⭕️أكبر مصيبة عالمية تنتج عن أزمة هرمز لاعلاقة لها بالنفط والغاز!⭕️

🌀نظراً إلى شهرة دول الخليج بالنفط والغاز فإن معظم الناس يظنون أن آثار إغلاق مضيق هرمز تتركز في النفط والغاز المسال، لكن الواقع أن أكبر أزمة عالمية جراء إغلاق المضيق لن تكون بسبب توقف مرور النفط والغاز المسال وإنما بسبب توقف تدفق الأسمدة تليها صادرات الهليوم.

🌀والواقع أن إغلاق مضيق هرمز هو أكبر أزمة في حياتنا لأنها ضربت دول العالم كلها من جهة، وضربت القطاعات الصناعية والزراعية والسياحية والعقارات، وعلى رغم تضرر الولايات المتحدة لكنه ضرر على المدى القصير، بينما المنافع على المدى القصير والمتوسط والطويل، والمنافع على المدى الطويل لا تُقدر بثمن لأن إغلاق المضيق يجعل الولايات المتحدة تسطير على تجارة النفط والغاز والغازات السائلة والهيليوم والأسمدة والميثانول والوقود الحيوي، إضافة إلى كل ما يتعلق بالذكاء الاصطناعي، ومن ثم يتحقق الهدف المذكور في إستراتيجية الأمن القومي التي نشرت في نوفمبر (تشرين الثاني) 2025.

🌀ما سبق من أزمات نفطية لا يقارن بما حدث خلال الأسابيع الماضية لأن الأمر في الماضي اقتصر على النفط، أما الآن فقد امتد للغاز المسال والغازات السائلة والهيدروجين والأمونيا والغازات السائلة والأسمدة والهيليوم والميثانول وبعض المعادن مثل الألمنيوم، ونفطياً فالمشكلة ليست فقط بالكمية التي جرت خسارتها وإنما في النوعية أيضاً، فلا يمكن بأي شكل من الأشكال التعويض عن هذه الخسارة لأن معظم النفط المصدر من هرمز من النوع المتوسط الحامض، وحتى لو نظرنا إلى نفط مربان الإماراتي نجد أنه من النوع الخفيف الحامض، بينما أكثر الأنواع الخفيفة في العالم حلوة، وبالنسبة إلى الأسمدة فقد وصل الأمر الآن إلى أن المنظمات الدولية والخبراء بدأوا يحذرون من أزمة غذاء عالمية، ليس بسبب نقص الأسمدة فقط وإنما أيضاً بسبب الارتفاع الكبير في أسعارها، مما يمنع المزارعين حتى في دول زراعية ضخمة من الزراعة لهذا الموسم الصيفي أو الموسم الشتوي الذي يليه.

⚫️أزمة الهيليوم

🔰المستقبل للذكاء الاصطناعي والمستقبل للدول التي تنتج رقائق الكمبيوتر وأشباه الموصلات للذكاء الإصطناعي، بخاصة تايوان وكوريا الجنوبية والصين، وكان الرئيس ترمب أعلن منذ بداية رئاسته الثانية أنه يريد جلب هذه الصناعات إلى الولايات المتحدة، وعلى رغم إنفاق المليارات فإن هذه الصناعات لم تأت إلى الولايات المتحدة.

🔰بدأ الهجوم الإسرائيلي الأميركي على إيران آواخر فبراير (شباط) الماضي، وفجأة تلغي شركات التأمين الأوروبية تأمين الحرب على كل السفن وحاملات النفط والغاز المسال والهيليوم المُبرد في الخليج، وتتوقف الحركة في مضيق هرمز على رغم حروب عدة في المنطقة وآخرها في يونيو (حزيران) 2025، وخلال الهجوم المستمر على السفن في المنطقة الأعوام الماضية لم تقم شركات التأمين بإلغاء التأمين بالشكل الذي فعلته في الخليج، فلماذا؟

