Since the Iran war began, there has been a 100 bp swing in Dec 27 SOFR implied rates - from 75 bps of cuts to 25 bps of hikes.

My guess is that we will see at least half of this unwind.

For 2 yrs, it has been a good bet to fade the rate hike calls. This regime is still intact.

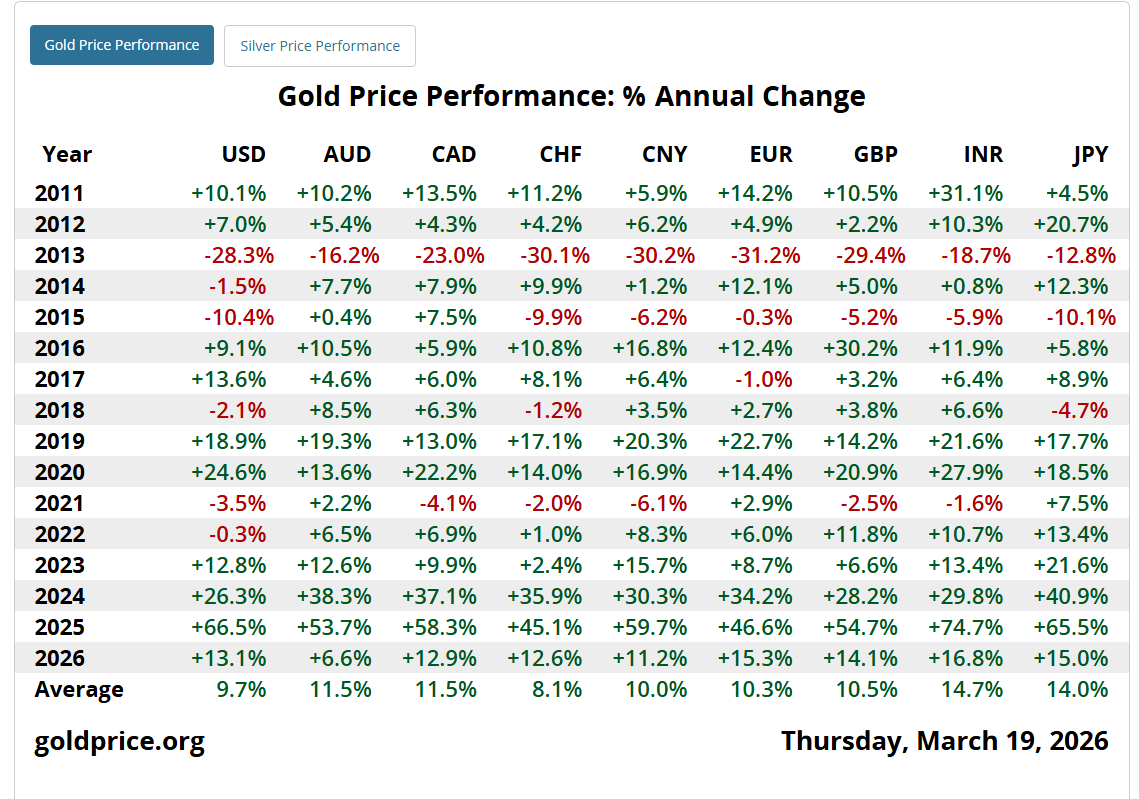

More Central Banks Than Ever Say They Will Buy Gold This Year

More central banks than ever expect to increase their gold reserves, a sign one of the key forces behind bullion’s record-breaking rally remains intact despite this year’s pullback.

In a survey of 74 central banks, 45% said they plan to buy in the coming year, the biggest-ever share in data collected by the World Gold Council and YouGov Plc since 2018. Just one said it planned to cut holdings, the WGC said in a report Tuesday.

In the coming year, emerging-market and developing-economy central banks make up most of the prospective buyers, according to the WGC’s survey. About 53% of those respondents said they expect their holdings to increase, compared with 18% of advanced-economy central banks. (Bloomberg)

Solid(ish) jobs report.

But, too many are extrapolating a labor boom.

Unemployment rate unchanged.

