* Important: SK hynix has no plans to add any new NAND flash capacity.

=> The only players that will add new capacity are pure-play NAND manufacturers, YMTC, and Kioxia.

- This refutes the previous rumor that SK hynix would add NAND capacity at a new greenfield fab.

- The biggest beneficiary should be Kioxia, which has a greenfield site available for new capacity expansion. Kioxia’s market share is likely to increase.

On Monday we announced an equity offering for Alphabet - part of our multi-year investment strategy to meet the AI opportunity ahead and support the demand we’re seeing from enterprises and consumers. Pleased to share the offering was well over-subscribed. We raised a total of ~$45B, with an additional $40B to come as part of an “at the market” program starting in Q3 (for a total of ~ $85B). A huge thank you to our investors, including Berkshire Hathaway who invested $10B.

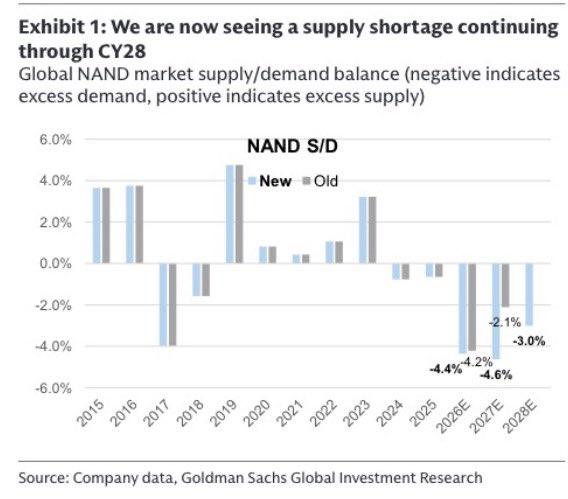

Goldman finally upgrades Kioxia https://t.co/gvV7GGWRoK to Buy and nearly doubled its PT from ¥48,000 to ¥93,000 and got materially more bullish on Kioxia and, by extension, the NAND cycle.

Peak profits are now expected to continue rising through FY3/29 instead of peaking materially earlier!

(++) Goldman now expects NAND supply tightness to persist through CY28

(++) Peak profits this cycle seen materially higher and more sustainable than previously assumed

(++) Samsung, SK Hynix and Micron continue prioritizing DRAM/HBM investment, limiting NAND supply growth

(++) DRAM procurement risk for enterprise SSDs appears largely resolved

(++) BiCS 8 transition expected to drive lower costs and stronger margins over time

(+) IR Day, quarterly results and continued NAND price increases seen as potential catalysts

Goldman isn’t arguing NAND has become a structurally different industry. They’re arguing the cycle itself has changed because AI demand is arriving while supply growth remains constrained.

Same cyclical industry, much higher earnings ceiling.

If NAND supply remains constrained because memory makers keep allocating capital toward DRAM/HBM, that should support the broader NAND ecosystem for longer than investors currently expect.

https://t.co/gvV7GGWRoK $MU $005930.KS $000660.KS

Only a handful of compounders could yield an excess return on invested capital. $MSFT is surely one of those names, so it stands to reason that best-in-calss investors choose to allocate their capital on the mispriced software juggernaut. @joecarlsonshow

As two of the largest forces in equity markets -- growing index ownership and increasing amounts of capital controlled by extremely short-term-oriented, leveraged, volatility-intolerant investors -- converge, we have found occasional opportunities to acquire some of the most dominant long-term compounding franchises at attractive valuations.

For example, we acquired Alphabet $GOOG when the stock declined substantially on the release of ChatGPT in late 2022, Amazon $AMZN in the weeks following Liberation Day, and $META more recently on the market's response to the company's unexpectedly large cap ex guidance and expenditures.

In our 13F which we will file later today, we will disclose a new position in Microsoft, a company we have followed for many years now offered at a highly compelling valuation. While $PSUS will not be filing a 13F tomorrow, it has also recently made $MFST a core holding.

Microsoft operates two of the most valuable franchises in enterprise technology, which account for approximately 70% of the company's overall profits: M365 and Azure.

M365, the company's productivity suite, is the dominant operating platform for knowledge work, with over 450 million workers using Word, Excel, PowerPoint, Outlook, and Teams on a daily basis.

Azure is the world's second-largest hyperscaler cloud platform and, like AWS in our Amazon investment, is a direct beneficiary of the multi-decade migration of enterprise IT workloads to the cloud, which is now further accelerated by surging demand for AI inference workloads.

Both M365 and Azure are underpinned by Microsoft's unparalleled enterprise distribution and the security, compliance, and identity infrastructure it has built and refined over decades.

Beyond these core franchises, Microsoft also owns a portfolio of other leading businesses, including LinkedIn (the world's largest professional network with 1.3 billion members), its gaming platform (Xbox and Activision Blizzard), and search and news advertising (Bing and the Edge browser).

We began building our position in MSFT in February following a meaningful share price decline after the company reported its fiscal Q2 2026 results. We were able to establish our position at a valuation of 21 times forward earnings, broadly in line with the market multiple and well below Microsoft's trading average over the last few years.

