids to the office, do off-sites & outings. Make it a "special" place to work and bring humanity into the day to day.

Understand burnout is a common thing in the 4-7 year range and sometimes burnout leads to exploring new pastures. Consider a sabbatical offering. I honestly loved the part of moving jobs where I got to take 1-2 months off between seats. Build that into your talent development plan.

Work to really articulate the pros & cons of the SM vs. MM seat. Tactfully walk through the risk of the MM seat - drawdowns, risk model constraints, top-line cost flow throughs, high turnover, etc (this is where I think our content will hopefully be helpful to our clients as we break down the MM approach in excruciating detail).

And if all else fails, and you really lose a star, keep an open door. If it were me, I'd let them know they have a seat when they want it. The grass looks greener for them right now, but when they get caught in a 200bps drawdown for positioning reasons and get a capital cut and 2 analysts quit...the grass doesn't look so green. Make it easy for them to come back. And, by the way, the pressure cooker of understanding that way to invest is likely to make them a monster upon return.

2) TIME ARBITRAGE.

This one isn't surprising, but it's true. In my MM teams, I always felt like we had a really good sense of the 9-18 month winners, but it is very hard to express those trades and stick with them. I can't just be long UNH, short WBA and wait it out - particularly if UNH is going to have a 10% pullback and WBA is going to beat a quarter & squeeze.

I run through this math in my deck, but a 20% drawdown on a 15% of LMV (long market value) position in a $50 vol, $1.5bn GMV book ALONE will hit my 150bps drawdown trigger and give me a capital cut. I simply cannot bear that risk as a MM PM - it is existential, as I then need a full 3% / 1-sharpe performance on my 50% book size just to get back to even.

What does that mean in simplistic terms? If I think there is a chance a stock goes down 15-25% before it goes up, I either can't own it or I can't own it in size. With more capital flowing to MMs, and that mathematical constraint true across the board, this behavior starts to create distortions to the price discovery mechanism in the markets.

How does that manifest? Via big over-reactions to near-term squishiness. Maybe a good company with a good 3-year story is going to miss a quarter, and due to that overhang the company has underperformed by 15-20%. Have a bias to lean into those trades.

The hero MM PM makes money 9-10 out of 12 months and limits losing months to under 100bps. That is done via a very sharp process around identifying inflections, revisions, and catalyst driven narrative shifts.

Find the "cheap but no catalyst" stories. Or sometimes the play might just to figure out when pods might want to buy the story and be there 3-6 months before. I came to LOVE situations where there was an obvious catalyst, but the catalyst wasn't coming for 4-6 months. Believe it or not, many traders won't wait that long, but the IRR of waiting can be really superb.

3) CONCENTRATE.

I am bearish on single-manager portfolios of yesteryear with 150+ positions. That is too many, in my mind. Markets are growing inescapably more efficient with alpha windows tighter and alpha pools more shallow. How wide is the alpha load on position 150 in that portfolio? I would submit not wide at all.

If 75% of stocks were fairly valued a decade ago, my guess is that is 90% today. There will always be anomalies & inefficiencies in markets, but the ecology of players has shifted.

The quotient of "dumb money" has decreased due to the secular trend of indexing.

Between quants arbitraging systematic, observable anomalies and pods arbitraging inflections & revisions applying their data & corporate access driven approach, anomalies are smaller.

So the bar should be higher for ideas in your portfolio. Concentration, to me, is the only way for SMs to survive. Find your great ideas and act decisively.

I strongly believe the days of the 40 person, 7-sector single manager 2 & 20 hedge fund are over. Markets won't allow that model to work anymore. The future for SM are smaller, nimbler teams with concentrated portfolios & low latency decisive decision making. It's the only way.

4) WHERE POSSIBLE, ALPHA ISOLATE.

Limited Partners (investors in hedge funds) have become much more sophisticated over the last decade. Particularly around factor attribution.

The MM's are true "alpha factories" in that the return stream is primarily idiosyncratic vs. systematic. That might seem academic, but in a year like 2022 when beta, investor overlay & LT momentum smashed returns at Tiger cubs, it becomes not so academic. MM's performed well last year by using market volatility to exploit idiosyncratic mispricings. If I'm an LP, that's EXACTLY why I'm paying 2 & 20.

I don't want to pay 2 & 20 for a HF portfolio to give me beta & exposure being long LT Mo and short residual volatility. I can do that now with factor baskets. I can buy the Goldman VIP ETF.

You have to give me something I can't get somewhere else for cheaper.

