2/2

But, as I explain in my latest Substack piece, they may be framing the issue incorrectly. This isn't a question of whether government should intervene in the economy so much as it is a question of which government should intervene in the economy.

https://t.co/f3mjSqJhdh

1/2

The FT warns in this editorial that Europe and the US should be wary of allowing government to play too important a role in driving the economy.

https://t.co/kOKCkfykUL

The new @phenomenalworld issue on American power is well worth reading. The key question is whether we are seeing the decline of US hegemony or a disorderly, openly coercive reorganization of imperial power /1 https://t.co/KXxjqZzvI6

THREAD: The collapse of higher education in the UK is misunderstood by almost everyone involved. We are told it is because of volatile international student markets. The truth is more to do with real estate and capital investment. Here is what is going on: in places like the US

@bankofengland this didn't make it into the published version:

the US Federal Reserve bought about $240bn inUS Treasury bonds since dec 2025.

Imagine the outcries about central bank independence if the Bank did this here

The Pettis–Tooze divergence may actually be quite straightforward.

Pettis is looking at the financial economy: debt, bad investment, suppressed consumption, and losses waiting to be recognised.

Tooze is looking at the real economy: factories, batteries, EVs, solar panels, supply chains, and industrial capacity.

They are connected - loosely-coupled - but they are not the same thing.

In a fiat world, that distinction matters more because the tie between financial claims and real output is looser, more political, and more discretionary than it was under gold.

A bubble in finance does not automatically destroy productive capacity. And productive capacity does not automatically validate every financial claim written against it.

That is why both Pettis and Tooze may be right at the same time.

Pettis sees the distortion in the claims.

Tooze sees the strength in the capacity.

The real question is how the state manages the gap between the two.

Under gold, that gap had a harder edge. Bad claims could persist for a while, but they eventually ran into the convertibility constraint.

Under fiat, adjustment can be deferred, socialised, refinanced, inflated away, repressed, or pushed through the fiscal state.

That is the post-1971 world: the financial economy can lie for longer, the real economy can endure beneath the lie, and the state decides how violently the two are made to meet - and who bears the loss.

Pettis: https://t.co/gbbZbqorEJ

Tooze: https://t.co/OhXxCDhdGL

#ElasticEconomics

#FunctionalFinance

#MalleableMonetarism

Great description of the European trade relationship with China from Jens Eskelund:

"it’s a 400-metre-long giant container ship loaded with 24,000 containers going to Europe and coming back almost empty"

1/3

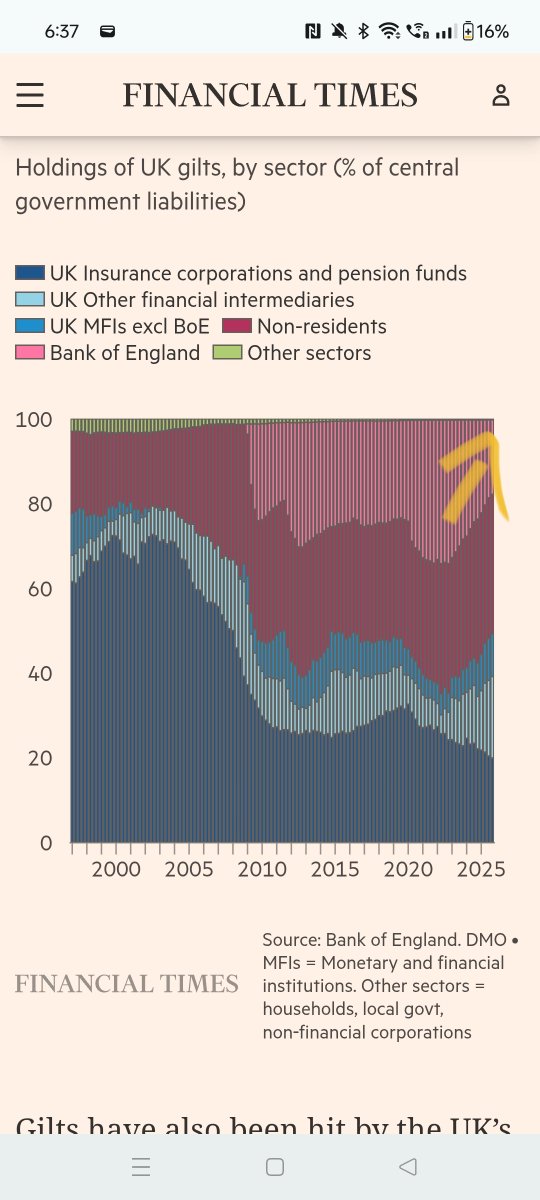

Bank of England was until recently largest holder of gilts.

It's been aggressively selling for no good reason other then Bailey wants to.

We have a Bailey premium on gilts nobody talks about

Bond vigilantes have repeatedly told @bankofengland that its aggressive QT actions were increasing Bailey premium.

the Bank's response was to stop asking them!

@adam_tooze@AndyBurnhamGM

This is more revealing as a statement of what education was like (and might still be like) for Chinese elites than for what it says about Xi (aside from the personal touch about Hemingway). Jack London stands out: very highly regarded in communist world as exemplar of naturalism and for his own socialism). In those terms, Heminway was continuation of London while Thoreau, Whitman, Twain can be seen as forming a line of enlightened-progressive-democratic writers.