🔰نتج من ذلك توقف تدفق الهيليوم إلى كوريا الجنوبية وتايوان اللتين تعتمدان على الهيليوم القطري بنسبة تصل إلى 75 في المئة من حاجتها، واللازم لتصنيع شرائح الكمبيوتر وأشباه الموصلات، وبدأ الهلع يصيب الصناعة، فليس هناك بديل للهيليوم القطري ومخزون الشركات الكبيرة يكفيها لنحو ستة أشهر، والشركات الأصغر لأسابيع والآن هذه الأسابيع تقترب من الانتهاء، ونتج من ذلك قيام الشركات المنتجة بإعادة توجيه الشحنات بحسب الحاجة أو لمن يدفع أكثر، بخاصة بعد الارتفاع الشديد في أسعار الهيليوم، والمشكلة الأكبر هي أن فتح المضيق أمام الملاحة لن يحل المشكلة لسببين، أولاً الهيليوم المبرد الموجود في السفن العالقة يتبخر بعد نحو ستة أسابيع، وجزء من المعامل القطرية جرى قصفها وتدميرها، وكل الأخبار الآن تشير إلى عدم توقف أي من خطوط إنتاج رقائق الكمبيوتر، ولكن هناك تباطؤ وبخاصة في بعض الشركات في الصين، والشركات الكبرى في كوريا الجنوبية وتايوان تركز على الشرائح المهمة ذات القيمة العالية، ولكن الخبراء يتوقعون أن يحدث تباطؤ قريباً، وهذا سيؤثر في صناعات عدة منها الهواتف الذكية وأجهزة الكمبيوتر والسيارات.

🔰الهيليوم غاز خفيف عديم اللون والرائحة وغير سام، يعرفه عموم الناس باستخدامه بنفخ البالونات لخفته، وهو ثاني أكثر العناصر وفرة في الكون وأكثرها خفة بعد الهيدروجين، لكنه على الأرض نادر جداً ومصدر غير متجدد، يُستخرج كمنتج ثانوي من حقول الغاز الطبيعي الغنية به، وفي عام 2025 بلغ الإنتاج العالمي حوالى 190 مليون متر مكعب، ويُقدر بسوق تبلغ قيمتها مليارات الدولارات، ويُعد الهليوم أساساً للتقنيات المتقدمة بفضل نقطة غليانه المنخفضة جداً، مما يجعله الوحيد القادر على تبريد المغناطيسات الفائقة التوصيل إلى درجات حرارة قريبة من الصفر، ويُستخدم نحو ربع الهيليوم العالمي في صناعة أشباه الموصلات لتصنيع الرقائق الإلكترونية، كما يُستخدم نحو ربع آخر في تبريد أجهزة الرنين المغناطيسي التي تعتمد على مغناطيسات فائقة التوصيل لتشخيص الأمراض، وأيضاً في تبريد الصواريخ والأقمار الاصطناعية.

رابط المقال: https://t.co/WU4mZmOc89

The indefatigable genius, Craig Tindale, has done it once again with a deep-dive analysis on the supply crunch of the chemicals needed to make the world go round.

The situation the world finds itself in has never before been articulated as clearly as Craig has analysed it here… All those that care how our world is changing, with absurdly profound consequences, should IMMEDIATELY READ his analysis.

@ctindale explains how chemical reagents have overtaken geology as THE main bottleneck impacting the global supply chain of metals.

An unprecedented shock has been created in the supply of sulphur and sulphuric acid. Initially, this was caused by the closure of the Strait of Hormuz… and further exasperated by subsequent export restrictions imposed by other major exporters of sulphur and sulphuric acid as they protect thier own industries.

As Craig points out, sulphuric acid is essential in the production of critical metals, such as copper, nickel, cobalt, uranium and rare earths… He goes into detail on how the growing contraction in the supply of acid is already impacting the production of critical metals in Chile, Africa, Indonesia and Kazakhstan.