70k leisure/hospitality jobs and 92k jobs from Educ/HC/Govt.

Over the past year, job creation ex-Govt/HC/Education is flat. This is a muddle through labor market still.

When someone answers "What do you think triggered the big stock market selloff Friday?"

They will come up with a large list of narratives, none of which mention positioning: People were choking on calls on Thursday, and purging all those calls on Friday.

ex: $SMH (pink) went from top right on this chart on Thursday (calls priced higher than puts in the +90% %'ile), to puts and calls being equally valued (i.e. center of chart).

Then look at how expensive QQQ options were INTO the Friday vs SPY (Y axis). Tech heavy Qs were massively overvalued related to SPY as everyone over-FOMO'd tech.

Positioning needed a reset.

The Dow was never a great measure of the market. It's price-weighted, which means a $300 stock moves the index more than a $30 stock regardless of company size. The S&P 500 replaced it as the professional benchmark decades ago.

Bond yields over 5% and 2Ys at 4.1% are becoming attractive to long term investors

The more you hear about the 'bond rout,' the more you should become interested

For equities, a post OPEX continuation and tradable low is likely on tap today

Have a super profitable 💰 day!

One of my favorite charts highlighting how heavy the low-profitability tail of the market became in the late 1990s. We continue to see the backdrop as a boom rather than a bubble, providing a higher floor for equities compared to the 98-00 period. Nonetheless, EPS growth expectations are as extreme today as they were in 2000, providing for a market that’s likely to see persistent volatility ahead as expectations ebb and flow. The biggest risk right now is rising interest rates, which has been weighing on market breadth since 2/27, becoming more systemic in recent days as the 10yr moved above 4.50%

📊 𝗖𝗵𝗮𝗿𝘁 𝗼𝗳 𝘁𝗵𝗲 𝗗𝗮𝘆 📊

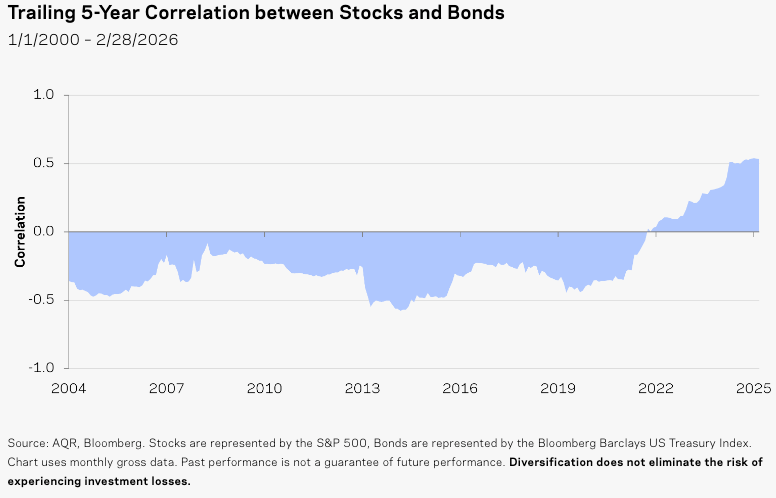

The stock bond correlation was usually negative from 2000 to 2020, but more often positive from 1900 to 2000.

via @CliffordAsness of @AQRCapital

https://t.co/5uDxh1i7IK

Investing Quote of the Day: “Annual income twenty pounds, annual expenditure nineteen six, result happiness. Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery.” - Charles Dickens

Talking oil and the need for an imminent off-ramp w/ @michaelsantoli this afternoon on @CNBCOvertime

Thank you for the conversation Mike!

https://t.co/XDuqKXtPIg

The amount of panic in my inbox over this #Gold sell-off is a good contrarian indicator.

If you are losing sleep over a short-term dip, you aren't looking at the big picture. Gold is still up double-digits in almost every major currency this year.