The Carter Doctrine is gone, Hormuz is shut, OPEC is falling apart.

The global oil economy is entering a new period of instability. And it's because of US action (or inaction). The consequences will be profound. My latest for @nytopinion https://t.co/J0YopCoDJg

Extraordinary EU energy development: The Belgian Government has just announced it intends to buy all seven nuclear units from owner Engie.

Perhaps 3, 5 or more reactors are now potentially going to be saved and restarted. Decommissioning work may be stopped immediately.

Everyone's been waiting for "the European Amazon" for 20 years.

Turns out it might be a discount grocery chain.

Dutch Central Bank just picked Lidl as its cloud provider. Not AWS. Not Google. Not Microsoft. Lidl.

The reason: trust in US tech is eroding across European institutions. Data sovereignty rulings, the political climate, tariff drama. Every quarter the case for sitting on top of US infrastructure gets harder to defend.

So Europe is decoupling. Quietly. Contract by contract. While everyone watches the political theatre.

Lidl pulled in nearly €2B from cloud last year. All infrastructure built inside the EU.

The "European alternative" people have been waiting for?

Turns out it's a grocery chain that's been quietly investing for years.

If a discount supermarket can win central bank cloud contracts, is US big tech's moat in Europe thinner than anyone admits?

Last place anyone was looking. First to deliver.

The idea of removing defence spending from the scope of fiscal rules is gaining traction. Andy Burnham mentioned it yesterday (“There’s certainly a case, when we look at the pressure on defence spending, to consider that exceptionally outside of the rules”). What might this mean?

Decades of sanctions appear to have turned Iran into a major industrial power. This is maybe the most surprising and important new thing I have learned from the present war. The 7 countries with the capacity to produce advanced heavy-duty gas turbines are United States, Germany, Japan, Italy, South Korea, China, and Iran.

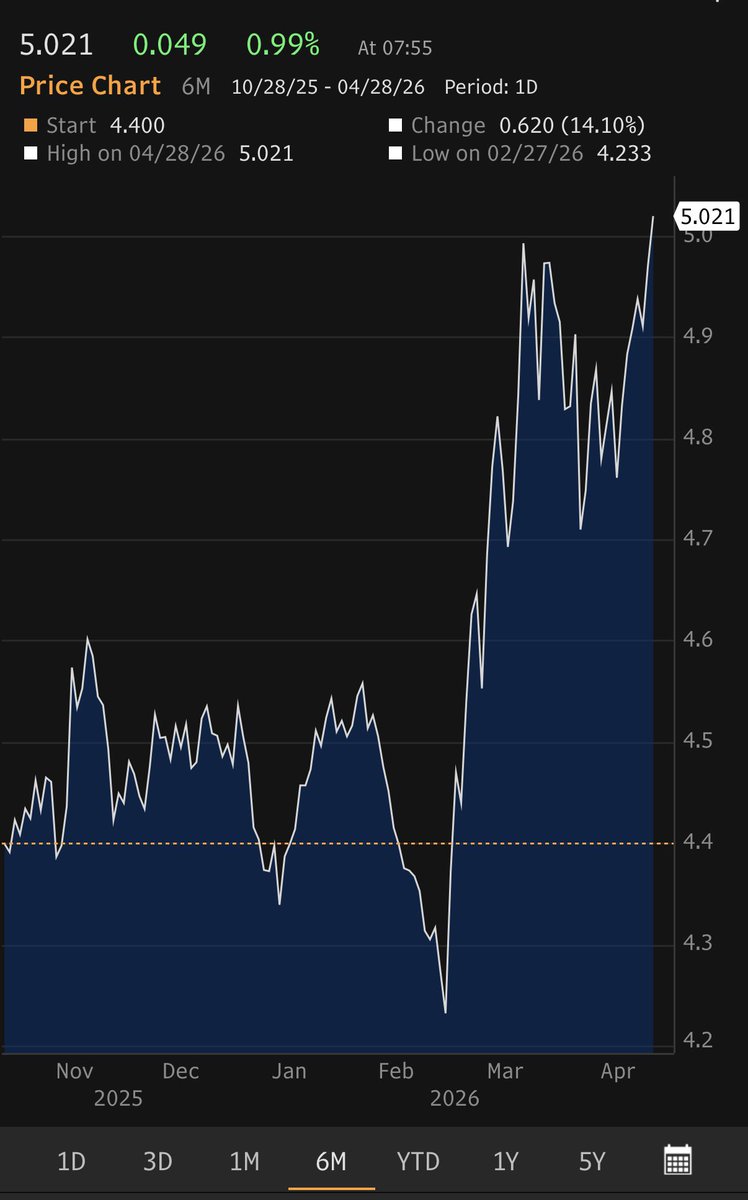

It's a good job the UK can lean on its strong real GDP growth and solid fiscal trajectory, because this sort of thing would look quite worrying otherwise

Unfortunately for the UK’s growth and fiscal outlook, it has become a near certainty:

Whenever global interest rates rise due to a common external shock—in this case, higher oil prices—British borrowing costs increase more than most others (as illustrated in this CNBC table for 10-year government bond yields).

#economy #uk #markets #debt #bonds #growth