We’re very excited to share that Frec has now surpassed $1 billion in customer assets on the platform. 🚀🚀🚀

The speed of compounding is truly astounding.

It took us one year to reach our first $100 million, another year and a bit to get to $550 million, and less than four months from there to reach $1 billion. And here’s the most surprising metric: we added more than $80 million last week alone.

We always had conviction, but to the rest of the world, this milestone marks the moment Frec goes from “there’s something here” to “that is a real business.” We’ve crossed the chasm. Tax-aware investing delivered directly to customers is here to stay.

We’re deeply grateful to the thousands of customers who placed an enormous amount of trust in us.

And I’m also lucky to be working alongside an incredible team that brings so much grit, customer obsession, and passion to our mission every day.

$10 billion and beyond, here we come!

PS - We’re hiring backend and frontend software engineers, quant researchers, and quant developers. Ping me if interested.

When President Trump’s Q1 financial disclosures came out, many people assumed he was actively trading individual stocks. It turns out he was most likely using some form of an automated, managed strategy like direct indexing.

Our team helped Bloomberg’s @justinaknope investigate the nature of the trades. She published her findings in an article that came out a few days ago, linked in the thread.

Here’s the back story.

President Trump’s recent financial disclosures included thousands of securities transactions in Q1 2026, including 3,642 equity transactions. Reporters and commentators quickly raised questions about whether the president was personally trading individual stocks.

During a White House press briefing on May 19, Vice President JD Vance was asked about the trades by @AndrewFeinberg of The Independent. The VP rejected the idea that Trump was personally placing trades, saying, “The president doesn’t sit at the Oval Office on his computer on his, like, Robinhood account buying and selling stocks. That’s absurd.”

Eric Trump later posted on X that the president’s holdings were maintained by third-party advisers through “automated, model-based portfolios and direct indexing strategies.”

Our own analysis points in the same direction. A typical direct indexing account on @frecfinance can generate hundreds or even thousands of trades in a quarter, depending on the index, account size, cash flows, tax-loss harvesting activity, and rebalancing needs.

We also saw patterns that looked consistent with tax-loss harvesting, including sales around market drawdowns.

So there we have it. POTUS most likely uses direct indexing. And with Frec, direct indexing is no longer just for institutions and the ultra-wealthy.

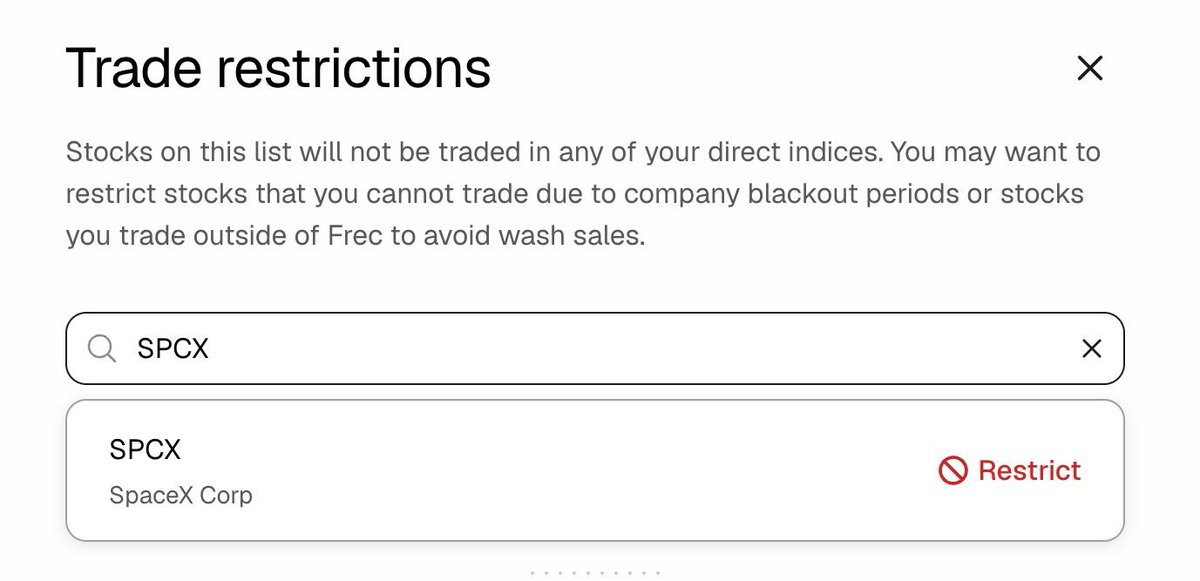

Many customers have reached out about preemptively restricting SpaceX from their direct indices.

