Even when oil was negative $37 per barrel during Covid Democrats wouldn’t refill the Strategic Reserve.

And now that we need it, they say it’s Trump’s fault.

i gave an AI $50 and told it "pay for yourself or you die"

48 hours later it turned $50 into $2,980

and it's still alive

autonomous trading agent on polymarket

every 10 minutes it:

→ scans 500-1000 markets

→ builds fair value estimate with claude

→ finds mispricing > 8%

→ calculates position size (kelly criterion, max 6% bankroll)

→ executes

→ pays its own API bill from profits

if balance hits $0, the agent dies

so it learned to survive

built in rust for speed

claude API for reasoning (agent pays for its own inference)

runs on a $4.5/month VPS

weather markets: parses NOAA before polymarket updates sports: scrapes injury reports, finds mispricing crypto: on-chain metrics + sentiment

$50 → $2,980 in 48 hours

how much do u think i’ll see in a week?

🚨 GLOBALISM JUST DIED IN DAVOS

Howard Lutnick just walked into the lion’s den — and told the World Economic Forum exactly what they didn’t want to hear.

“Globalism has failed.”

Not whispered.

Not softened.

Declared — on their own stage.

He dismantled the entire WEF doctrine in minutes:

• Offshoring hollowed out the West

• Cheap labor destroyed innovation

• Net Zero made Europe dependent on China

• Sovereignty begins with borders

• Nations must control their industry, energy, and medicine

Then came the line that shook the room:

“Why would Europe agree to Net Zero when they don’t even make a battery?”

That’s the truth globalists can’t answer.

Green agendas without industry.

Climate pledges without sovereignty.

Moral posturing while outsourcing power to Beijing.

America First isn’t isolation.

It’s independence.

And Lutnick made it crystal clear:

The old model is finished.

The globalist experiment has failed.

And the future belongs to nations that put their people first.

Davos just heard the obituary — live.

53 banking associations just wrote themselves a $6.6 trillion protection bill.

They called it the CLARITY Act.

Here is what they do not want you to understand.

Banks pay depositors 0.1% interest. Stablecoin issuers hold Treasury bills earning 4.5%. If stablecoins could pass that yield to users, banks lose the deposit war. They cannot compete. The math is fatal.

So they made competition illegal.

The Kansas City Fed calculated what happens if stablecoins pay competitive rates. Banks lose 25.9% of deposits. $1.5 trillion in lending capacity vanishes. The entire community banking model collapses.

Their solution was not innovation. Their solution was legislation.

The CLARITY Act everyone is celebrating contains Section 404 prohibiting yield payments through any mechanism. Not just from issuers. From exchanges. From affiliates. From partners. Every single pathway to competitive returns, closed by statute.

Brian Armstrong reviewed the 278-page draft for 48 hours. He withdrew Coinbase support at 11pm. The markup was postponed by morning. He saw what Wall Street analysts missed entirely.

This is not crypto regulation.

This is Dodd-Frank for digital assets. Incumbents writing rules that crush competitors. Regulatory capture so brazen they published the lobbying letters on their own websites.

The American Bankers Association. 52 state banking associations. The Community Bankers Council. All coordinating to eliminate an industry they cannot beat in open markets.

Meanwhile China made e-CNY interest-bearing on December 29.

America is banning stablecoin yield while Beijing is paying it.

The crypto industry spent years begging for regulatory clarity.

They got it.

Clarity that $6.6 trillion in deposits will be protected at any cost. Clarity that banks write the rules. Clarity that if you cannot win in markets, you win in Congress.

This is the largest regulatory capture event in American financial history.

And it is being sold as innovation policy.

David Friedberg: California’s “Billionaire Tax” is a Trojan Horse to Go After the Middle Class's Private Assets

@friedberg:

“The reason they're calling it a billionaire tax is to make it easier for people to vote for it, and sign up to this entirely new tax system that they're proposing to put on all Americans at some point, and for the first time ever degrading our private property rights.”

“Forget about how much wealth you have, forget about how rich you are, forget about the term billionaire, millionaire, whatever it is.”

“We're creating, or proposing the creation, of a new tax system that allows the government for the first time ever to come in and audit everything you own.”

“All the jewelry your grandma gave you, the value of all the couches in your house, the value of your car, the value of all your stocks and bonds, and the government can come in, and for the first time, look through the veil into your personal property.”

“And say, ‘Here's how much all this stuff is worth. I'm charging you a percentage of that. That's what I need to get paid.’ And it doesn't matter that it starts with billionaires. What matters is that we're giving the government the right to look into our private property and take a percentage of it every year.”

“The total net worth of billionaires in the US is $8 trillion.”