Not to be forgotten is that over 50% of the world’s sulphuric acid is used in the production of fertilizer. The supply shock is also having a significant impact on the security of food supply. Governments have a priority to ensure their populations have enough food to eat at a price they can afford to eat it at….leading to further export restrictions.

Craig forecasts:

1) vertical integration and “reagent security” will become essential to metals producers,

2) the supply of chemical reagents will be weaponized, and

3) technological substitution will accelerate as we seek alternatives to solve our dependency.

Craig’s incredibly insightful analysis even includes a handy Reagent Brittleness Index (RBI), which he artfully uses to create a Sulphur & Acid Supply Risk Dashboard for Critical Mining Assets.

Spoiler: Craig notes that the Kamoa-Kakula Copper Complex in the DRC emerges as a mining operation least at risk to chemical supply shocks, as our new on-site copper smelter becomes a major sulphuric acid PRODUCER for the region.

We are genuinely alarmed by the consequences of the new reality the world finds itself in… take an hour out of your weekend and carefully read it for yourself.

Has anyone else gotten to the donut part of The Pitt tonight, the screen went blank, and their language was automatically changed to Czech? Literally could not change it no matter what I did. #thepitt

Has anyone else gotten to the donut part of The Pitt tonight, the screen went blank, and their language was automatically changed to Czech? Literally could not change it no matter what I did. #thepitt

Is there an AI bubble? With the massive number of dollars going into AI infrastructure such as OpenAI’s $1.4 trillion plan and Nvidia briefly reaching a $5 trillion market cap, many have asked if speculation and hype have driven the values of AI investments above sustainable values. However, AI isn’t monolithic, and different areas look bubbly to different degrees.

- AI application layer: There is underinvestment. The potential is still much greater than most realize.

- AI infrastructure for inference: This still needs significant investment.

- AI infrastructure for model training: I’m still cautiously optimistic about this sector, but there could also be a bubble.

Caveat: I am absolutely not giving investment advice!

AI application layer. There are many applications yet to be built over the coming decade using new AI technology. Almost by definition, applications that are built on top of AI infrastructure/technology (such as LLM APIs) have to be more valuable than the infrastructure, since we need them to be able to pay the infrastructure and technology providers.

I am seeing many green shoots across many businesses that are applying agentic workflows, and am confident this will grow. I have also spoken with many Venture Capital investors who hesitate to invest in AI applications because they feel they don’t know how to pick winners, whereas the recipe for deploying $1B to build AI infrastructure is better understood. Some have also bought into the hype that almost all AI applications will be wiped out merely by frontier LLM companies improving their foundation models. Overall, I believe there is significant underinvestment in AI applications. This area remains a huge focus for my venture studio, AI Fund.

AI infrastructure for inference. Despite AI’s low penetration today, infrastructure providers are already struggling to fulfill demand for processing power to generate tokens. Several of my teams are worried about whether we can get enough inference capacity, and both cost and inference throughput are limiting our ability to use even more. It is a good problem to have that businesses are supply-constrained rather than demand-constrained. The latter is a much more common problem, when not enough people want your product. But insufficient supply is nonetheless a problem, which is why I am glad our industry is investing significantly in scaling up inference capacity.

As one concrete example of high demand for token generation, highly agentic coders are progressing rapidly. I’ve long been a fan of Claude Code; OpenAI Codex also improved dramatically with the release of GPT-5; and Gemini 3 has made Google CLI very competitive. As these tools improve, their adoption will grow. At the same time, overall market penetration is still low, and many developers are still using older generations of coding tools (and some aren’t even using any agentic coding tools). As market penetration grows — I’m confident it will, given how useful these tools are — aggregate demand for token generation will grow.

I predicted early last year that we’d need more inference capacity, partly because of agentic workflows. Since then, the need has become more acute. As a society, we need more capacity for AI inference.

Having said that, I’m not saying it’s impossible to lose money investing in this sector. If we end up overbuilding — and I don’t currently know if we will — then providers may end up having to sell capacity at a loss or at low returns. I hope investors in this space do well financially. The good news, however, is that even if we overbuild, this capacity will get used, and it will be good for application builders!