My advice - get a risk model. There are now some vendors who offer off-the-shelf risk models that are as good or better than exist at MMs (Equity Data Science is one of our speakers in Academy). Learn to understand the risk decomposition in your portfolio, learn to do an attribution analysis for your LPs. The good ones will ask for this.

And my advice would be, if possible, to use a portfolio construction approach with a 60-65%+ beta-neutralized idiosyncratic bar with as low a possible correlation to the S&P 500 and GS VIP. If I'm an LP building a portfolio of hedge funds, that's what I want in my stable.

5) RECONTEXTUALIZE EARNINGS.

Given the desire to be a 9+/12 month positive P&L generator and given the drawdown risk characteristics inherent in the 400-600% gross leverage wrapper, earnings season becomes a critical catalyst event for MM portfolios. And not just print day, but the run-up and post-print mis-pricings.

As a MM PMs live for earnings season. The print to print activity was all with an eye towards the next earnings catalyst. The modeling, channel checks, calls w/ sell-side, 2-4 interactions with corporates each quarter, and the end of quarter structured and exhaustive earnings preview process was all done with an eye towards monetizing the volatility inherent in earnings season (print days are 2% of a year's trading days but generate ~20% of idio volatility).

What does that detailed process mean for SMs? Well, earning prints are the ultimate moving bar, the ultimate expectations gap game. There is simply a low chance you are going to compete & win this game consistently in today's market - even if you wanted to, the massive sell-side wallet at MM firms gets them top priority in corporate access & sell-side access. Throw in multi-million dollar alt data budgets and it is an arms race that very few SMs can compete in.

My advice would be to try to re-contextualize earnings as a primarily defensive minded period where the understanding is the SM team might not have the full context of expectations. That seems disempowering, but the alternative of spending ~50% of your research time on the earnings cycle seems like a bad decision too. Listen, will a huge NVDA-like Q1 beat & raise still move stocks? Yes, obviously. Certainly find the inflection in your thesis & understand the catalyst path.

But know that if, increasingly, you don't understand price movement in your space on print day - that's ok. Use earnings as thesis check in. Perhaps do some positioning work (via MM PM friends or spec sales) and look for counter-positioning moves to fade. Company misses MM whisper and get's hate-sold? Take advantage of those counter-positioning moves to leg into positions you like. More react than predict, would be my advice.

6) GO WHERE THEY AIN'T.

Try to understand where pods play to better understand the ecology & alpha pools. Pods generally will really like three things.

1) highly liquid stocks

2) catalyst-rich situations, particularly latent revision potential

3) tangible/reliable downside

The life-blood of the MM model is liquidity. I need liquidity for a couple reasons.

1) I need to risk manage my book in a kerfuffle so I don't get my capital cut. I can't do that if I am 5 days of volume.

2) I am turning over my book 5-10x per year, so with shorter trades I need to get in and out quickly.

Generally my experience trading large portfolios is that anything north of 2-3% of daily volume (outside of a natural cross) starts to create slippage, i.e. I'm pushing a stock up or down. For a 10% LMV position on a $1.5bn book ($75m position), even if that stock trades $100m ADV, that is taking me 33 days to enter, 33 days to exit with minimal slippage.

What does that mean? It means that I might cover 250 stocks on my team, but I REALLY want to cover the most liquid 50. That is really where my P&L is coming from. I will still cover $25-$75m names, but anything under $50m and certainly anything under $25m starts to become very difficult to enter & exit, particularly if I am wrong on a trade and get stuck.

My belief is that the trend toward MM HF's will hollow out the $5-50m ADV competitive set and paradoxically make this a reliable alpha opportunity for the remaining single manager funds.

On revisions, understand that in most sectors the forward trajectory of EPS revisions is deterministic to stock price returns, with some exceptions. A more creative, value driven mindset can surface ideas where the revisions and stock price might diverge.

6) FADE VOLATILITY.

My sense is that there is now over $1tn of gross capital deployed in "short part of the alpha curve" volatility budgeted market neutral HF strategies.

What are the implications?

Well, when a volatility event happens and I have a 1.5-3% drawdown, i.e. my longs go down and my shorts go up, I more likely than now will have to exit that trade after it has gone against me.

In a MM wrapper gross capital effectively becomes pro-cyclical with returns. From the Tiger perspective on things (i.e. "if I like a stock and it goes down for a stupid reason I like i more"), this is non-sensical. If my longs go down 3% and my shorts go up 3% I should take gross exposure higher.

