🚨ALERT: ETHEREUM RSI HITS LOWEST LEVEL SINCE LAUNCH

$ETH’s RSI has fallen to its lowest reading on record, signaling extreme oversold conditions as selling pressure intensifies.

PYPL PayPal.

Down massively from its peak. Now trading at ~8x earnings and ~8x free cash flow. Dirt cheap for a business this scale.

439 million active accounts. $1.79 trillion in annual TPV.

Wall Street has written it off. Meanwhile the business keeps printing.

Copper can't keep up with AI. That's not an opinion, it's physics.

Every data center being built right now is replacing electrical connections with light. NVIDIA confirmed it with $4.5 billion in direct investment.

I mapped 25 public companies across the photonics value chain:

Every AI cluster being built today hits the same wall. A hundred thousand GPUs mean nothing if the data can't move between them fast enough. Copper maxed out years ago and photonics replaced it: lasers, optical fiber, and transceivers that push data at the speed of light. The AI transceiver market doubled in two years. NVIDIA committed $4.5 billion across three photonics companies this year alone. This is where the infrastructure money is going.

Here's the full value chain:

🔬 MATERIALS & WAFERS

This is the bottom of the chain. Every laser and transceiver starts as a wafer substrate: indium phosphide, gallium arsenide, germanium, specialty glass. Nobody above this layer can produce anything without these inputs, and right now the most critical one, indium phosphide, is the tightest material in the entire AI supply chain. The gap between demand and capacity is getting worse, not better.

I think this is the most asymmetric layer on the map. Investors chase the transceiver companies and ignore who grows the substrates underneath them. But NVIDIA is writing checks worth billions in cash and warrants to lock up supply from this exact layer. First link in the chain, last to get attention, and the one that chokes everything above it if it breaks.

Tickers: $GLW, $AXTI, $IQE, $AIXA, $AMS

💡 CORE PHOTONIC DEVICES

This layer converts electricity into light and back. Without it, zero data moves through fiber. NVIDIA dropped $4 billion into two companies here this year just to secure production capacity, and both of them joined the S&P 500 within weeks of each other. That should tell you how fast this went from niche to essential.

The supply gap is not closing. The companies shipping next gen lasers at volume can be counted on one hand, and switching suppliers takes years of requalification. Order books stretch past twelve months. Every next generation GPU cluster consumes more of these components than the last, and no one can substitute them on short notice. I watch this layer more closely than any other.

Tickers: $IPGP, $COHR, $LITE, $LASR, $SIVE

🔌 COMPONENTS & MODULES

The companies here take raw lasers and detectors, package them into finished transceivers and modules, and ship them straight to hyperscalers. If the layers below are the engine, this is the vehicle that actually reaches the customer. Hyperscaler purchase orders land here. The revenue acceleration shows up here first.

What I like about this layer is that you can underwrite it today, not in two years. These are businesses with signed capacity commitments and product already moving. The consolidation angle matters too: larger photonics players have already started absorbing standalone module companies, and whoever remains independent gains pricing power as options thin out.

Tickers: $AAOI, $MTSI, $VIAV, $LPTH

⚙️ SYSTEMS & EQUIPMENT

No company above this layer can manufacture a single photonic component without the machines built here. One of these names holds 100% of the EUV lithography market with zero competitors. Others supply the bonding equipment for co packaged optics or the process control instruments used across the majority of advanced packaging lines. If photonics is the gold rush, this is the layer selling the picks.

My honest take: this is where the smart, patient capital parks. Equipment companies have pricing power and multi year order books that generate cash through full capex cycles. They attract holders who don't panic on the first pullback. The stocks don't run 1,000% overnight, but they compound while everything above them swings, and that tradeoff is worth more than most people give it credit for.

Tickers: $ASML, $BESI, $ASM, $LPKF, $MKSI

🔍 TEST, METROLOGY & YIELD

The most ignored layer on this map, and arguably the one with the cleanest business model. Every wafer, laser, and transceiver has to be tested and verified before it ships. As speeds climb and photonic devices get more complex, the testing challenge compounds fast. The industry is now constrained not only by what it can build but by what it can prove actually works.