“The net worth of the US, the middle class, and everyone else is $170 trillion, compared to $8 trillion of the billionaires.”

@chamath:

“They need a way to open the door so that they can go after the real honey pot.”

“The real honeypot is not 200 people.”

@friedberg:

“Just so everyone understands the real goal of this is not to tax billionaires, because there are other ways to tax billionaires.”

“Charge them a capital gains tax if they borrow against their assets that they haven't paid capital gains tax on. Very simple, that can resolve this.”

“Another thing you can do, you can raise the capital gains tax rate. Sounds unpopular. I don't agree with that, but that's another way to deal with this, which is to take the capital gains tax rate from 20% to 30%. You could do that.”

“The real goal of this is to create, for the first time in American history, a private property asset seizure tax. Because they're going after the $170 trillion, not the $8 trillion that the billionaires have.”

Venezuelan man:

“Those who say that the U.S. is only interested in our oil, I ask you:

What do you think the RUSSIANS and the CHINESE wanted here?

The recipe for arepas?"

😂😂😂

A cancer prescription in America…

Costs the pharmacy $7.

Patient pays $17.

When Medicare pays?

That EXACT same pill costs $2,400.

The fraud in this country is worse than we ever imagined…

The GENIUS Act becomes effective January 18th, 2027.

It establishes a stablecoin framework.

Banks can now issue stablecoins.

Non-banks can technically get permits, but it's extremely difficult.

Why this matters now:

The government is still running deficits and printing money,

They need buyers for the new debt they're constantly issuing (Treasury bonds).

The problem is that foreign buyers have been pulling back and buying less US debt.

By requiring stablecoins to be backed by "reserve assets" (which includes US government debt/Treasuries), the government essentially creates a new mandatory buyer for their debt.

Every stablecoin issued means someone has to buy Treasury bonds to back it.

So it’s a way to not pay not down their existing debt—but ensure there's demand to finance their ongoing deficit spending.

However, here’s the problem.

There's a kill switch built in.

Section 126 requires all issuers to have technical capability to freeze, seize, or burn stablecoins when legally required.

It's not optional—it's a licensing requirement.

And this is already happening.

Tether has already frozen $3.3 billion across 7,000 wallets, with 2,800+ coordinated with US agencies.

What does this mean for you?

In every disruption, opportunities emerge.

Payment processors, big banks and companies with massive transaction volume are positioned to profit significantly.

--

This is a short clip from my 20-minute breakdown on the GENIUS Act, how it affects your investments, and positioning strategies before 2027.

If you're interested in watching the full breakdown, comment "GENIUS" and I'll DM it to you.

🚨 JUST IN: The SEC has just clarified rules for how broker-dealers can hold crypto.

These are interim rules while they develop the permanent framework.

This is the regulatory clarity institutions needed to start moving trillions on-chain.

🚨 Crypto regulation was close to a bipartisan win — until timing ruined it.

☝🏼 Charles Hoskinson says the $CLARITY Act had ~70 Senate votes lined up. $Crypto had support on both sides.

Then $TRUMP launched.

Overnight, crypto stopped being neutral tech and became political optics. For Democrats, backing regulation looked like backing Trump. Momentum died.

Result?

#Bitcoin ran. Altcoins froze. Capital stalled.

Framework first. Memecoins later.

Timing cost crypto everything.

🚨 Billionaire investor Ron Baron explains the silent math destroying your wealth.

Your money loses 4 to 5% of its purchasing power every single year. The economy grinds higher at roughly 2%. That is a relentless 7% headwind against you, annually.

What that really means. Prices double every 10 to 12 years. Your savings are cut in half in real terms within about 15 years. Cash sitting idle is not safe, it is decaying.

The system is structurally engineered to punish savers and force capital into risk just to survive.

Banks earn 4.4% on reserves parked at the Fed...

They pay you 0.01% on your savings account.

And now they're lobbying Congress to make sure stablecoins can't offer you anything better.