But...LEVERAGE. It is generally believed that MM funds will run with 400-600% gross exposure. Basically a MM hedge fund is like your typical 20% down buyer on a house - if the house value goes down 10%, I'm not down 10%, I'm down 50%. Leverage accelerates outcomes, and in a MM context turns 3% returns on gross into 15 returns on equity via the acceleration dynamics of leverage.

What does this mean in practice? Well, if leveraged players have a drawdown, their reaction to that drawdown is likely to actually ACCELERATE that drawdown via de-grossing of portfolios. If you've spent any time trading the last decade, you know the intensity & frequency of these de-grossing kerfuffles is only increasing.

This is just a math problem. If I run a big book at a pod and I have a 3% drawdown and the pod doubled my book from $2bn to $4bn to try to take advantage of that drawdown and I'm down ANOTHER 3%, it's a huge problem. A risk these funds can't and generally won't take. So there is a systemic risk approach to limit left tail outcomes by truncating your PMs who are underperforming. And it's worked at the GP level beautifully, so I wouldn't expect that to change (if anything, more replicators will come).

What does that mean for you, dear single manager?

These kerfuffles are your friend. Learn to identify them and monetize them. You are the only player at the table who has the capital to step into this kerfuffle. Do the work, but don't be afraid to fade a kerfuffle. Preferably on a beta-limited way, looking for blown out spreads. There are different ways I've monitored for kerfuffle and spread-blow outs and I am building that into my content.

7) UNDERSTAND THE ECOLOGY.

Don't have your head in the sand with regards to the other players in the market.

Great poker players study their opponents more than they study the cards - their approach to the game changes based on who is at the table. Annie Duke was a guest speaker at at analyst training and told us to "run the nuts" against retail investors, play the obvious hand when presented (that's worked beautifully on AMC & GME).

But the poker game changes when you are at a 12-top full of pros. Their tendencies & tells are harder to glean.

The same is true in markets in 2023.

When Buffett started investing professionally in 1956, there were virtually no investors doing fundamental analysis. Reading a 10-K was an alpha generator.

When Julian Robertson started investing professionally in 1980 the fundamental investing hedge fund industry was a cottage industry. You could have a massive informational edge simply with some effort.

The ecology is different in 2023. The hedge fund industry is $4.5tn+ with over 12,000 funds in the US alone. Information is distributed more uniformly. Quants have eaten the alpha on Buffett's favorite factors & turned those factors into beta. And thousands and thousands of sharks are out their looking for any sign of an edge.

My advice, study the players at the table. Understand the incremental buyer of your position - who are you selling it to. Work to understand when the MM, when the SM, when the LO might want to get involved.

And, importantly, spend time trying to understand how the shifting capital players create new anomalies in market. For example, the indexing wave has created a large alpha opportunity for index-rebalance.

It is my belief that 1) the shift to MM biz models in the HF industry is secular not cyclical. Shared overheads, risk diffusion (P&L is additive & risk is sum of squares), the challenges of a SM launch all align to support the view that the MM model is here to stay.

But out of that trend, I also believe that new alpha opportunities will emerge for the enterprising, adaptive single manager.

If you've read to this point, damn that ended up being a LOT longer than I expected it to be. I'd love your thoughts & feedback.

If you are a SM or MM who thought any of this is helpful, please DM me or e-mail me at [email protected]. As I said, I am working on a lengthy deck and some deeper sessions from clients on this front both delivered via zoom & in-person. I will have some capacity for consulting on this front.

Have a great Friday & weekend all!