As of today, customers can add a trade restriction against SPCX so Frec will not open a position. They will also be able to exclude it from any index that adds it.

It’s worth clarifying where things stand.

S&P Dow Jones Indices: No final change has been announced. S&P is consulting on megacap IPO eligibility changes, but even if adopted, S&P 500 inclusion would still be at the discretion of the index committee.

FTSE Russell: This one has changed. FTSE Russell has introduced fast-entry rules for large IPOs, and based on current public information, SpaceX appears more likely to qualify for Russell large-cap indexes like the Russell 1000.

MSCI: MSCI says it has not changed its rules for large IPOs. Its methodology already includes fast-track provisions for large IPOs, but weights are based on free-float-adjusted market cap, which can limit the impact of a low-float listing.

CRSP / Morningstar: No change, already allows eligible IPOs into its index suite after five trading days if they pass market-cap, liquidity, and other investability screens.

Nasdaq-100: We do not currently support Nasdaq indices, but Nasdaq has also updated its methodology to allow very large newly listed companies to be evaluated shortly after listing, with adjusted rules for lower-float securities.

The broader point is that ETF investors outsource all decisions to fund managers and index providers. When an index changes, they generally have to accept the new exposure and have no say.

Direct indexing gives investors more control. They can restrict individual securities, customize their exposure, and participate in markets in a way that better reflects their own preferences. They can also transition between indices more tax-efficiently, instead of being forced to sell one ETF and buy another.

That is one of the reasons we believe direct indexing is a better ownership structure for long-term investors.

When we first launched Frec, we sent tiny money trees in the mail to our first 60 customers.

We wanted to thank them for betting on us early, funding their accounts when the company was brand new, and trusting us when Frec had almost no customer assets.

One of those customers just sent me a picture of their money tree two and a half years later. It’s amazing to see how much it has grown.

Money trees seem to grow slowly, then one day you notice how far they’ve come. It felt like the perfect reminder of the kind of long-term mindset we love building for.

Many of our customers want more international indices on Frec, and today we’re launching 5 new options: MSCI ACWI ADR, MSCI ACWI ADR Long short, MSCI World ADR, MSCI World ADR Long short, and MSCI EAFE ADR.

Historically, these ADR indices have closely tracked their non-ADR parent benchmarks. For example, in 2025, the MSCI ACWI ADR index showed a 22.36% return (vs. 22.87% for the parent benchmark), the MSCI World ADR returned 21.17% (vs. 21.60%), and the MSCI EAFE ADR returned 32.23% (vs. 31.89%).

We also rolled out a major upgrade to our trading infrastructure. We now trade over-the-counter (OTC) ADRs for our direct index strategies. This gives customers broader market exposure and the potential to significantly reduce tracking error due to the ability to invest in a greater number of the index’s underlying positions. Because liquidity varies widely across the OTC ADR market, we put a lot of work into analyzing these assets and developing a framework to assess their tradeability. This new logic seeks to facilitate OTC ADR trades in a highly cost-efficient way, which ultimately means more efficient portfolio construction for our customers from both a tracking risk and tax perspective.

Existing S&P Emerging and Developed Market ADR indices on Frec will also benefit from the upgrade.

More details on the new indices:

- ACWI, which stands for the All Country World Index, consists of large and mid cap companies in the US, developed, and emerging markets.

- World consists of large and mid cap companies in the US and developed markets.

- EAFE consists of large and mid cap developed market companies.

We’re excited to offer these new options for our customers.