Notably, MSFT's headline multiple does not reflect the value of Microsoft's approximately 27% economic interest in OpenAI, which would represent approximately $200 billion, or 7% of Microsoft's market capitalization, at OpenAI's most recent funding round valuation.

We believe Microsoft's recent share price decline has been principally driven by investor concerns around two key issues: i) the competitive positioning of M365 against increasingly capable AI lab offerings (notably Anthropic's Claude Cowork), and ii) the durability of Azure's growth, especially in light of Microsoft's evolving relationship with OpenAI.

In our view, investors underestimate the resilience of the M365 franchise given its deeply embedded role across enterprises and highly attractive price-value proposition. Unlike point software solutions, which may be vulnerable to disintermediation by better-performing AI alternatives, M365 is tightly integrated into the daily workflow of nearly every large enterprise and is supported by Microsoft's identity, security, compliance, and data governance infrastructure, which would be nearly impossible to replicate.

Attractive bundle economics further reinforce Microsoft's advantage, with monthly average revenue per user on the M365 suite at approximately $20, less than half of what customers would pay to purchase the underlying applications individually from different vendors.

Moreover, we are encouraged to see Microsoft prioritizing its R&D efforts and investment in Copilot, its own AI agent embedded across M365, with direct involvement from CEO Satya Nadella. We believe these efforts will translate into improved product velocity and greater customer adoption over time.

Alongside Copilot's rollout, the company has also begun shifting its pricing model from pure per-seat licensing to a hybrid model of seats plus metered consumption, which helps expand the company’s revenue opportunity as AI agents drive incremental usage that a seat-only structure would not capture. These initiatives should help sustain M365’s strong underlying growth momentum, which was already evident in the business unit’s 15% revenue growth (in constant currency) last quarter.

We believe concerns regarding Azure's growth trajectory are similarly misplaced, particularly in light of the franchise's exceptional recent performance. Azure revenue grew 39% in constant currency last quarter, with company guiding to modest acceleration through the second half of the year.

We view Microsoft's recent decision to restructure its OpenAI partnership not as a concession but as part of a deliberate pivot toward a more open, multi-model architecture that better serves enterprise customers, who increasingly seek optionality across model providers.

Microsoft recently disclosed that over 10,000 enterprise customers have used more than one model on Azure Foundry, the company’s modular AI model marketplace. This model-agnostic approach also strengthens Copilot, which can auto-route queries across multiple models to deliver the optimal output for a given task.

To support Azure's rapid growth amid persistent supply constraints, Microsoft has raised its calendar year 2026 capex budget to approximately $190 billion. Consistent with what we have observed at hyperscaler peers Amazon and Google, we view this spend as growth capex that should drive future revenue generation. This is particularly true for Microsoft, given that roughly two-thirds of its capex budget is allocated to server and networking equipment that correlates directly with near-term revenue.

Like our purchases of $GOOG, $AMZN, and $META, we believe that $MSFT offers analogous and compelling long-term value at today's valuation.

@joecarlsonshow $MA looks a "low-hanging fruit", since the stock price has almost moved sideways this year while free cashflow is on the rise, a recipe for multiple expansion.

@joecarlsonshow $SPGI has unfairly been underpriced against the rest of the four holdings. Given almost 90% of its revenue comes from subscription-based fee, steady cashflow is nearly guaranteed, which can be reinforced by pricing power.

@long_equity

I'm a firm believer that Quality Growth Investing prevails over market noise and let your wealth compound in the long run. Here's an empirical study that bears out the relevance of free cash flow and there's a way to get multi-bagger winner.

https://t.co/riHK90fQJt

"at fault": if someone is at fault, they are responsible for something bad that has happened

ex. The police said that the other driver was at fault.

ex. Some people claim that it is the UN that is at fault.

"at fault": 責任がある

Trump and others in his administration have insistently claimed that the “radical left” is now disproportionately to blame, while prominent writers and think tanks have asserted that the right is more at fault. @ForeignAffairs

Nvidia CEO Jensen Huang goes one-on-one with Jim Cramer https://t.co/jLcl2ZhN2R via @YouTube

Jensen knows how to navigate the AI industry as a full-stack AI infrastructure, playing a key role in ensuring everyone is benefitting from the renaissance of artificial intelligence.

"have/take pride of place": to have the most important position in a group of things

ex. A portrait of his grandfather takes pride of place in the entrance hall.

ex. A large photograph of the children had pride of place on the sitting room wall.

"pride of place": 最高位

When it comes to rewarding resistance to the United States, there is no better symbol of this promise than Xi’s decision to give pride of place during the military parade in Beijing to North Korean leader Kim Jong Un.

@ForeignAffairs

"oxymoron": a deliberate combination of two words that seem to mean the opposite of each other, such as ‘cruel kindness’

ex. Compassionate capitalism is not an oxymoron.

"oxymoron: 矛盾語法

In principle, a riskless export control license is an oxymoron; licenses are required only when the government has identified a risk. It did so for the H20 chip just a few months ago, in April.

@ForeignAffairs