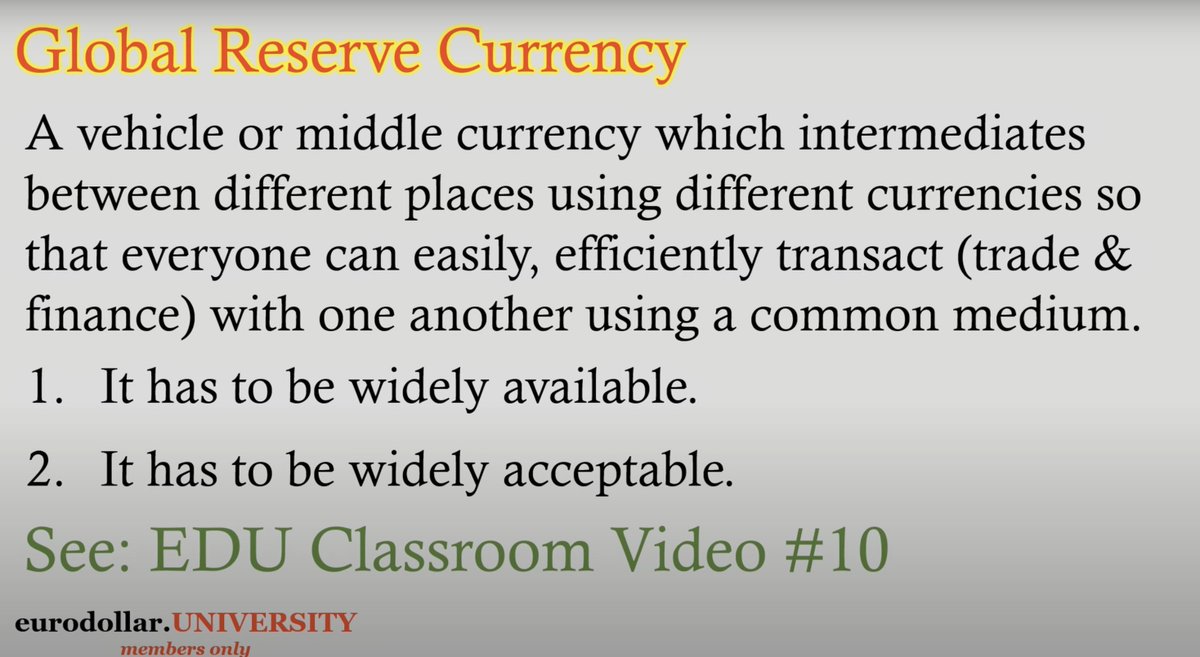

🚨 What is a eurodollar? - (Must Read)🚨

THREAD:

1: The Mystery Begins

The Euro$ is NOT what you think it is. It's our hidden monetary system, lurking in the shadows.

Think of Euro$s as a black hole, hidden yet profoundly affecting everything around it.

The Government doesn't have a monopoly on money; the Euro$ is completely outside the purview of the Fed

2: The Urgent Question

What is the Euro$'s origin? No one is sure!

In the late 1950s, European banks began transacting in US$ claims, creating a network of outside the US.

3: The Birth of Euro$s

A Federal Reserve report from 1960 reveals the emergence of Euro$s as European banks sought dollar deposits for investments.

Euro$s aren’t actual dollars; they are a web of claims and transactions.

4: The Global Money Network

Euro$s enable banks worldwide to transact efficiently, linking monetary resources with needs across continents.

It's more a global communications network than a currency.

5: The Ledger Money System

Euro$s aren't physical dollars; they are ledger claims on US$s, a virtual currency.

Banks create claims and then use them to intermediate monetary needs all over the world.

6: A New Era of Prosperity

Euro$s became the lifeblood of a globalizing economy, facilitating trade and investments on an unprecedented scale.

This system brought unparalleled global prosperity.

7: Unintended Consequences

Euro$ has malfunctioned since ‘07, the world faces risk of undoing decades of that progress.

Competing arrangements can't replicate what Euro$s did so well—widely available and acceptable money.

8: The Ongoing Challenge

To replace Euro$s, something has to replicate its capabilities, an immense challenge.

Global reserve currencies MUST be a highly useful medium.

9: The Final Message

The Euro$ is our monetary system, whether you acknowledge it or not.

Understanding this hidden system is crucial as it affects our lives, not strictly the global economy.

10: Just the Beginning

Dive deeper into the Euro$r system with Eurodollar University's memberships.

Explore its history, fundamentals, and the hidden world of global ledger money.

Join us today at https://t.co/Z5Tb2tXafX. Will you stay in the dark, or take the red pill to uncover the hidden truths about how money truly works?

Very good thread on the mechanics of the corridor vs floor systems & the link with bank reserves and LCR ratios.

To be read in conjunction with @Isabel_Schnabel 's speech from earlier this year.

https://t.co/rSKiYNnQLC

The latest EU MM Contacts Group heavily discussed the robustness of Euribor as a Benchmark rate. Whereas, ESTR has become entrenched as the risk-free benchmark rate, Euribor still has an important role to play. So what is going on?

* Why raising interest rates lowers inflation, and usually (but may not) raises unemployment 🧵

When the CB raises nominal interest rates, agents want to save more in nominal vehicles as opposed to real ones. The relative value of nominal vs real must rise. Inflation must fall.

The BoJ has run the most successful policy out of any CB, hands down.

Also unlike every other CB, it also chose a disinflationary period to adjust policy, while trading it to avoid high rates vol.

This policy makes sense for Japan...just forget about BoJ's balance sheet.