A customer recently switched to Frec's Long Short Direct Index from a fund called the Gotham Triple Advantage S&P 500 Strategy. He stopped by the office last week and shared why he made the move.

For context, there are two primary ways investors put money to work in long short funds: a brokerage account (some call this an “SMA”) like on Frec, or through a fund.

It turns out, there’s a big limitation to investing through a fund.

If you invest $1m and the fund allocates you $250k–$350k of capital losses, those losses may offset your capital gains elsewhere. But the catch is that these K-1 losses are limited by the investor’s tax basis in the partnership. A partner cannot deduct losses beyond their contribution.

Example:

Year 0: customer invests $1m . The customer’s tax basis roughly starts at $1m, subject to liability allocations and other adjustments.

Year 1: fund allocates $300k of capital losses. The customer can use those losses. The tax basis drops to ~$700k.

Year 2: another $300k of losses. Tax basis drops to ~$400k.

Year 3: another $300k . Tax basis drops to ~$100k.

Year 4: another $300k . Only ~$100k is usable; the extra ~$200k is suspended because the customer lacks basis.

A brokerage account can generate more tax alpha because realized losses are reported on a 1099 and can be used to offset gains without those partnership tax-basis restrictions. However, investing through a brokerage account risks creating wash sales if the customer (or their spouse) trades individual names too. This is why Frec gives customers many controls like trade restrictions, do not short lists, and ingests self-directed trades when rebalancing portfolios to avoid wash sales.

Tax loss harvesting is pretty insane

I'm up almost 10% for the year simply investing in S&P 500

But because I use a direct indexing strategy instead of buying an ETF, I have 50K in "tax losses" I can use to offset the gains from selling my startup