Yield is money. Better defect detection means better margins for every company upstream, which is why foundries keep buying test equipment even when they slash budgets everywhere else. These are capital light businesses tied to every unit of production across the chain. Last check before product hits the customer, and one of the few layers where demand doesn't cycle down when the rest of semis softens.

Tickers: $CAMT, $FORM, $AEHR, $ONTO, $VIAV

🧠FINAL THOUGHTS

The NVIDIA capital concentration tells the whole story. One company wrote $4.5 billion in checks to three photonics suppliers in a single quarter. That is a company locking down the one input that could bottleneck its GPU deployments: the optical interconnect.

Returns across this sector have been historic over the past twelve months. But separate the revenue growers from the narrative trades. Some of these companies are printing real quarterly numbers that would impress in any sector. Others are carrying multi billion dollar market caps on sub $100 million in annual revenue. Same sector, wildly different risk.

Every generation of AI infrastructure from here forward needs more photonics. Not less. The copper to light transition inside data centers is early. Co packaged optics is barely in deployment, and 1.6T transceivers are ramping with 3.2T already on roadmaps. The chain locks together: stress on any single link reprices every link above it.

The photonics sector has run and people think they missed it.

They have not seen what is coming. The buildout is only just beginning.

Here is the simple reality. Every AI cluster on earth needs to move enormous amounts of data between chips at the speed of light.

As clusters scale from thousands of GPUs to hundreds of thousands the amount of optical connectivity required does not grow in a straight line. It explodes.

Goldman called optical networking the next mega trend in AI infrastructure with a $154 billion TAM by 2028. We are nowhere near the peak of this cycle. We are at the start of it.

These are my four favorite ways to play it.

$AAOI — The vertically integrated bottleneck play. They make their own lasers in-house while competitors wait in line for supply. Two to three hyperscalers told them they would buy every transceiver they can make. Revenue up 83% to a record $456 million with guidance over $1.1 billion for 2026. When you own the bottleneck input you win.

$CRDO — The margin monster. Just tripled revenue to $1.3 billion in a single year at 68% gross margins. Guided to over 80% growth next year with optical alone contributing more than $600 million. Analysts raising targets to $270 and $300. One of the fastest growing names in all of semis.

$LITE — Lumentum. The blue chip photonics giant. Decades of optical expertise and one of the primary suppliers of the laser and transceiver components that the entire industry depends on. The safest large cap way to own the buildout.

$COHR — Coherent. The diversified photonics powerhouse with exposure across datacom, telecom, and industrial lasers. A massive installed base and direct leverage to the 800G and 1.6T transceiver ramp that hyperscalers are scaling right now.

The market thinks the easy money is gone. The reality is the AI cluster buildout is still in its early innings and every one of these companies has an order book bigger than it has ever been.

The plumbing of AI is photonics. And the plumbing is just being laid.