1/

The liquidity drain has begun, with hundreds of billions in reserves set to leave the system. But this reduction could not only fail to subdue risk assets. A squeeze in a covert market will allow the Fed to ease, again without a pivot. The Repo Market Put™ awaits us... 1/

Macrosynergy's "Quantamental Academy":

"How to use quantitative-fundamental information to develop algorithmic trading strategies and backtest discretionary trading principles."

https://t.co/Vxym9r5QDN

Rebalance flows 101

We often hear about portfolio rebalance flows as moving markets. On occasion these flows are substantial and do impact markets. This thread will examine some of the various sorts of portfolio rebalances that regularly occur and ones that are episodic

What do hedge funds and banks like Jane Street, Man Group, and Goldman Sachs have in common?

Internal market price databases.

Any serious quant has a database of prices.

The good news?

It's easy to build one with Python.

Here's how:

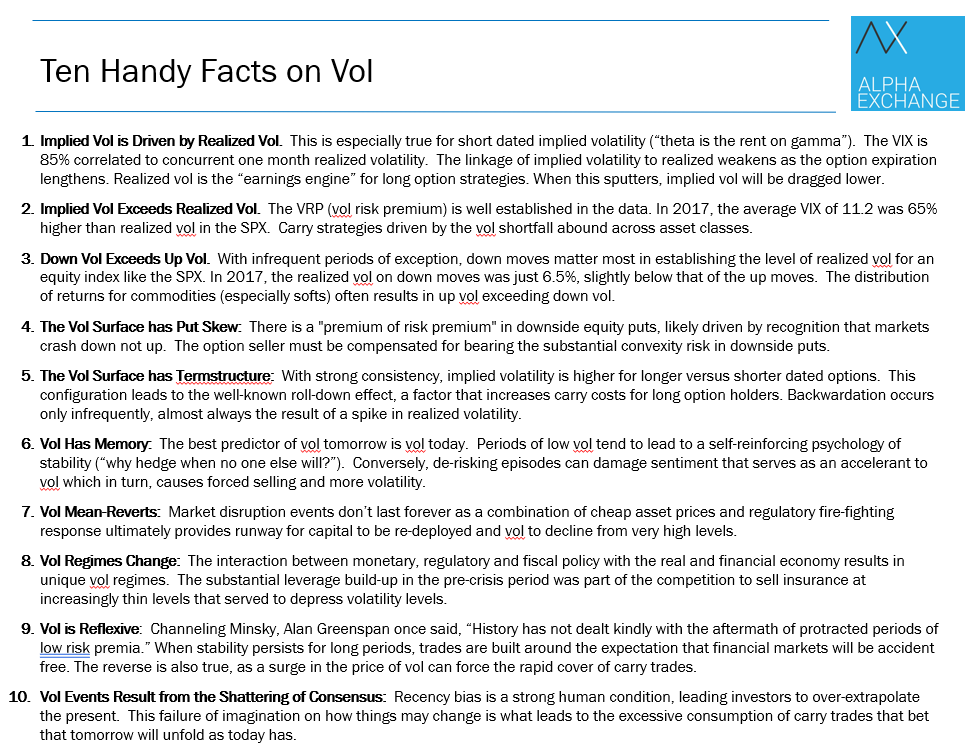

published a short pod on Friday, "Ten Handy Facts on Vol"...here's the list. they aren't really "facts", but observations around the behavior of volatility and option prices. on #5, note the spread between the VIX and 6m VIX future is in 99th %ile (10 years).

This book is a solid introduction to momentum strategies. It's targeted at equities but the principles of momentum translate to virtually any asset class. Highly recommend.

Insurance protecting against brutal Fed cuts this year are still SUPER rich, despite the relative calm.

Calls that protect against a Fed that suddenly cuts >175bp in a year are RIDICULOUSLY expensive compared to puts (which protect against higher for longer).

Explainer.

1/

The Kelly criterion is a formula that determines the optimal size for a bet.

In case you’re unfamiliar:

• Maximizes account growth

• Originally used for betting

• Use it with other risk tools

And of course:

You can compute it with Python.

Ready?

Long overdue... A collection of all my threads, that I started posting from July this year, at one place.

Trading Ratio spreads (more to come)

Part 1: https://t.co/K0twy8dkfX

Part 2: https://t.co/0pcLIqC9oT

+

So much better to think from a multiple-data point probabilistic framework than from a right/wrong framework. While it means you have to accept more uncertainty about what's going on, done well it will improve your accuracy of understanding reality.