Paul Tudor made $100M in one day, Stan Druckenmiller made 1 trade that broke the Bank of England

on one RobinHood stage two $10B+ hedge fund CEOs gave a 30-minute trading masterclass

completely free - two of the greatest traders in history will show you the most important rules of trading

bookmark & watch - this is better than any paid course from fake traders

Welcome to the most asymmetric trade in modern financial history.

The thread below lays out why. The opportunity exists because capital has chased the AI trade while ignoring the physical assets AI requires to run — assets that have quietly become the best-performing asset class of the decade. Since October 2020 when we first called for the commodity super cycle: QCI Total Return +217%, GSCI Total Return +205%, Gold +140%. NASDAQ trails at +130%. S&P 500 at +85%. The top three are all commodities. Yet oil cannot get out of its own way while copper and the broader atom complex prints fresh highs . That is the dislocation. That is the trade.

Get long. Buckle in. Hang on for the ride.

Forgive the longer posts in this thread — attempting to mimic my old 10-bullet commodity takes. On to it.

INSTEAD OF WATCHING AN HOUR OF NETFLIX TONIGHT.

This 1 hour Stanford lecture by Joel Peterson will teach you more about negotiation and getting what you want than most people learn in years.

Bookmark it and give it an hour, no matter what.

Abaxx Technologies Inc. to List on the Toronto Stock Exchange

The Company has received conditional approval to list its common shares on #TSX where its trading symbol will remain unchanged.

Concurrent with the listing, Abaxx will be delisted from Cboe Canada.

https://t.co/iMveIdtPKR

Warren Buffett's Berkshire Hathaway has $400 billion in cash & cash equivalents.

My Berkshire Hathaway holding has become my cash & cash equivalent allocation.

You understand this if you understand owner earnings.

Canada’s household psychology has changed.

That matters more than most people understand.

People are not robots. They do not simply change their minds because policymakers cut rates, increase immigration, print money, or try to restart the real estate mania.

Once a speculative bubble breaks, psychology changes with it.

The belief that “housing only goes up” gives way to doubt.

Doubt becomes caution.

Caution becomes lower bids.

Lower bids become falling prices.

That is how a credit bubble turns into a debt-deflation cycle. ❄️

For years, Canada treated rising home prices as a sign of prosperity.

But much of it was not real prosperity.

It was credit expansion, leverage, and financial speculation.

Now the psychology is shifting.

Young people who were locked out of the market are not desperate to rescue the bubble.

Many are waiting for value to return.

And frankly, after two decades of unaffordable housing, lower prices would be a welcome relief for the next generation.

That is the part many people still do not understand:

You cannot easily restimulate a mania once the public stops believing in it.

Economic Winter is not just about falling prices.

It is about a change in psychology.

And once psychology turns, the old playbook stops working. 🌨️

My thoughts on $BRK

People overcomplicate $BRK because they try to value every piece perfectly down to the decimal. They debate price to book, intrinsic value formulas, and build giant spreadsheets modeling every subsidiary. Meanwhile I look at it much more simply. $BRK has roughly $400b in cash and around $300b in stocks.

That’s about $700b right there between cash and equities alone. So when the company is worth around $1t, you’re basically paying roughly $300b for everything else. That includes the railroad, the energy business, insurance operations, manufacturing, distribution, service businesses, and one of the greatest collections of operating assets ever assembled.

And honestly I think people massively underestimate the value of the insurance float. The float is one of the greatest financial assets ever created because $BRK gets access to enormous amounts of capital at extremely attractive economics. Most people do not fully understand how powerful that becomes over decades. That float has quietly fueled one of the greatest compounding machines in financial history.

But the part that fascinates me most is the discipline. Almost every CEO on earth would have cracked by now sitting on $400b of cash. Most management teams would feel pressure to force acquisitions just to appear active. $BRK has basically said if we cannot find something intelligent to buy at scale, we are willing to wait.

People look at the cash and think it’s dead money, but optionality matters. $BRK effectively owns a giant call option on future chaos. When markets panic and liquidity disappears, $BRK becomes one of the only entities on earth capable of writing enormous checks instantly without relying on financing markets. That is a huge strategic advantage.

The other thing people miss is how rare true permanence is in capitalism. Most corporations optimize for optics. CEOs rotate, incentives change, cultures decay, and strategies constantly shift depending on sentiment. $BRK was built differently.

It was designed almost like an anti Wall Street structure where long term thinking itself became the competitive advantage. In many ways that culture may end up being Buffett’s greatest creation, even bigger than the stock portfolio itself. A lot of companies talk about long term thinking. $BRK actually structured the organization around it.