AI infrastructure for model training. I am happy to see the investments going into training bigger models. But, of the three buckets of investments, this seems the riskiest. If open-source/open-weight models continue to grow in market share, then some companies that are pouring billions into training models might not see an attractive financial return on their investment.

Additionally, algorithmic and hardware improvements are making it cheaper each year to train models of a given level of capability, so the “technology moat” for training frontier models is weak. (That said, ChatGPT has become a strong consumer brand, and so it enjoys a strong brand moat, while Gemini, assisted by Google's massive distribution advantage, is also making a strong showing.)

I remain bullish about AI investments broadly. But what is the downside scenario — that is, is there a bubble that will pop? One scenario that worries me: If part of the AI stack (perhaps in training infra) suffers from overinvestment and collapses, it could lead to negative market sentiment around AI more broadly and an irrational outflow of interest away from investing in AI, despite the field overall having strong fundamentals. I don’t think this will happen, but if it does, it would be unfortunate since there’s still a lot of work in AI that I consider highly deserving of much more investment.

Warren Buffett popularized Benjamin Graham’s quote, “In the short run, the market is a voting machine, but in the long run, it is a weighing machine.” He meant that in the short term, stock prices are driven by investor sentiment and speculation; but in the long term, they are driven by fundamental, intrinsic value. I find it hard to forecast sentiment and speculation, but am very confident about the long-term health of AI’s fundamentals. So my plan is just to keep building!

[Original text: https://t.co/psPlIFRJsi ]

BREAKING: The UK's 30-Year Yield officially crosses above 5.70% for the first time since April 1998.

Despite the Bank of England cutting rates FIVE times in 12 months, yields are soaring.

When you have higher rates with rate cuts, something is seriously wrong.

Guess what the biggest driver of this stock market rally has been? Leverage. For the first time ever, margin debt has topped $1 trillion and has ballooned +25% over the past year. Fully one-fifth of all the leverage supporting the stock market has been built up just in the past year alone; almost half of the outstanding margin debt has come in the past five years alone. That is quite an achievement. It’s also pretty scary.

Scott Bessent had one job.

To sell the U.S. debt to the world.

He’s going to do it with Stablecoins (his words, not mine)

Here’s exactly what he’s got planned:

Gold producers’ margins updated.

We’re living through what could be described as the “Golden Age of Mining”, in my view.

Yet, it’s striking to see that many mining stocks still trade as if gold were below $2,000/oz.

A significant re-rating is still on the horizon, in my opinion.

Stable coins that eat the world will be 100% or more backed with USDTbills, USD reserves, and repo on USD Govies

They are senior secured, designed to never break the buck, and fully backed. Oh they are on chain too.

$MSTR $STRC is junior, entirely unsecured, with a "trust me" rule to protect the buck with a dividend that can be deffered in perpetuity. Oh also can't be levered much and is NOT on chain

Japan is the (potential) black swan no one sees coming, which could derail the current (massive) U.S. stock market mega bubble. #carrytradeunwind#fireinacrowdedtheatre

Agree. That little uptick at far right = US is finally on the right track

But history will not be kind to US leaders who squandered an insurmountable lead, increasing US debt by $31T in 26 yrs on wars & bailouts while not growing US electricity generation AT ALL from 1999-2020.

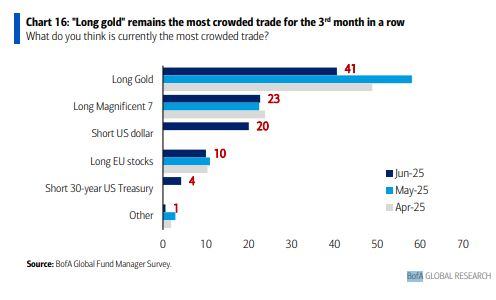

Love how all these active managers say long gold is the most crowded trade each month and yet none of them hold it and instead are up to their eyeballs in equity risk.