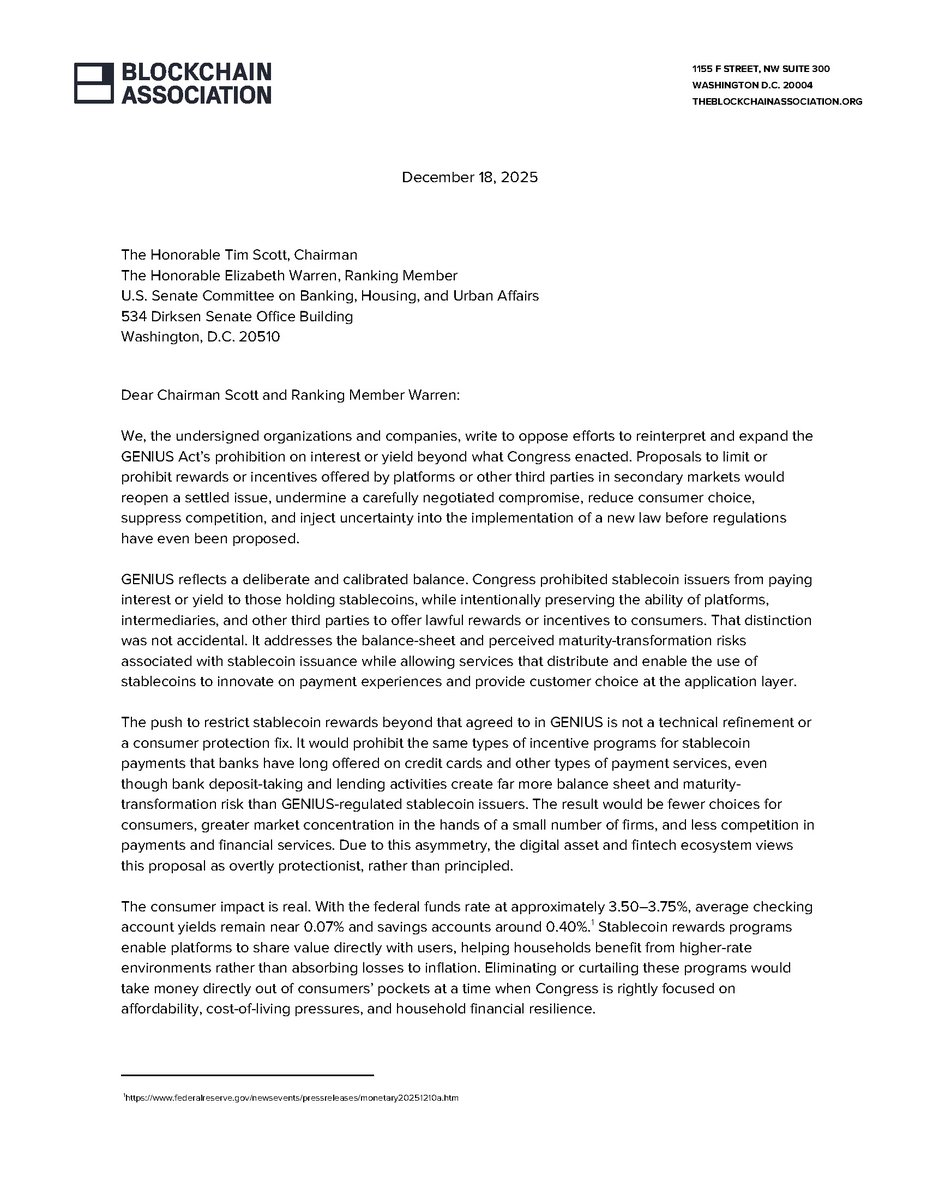

The GENIUS Act already settled this. Congress spent months hashing out a compromise. Stablecoin issuers can't pay interest directly, but platforms and third parties can offer rewards. Done. Finished. Everyone shook hands.

That was a few months ago.

Now the banking lobby wants to reopen it. They're calling it a "safety concern." They're worried about "community bank deposits."

Independent research shows zero evidence of disproportionate deposit outflows from community banks. Meanwhile, the big banks are sitting on trillions in reserves, collecting interest from the Fed, passing almost none of it to customers.

How this plays out for the most part is that your bank takes your deposit, parks it at the Federal Reserve, earns 4%+ on it, gives you basically nothing. A stablecoin platform wants to share some yield with you and suddenly that's a threat to financial stability?

We saw three different lobbying pushes on this bill in the last year & every single time, the framing is consumer protection, but in reality, every single time, the actual effect would be protecting big banks and incumbent margins.

What you should actually watch for:

-Any amendment that bans "rewards" broadly rather than just direct interest payments from issuers.

-Whether the same legislators worried about stablecoin yields have ever questioned why bank savings rates haven't moved in fifteen years.

-Who's funding the "community bank protection" messaging (Usually not community banks lol)

If Congress caves on this, it sets a (not good) pattern. Pass a framework, let the incumbents lobby it back open, chip away until the new entrants can't compete, and crypto companies aren't the only ones watching. Every fintech considering U.S. markets is taking notes on whether legislation here actually sticks.

We signed on to this letter to show our support and conviction in moving the industry forward in the United States. The next six months will show whether the U.S. wants competitive payments infrastructure or protected banking margins under the guise of "stability"

as always, thanks to @BlockchainAssn for their hard work in the industry alongside @standwithcrypto & @na_blockchain

special shoutout to @TBC_Jessi@512mace & @wadepreston for pushing this along as well