I also think people misunderstand what $BRK really is. They think it’s just “an insurance company that owns stocks.” But $BRK is basically a giant ecosystem of real world economic activity. Railroads, energy infrastructure, manufacturing, freight movement, insurance, distribution, consumer spending, and financial assets all under one umbrella.

In many ways it’s almost like owning a miniature version of the American economy. But unlike an index fund, the capital allocation is centralized under highly disciplined operators. You get diversification without complete chaos along with durability, liquidity, tax efficiency, reinvestment flexibility, and world class balance sheet.

And honestly the most underrated asset may simply be trust. If $BRK calls during a crisis, people pick up the phone. If $BRK wants to buy a family owned business, sellers trust the company will preserve the culture and operate responsibly.

I also think people are underestimating Greg Abel. Nobody is Warren Buffett and nobody ever will be, but that doesn’t mean $BRK suddenly stops being $BRK. Greg already understands the culture, operational discipline, and capital allocation philosophy better than almost anyone alive.

That’s why $BRK almost a forever asset or a savings account on steroids. No, it’s not going to triple overnight and no, it’s not some hyper growth AI stock. But when I look at over $700b between cash and equities, elite operating businesses, insurance float, fortress balance sheet strength, world class reputation, and disciplined reinvestment talent, I have a hard time viewing it as expensive.

🌹

Agnico Eagle Mines shares are being sold due to new record earnings and the highest margins and net earnings ever. Of course, Agnico made a big strategic mistake. They're using their cash bonanza to buy junior gold miners (see Finland) and buy back shares.

Instead, they should have purchased acres of land for new data centers and bought NVIDIA chips with their cash. Agnico shares would double overnight - easily.

$AEM

I bought a home in Toronto at the exact top of the 1989 bubble.

Spent 4 years deleveraging to stay solvent.

That pain taught me to build the TELTAAM Model.

It's called 2000. It was 2008.

Now it's calling Economic Winter 2026-2047.

🧵

🧵Canada’s housing bubble is visible in one chart.

StatsCan’s new income data confirms the brutal math:

Real family incomes rose.

Real home prices exploded.

Since 1981, Canadian real family income has been up to an index level of 137.

Real home prices are still at 283.

That means home prices are still more than 2x the income-linked level.

My guest today is Paul Tudor Jones (@ptj_official), one of the greatest macro traders of all time.

He correctly predicted the 1987 stock market crash and shorted the Japanese bubble in 1990. For over 40 years, his flagship fund has had a negative correlation to the S&P 500. 100% of his returns are alpha.

He says today's market has so many similarities to 2000, "the easiest bear market I've ever seen in my whole life."

He makes the case for going long dollar-yen, why Bitcoin beats gold as an inflation hedge, and why he was wrong about Warren Buffett.

But what I'll remember most from this conversation is Paul's zest for life. He's 71 and still wakes at 2:30 every morning to trade the London open. He works out for two hours a day. He walks with his wife every evening. He travels the country chasing peak spring and peak fall. He's so excited about the songs picked for his funeral that he wishes he could be there to hear them.

Paul has lived five lifetimes in one. He's one of the most entertaining and interesting people I've met, and the conversation will leave you searching to be as passionate about what you do as he is about what he does.

Enjoy!

Timestamps:

0:00 Intro

1:00 The Kindest Thing

13:19 Trading vs. Investing

17:33 Lessons from Warren Buffet

22:24 The Existential Risks of AI

29:54 The Nature of Trading

31:46 Bitcoin

35:55 Bubbles

42:08 A Day in the Life of PTJ

46:00 Information Overload

47:07 Passion for Markets

50:49 The Robin Hood Foundation

54:18 The Workless World

56:03 Journalism

1:00:00 Principal Components of a Great Life

1:05:06 Kill Them With Kindness

Canada owes more money per family, relative to its economy, than any country on this list.

More than Hong Kong. More than Japan. More than the US.

And the worst part? Most of that debt is mortgages locked into interest rates set years ago that are about to reset dramatically higher, all at once, in 2026.

When households are this stretched, they stop spending. When they stop spending, businesses fail. When businesses fail, unemployment rises. When unemployment rises, people sell homes. When homes flood the market, prices crash. When prices crash, the collateral holding the banks together disappears.

Deleverage before the economy forces you to.

Holy shit, this is some truly expert level analysis

Made me mega bullish on Brazil 🇧🇷

“Brazil is the only large democracy in the world that is simultaneously a food superpower, a water superpower, an energy superpower, a mineral superpower, and a carbon superpower, with export routes that do not depend on any contested strait or chokepoint”

🇨🇦 Canadian homeowners: in REAL (inflation-adjusted) terms, home prices are back to 2016 levels.

Nine years. Zero real return.

The 2020–2022 boom wasn't wealth creation it was a rate-fueled illusion.