Feels like a cheat code

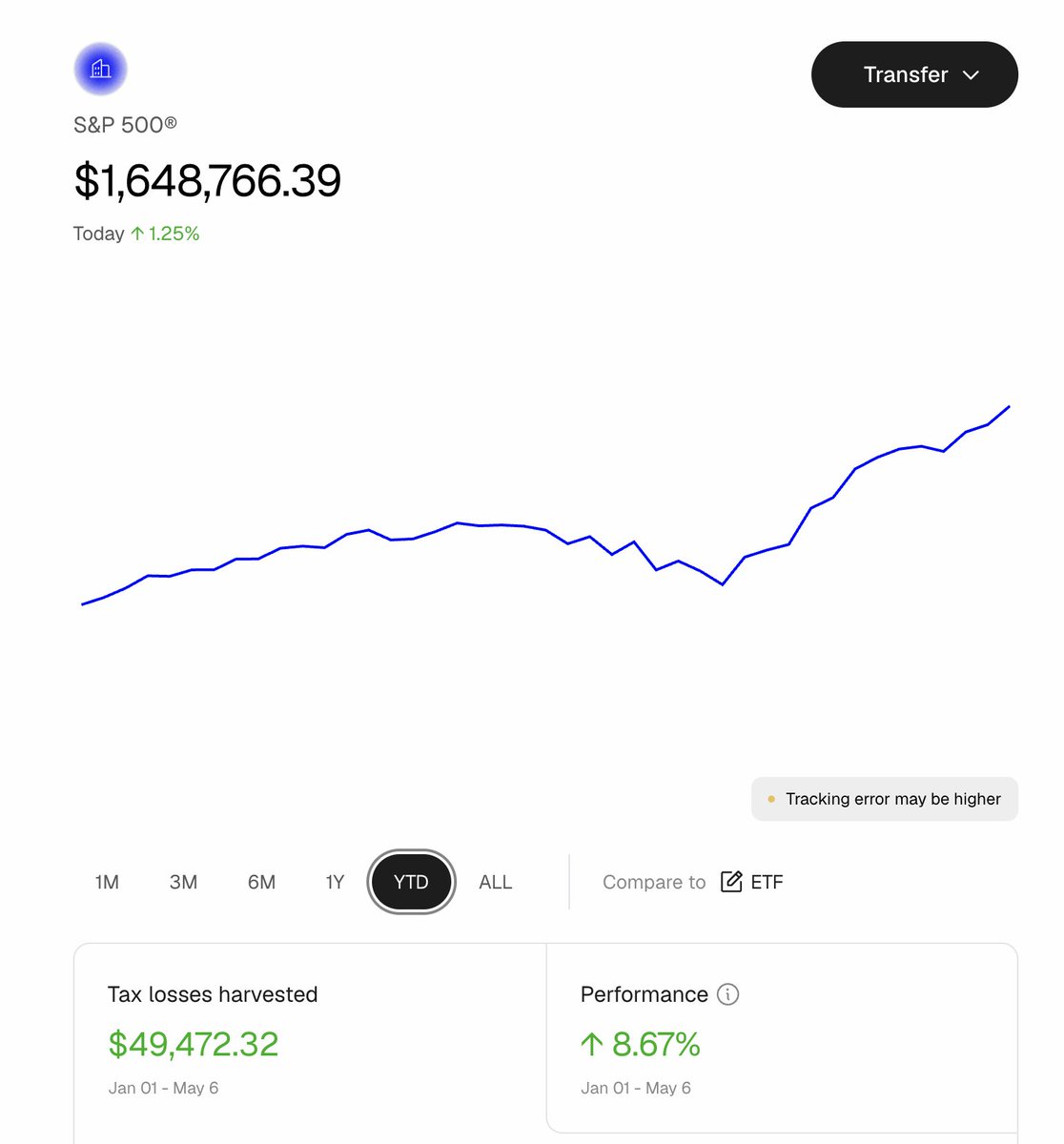

Today’s financial headline is: “S&P 500 continues higher after benchmark wipes out Iran war losses.”

The S&P 500 fell from a peak of roughly 6,945 at the end of February to a low of about 6,343 at the end of March, a decline of 8.6% in just one month.

True story: a customer deposited $5 million into a @frecfinance 140/40 Long short direct index near the top, on February 27.

When the market started declining in mid-March, he messaged me: “I invested at the absolute worst possible time.”

I told him, “I can’t give investment advice, but if history is any guide, you’ll likely be fine if you stay invested.”

He stayed the course and let the direct index do its job.

Today, he has fully recovered and is up 2% on his investment. On top of that, he has harvested $195,000 in losses. He is also outperforming the benchmark by more than 1% in pre-tax excess returns because of the Quality tilt he applied to his index. Quality stocks held up better during the dip.

These sharp V-shaped drawdowns and recoveries are a great example of why someone might choose a direct index over an ETF.

If this customer had invested in an ETF instead, he would have faced two choices. He could have tried to sell and buy back manually during the drawdown to harvest losses, which is harder than it sounds. I know customers who sold near the bottom, waited too long to buy back in, and missed the recovery.

Or he could have simply stayed invested in the ETF and missed the opportunity to capture losses altogether. In this case, the direct index harvested $195,000 in losses, about 4% of the original investment, which could translate into roughly $80,000 in tax savings for a California resident.

We’re very excited to share that Frec has now surpassed $1 billion in customer assets on the platform. 🚀🚀🚀

The speed of compounding is truly astounding.

It took us one year to reach our first $100 million, another year and a bit to get to $550 million, and less than four months from there to reach $1 billion. And here’s the most surprising metric: we added more than $80 million last week alone.

We always had conviction, but to the rest of the world, this milestone marks the moment Frec goes from “there’s something here” to “that is a real business.” We’ve crossed the chasm. Tax-aware investing delivered directly to customers is here to stay.

We’re deeply grateful to the thousands of customers who placed an enormous amount of trust in us.

And I’m also lucky to be working alongside an incredible team that brings so much grit, customer obsession, and passion to our mission every day.

$10 billion and beyond, here we come!

PS - We’re hiring backend and frontend software engineers, quant researchers, and quant developers. Ping me if interested.

From my research... I think that low cost direct index + tax loss harvesting look like a great product.

I'm moving over to @frecfinance, here's $250 if you do too: https://t.co/23WHPpe12g