Don't let recency bias shake you out of a generational bull run. The data speaks for itself. 👇

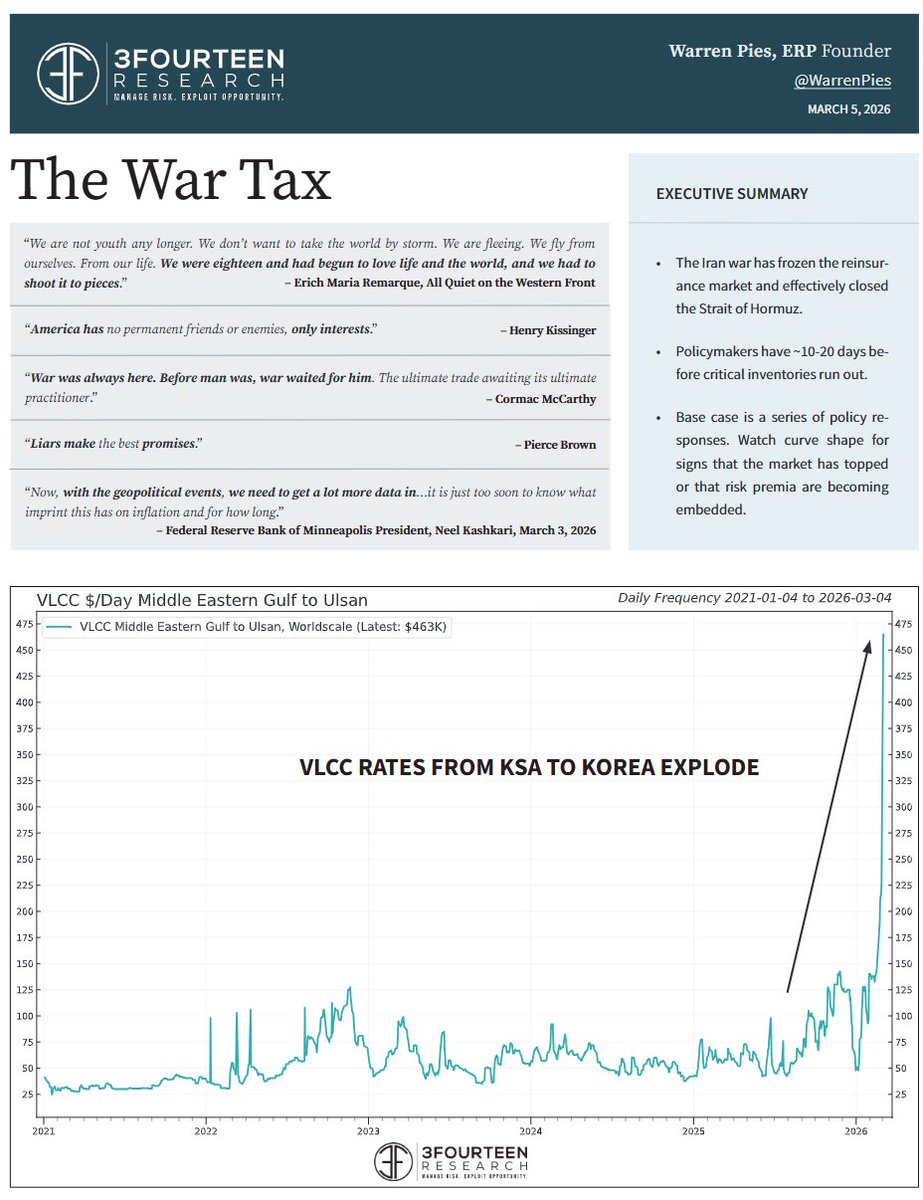

Years before becoming a client of 3Fourteen's institutional research, Warren was my go-to energy guy. This report is a great reminder why. Outstanding.

New report out to 3FR clients breaking down oil/risks:

-Markets need a policy response in the next 10 days.

-Watch the curve for signs of a top (or signs that temporary risk premia is becoming embedded).

-If they adjust policy b/c of supply disruption, Fed is making a mistake.

Global equities flipped since the U.S. – Iran conflict began.

Before the war, U.S. stocks $SPY ranked 39th of 45 global country ETFs YTD. Since Feb 28, the U.S. has surged to #4.

South Korea $EWY, the top performer pre-war, is now the worst performer in the post-war period.