BIS Updated data shows Canada now has the steepest real price decline of any major advanced economy.

And the long-term trend line still has -50% more downside to go.

Source: BIS Residential Property Price Database (Q4 2025)

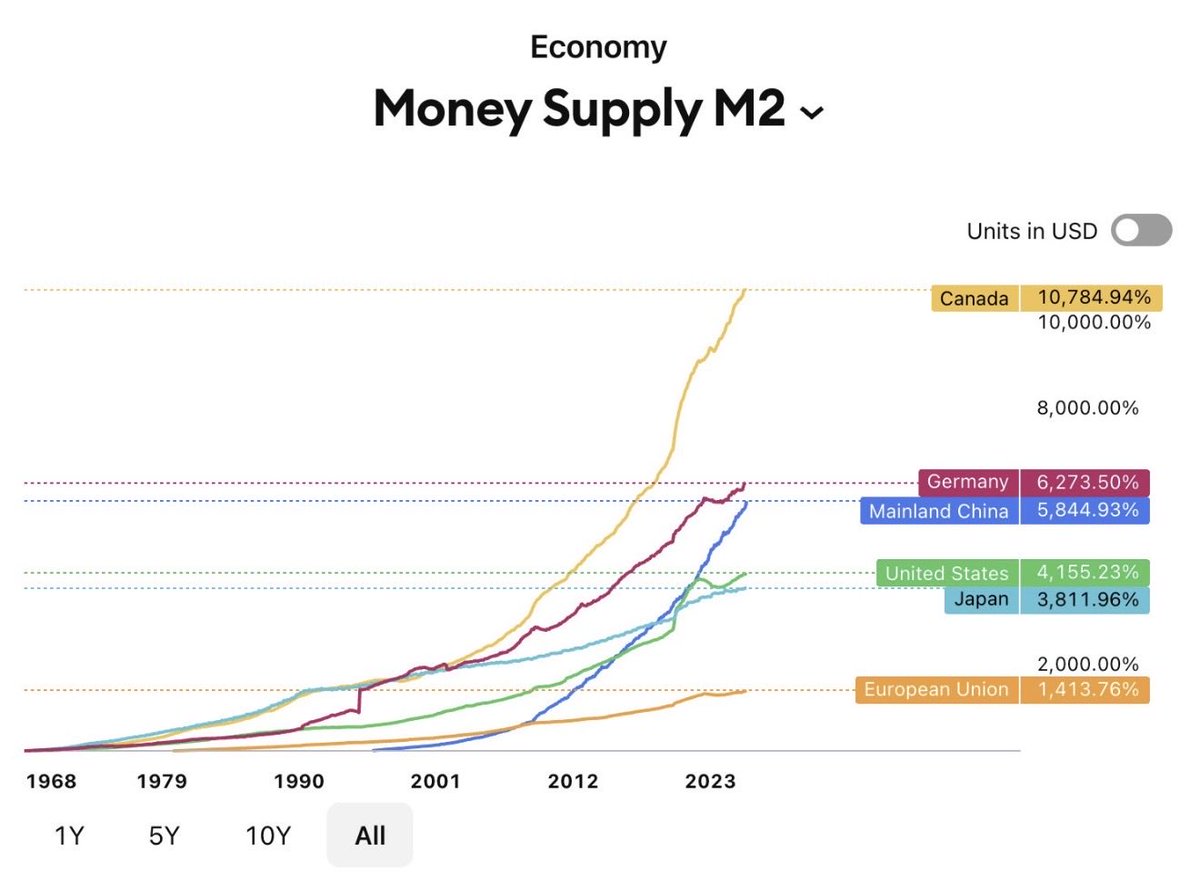

🚨 LOOK AT THIS CHART

Money supply (M2) growth since 1968:

🇨🇦 Canada: 10,784%

🇩🇪 Germany: 6,273%

🇨🇳 China: 5,844%

🇺🇸 United States: 4,155%

🇯🇵 Japan: 3,811%

Canada printed more money than every major economy on earth.

Every other country started levelling off.

Canada’s line goes VERTICAL.

This is why your dollar is worthless.

This is why homes cost $1 million.

This is why groceries doubled.

This is why food bank visits hit 2.2 million.

This is why your savings buy less every single year.

It’s not “global inflation.”

It’s a printing press that never stopped.

IT’S THE CANADIAN PESO.

The government devalued YOUR MONEY to fund spending it couldn’t afford.

This is excellent!! Was going to write something similar, but Radigan beat me to it, and did it far better. You all should read this👇👇 We’re nearing the point of no return…

Canadian subprime lender Goeasy https://t.co/xVuHJwjdJo drops 58% today, but share prices of Cdn banks are up, though the customer base is generally the same. Are investors too complacent about the risks of lending to Cdn households?