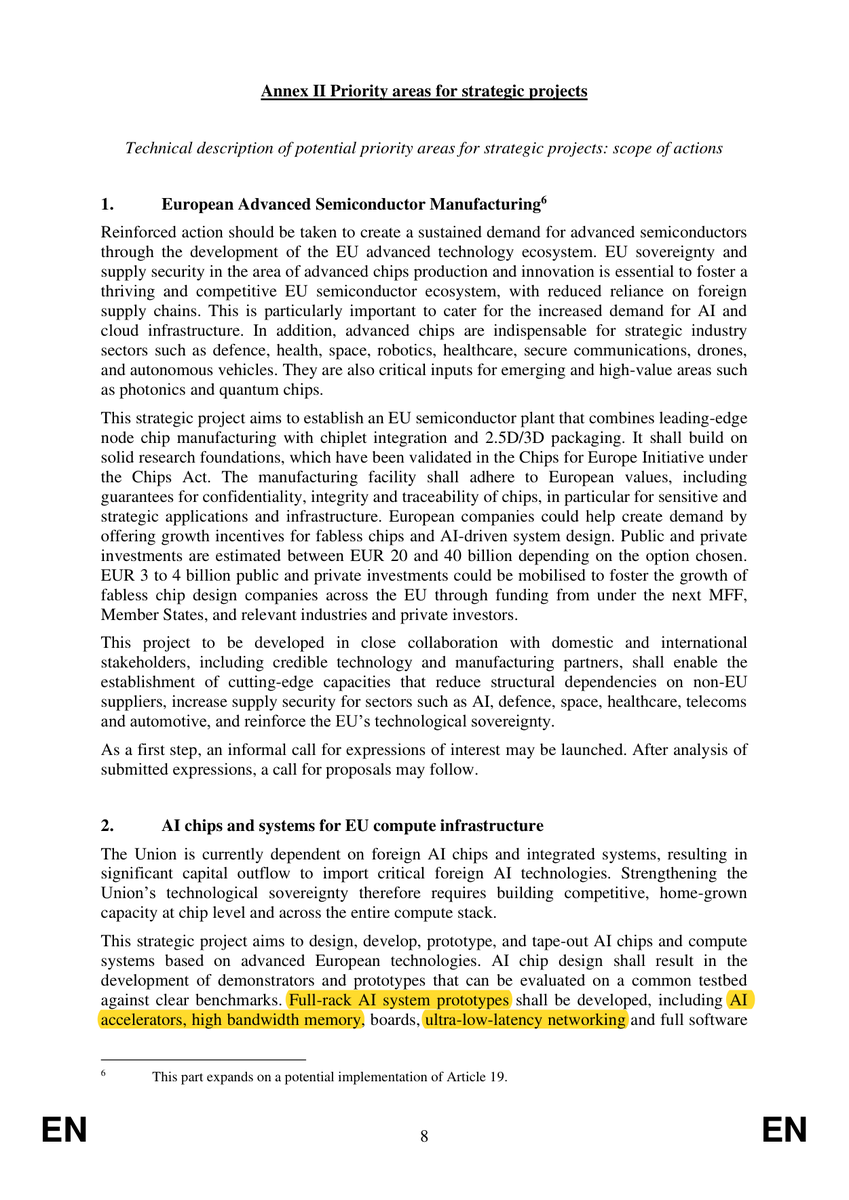

Europe doesn't want its own chip - it wants its own RACK.

The strategic plan calls for full-rack AI system prototypes: accelerators + high-bandwidth memory + boards + ultra-low-latency networking + full software stack, benchmarked on a neutral EU testbed.

That's the EU openly copying the Nvidia rack-scale model, where the unit of competition is the system, not the die.

Pair it with the separate €8–12B leading-edge design push (RISC-V, ASICs, AI accelerators) and the intent is clear: capture value in design + integration, not just fab.

$NVDA $AMD

Yeah… I think all your upstream semi supply chain companies are going much higher.

Goldman now expects a combined $5.3 trillion of capex spending for the four largest hyperscalers $GOOGL / $META / MSFT / $AMZN from 2025 to 2030.

Revised up from $4.5T from Q1 earnings.

“Aggregate capex est. $7.6 trillion between 2026 and 2031.”

And it flows upward to these tiny chokepoints like $SIVE for CPO lasers/ $SOI for Silicon Photonics substrates. Leaderdrive/Harmonic for Humanoids components.

And so on…

Ai names don’t move in a straight line up,

but is just the beginning of the next Industrial Revolution as we move from R&D/compute buildout into commercialization from Agents -> Physical AI -> discovery.

🦔Sam Altman says OpenAI's top internal user burns 100 billion tokens per month. Six years ago that number was 100,000. An external customer uses even more. Cost complaints are now the second most frequent issue he hears from clients. And his next move is "always on" AI that runs autonomously in the background, which would multiply consumption far beyond current levels. Altman shared this during a livestream on enterprise AI adoption covered by Axios.

My Take

Altman just described a future where consumption goes up by orders of magnitude while his customers are already asking how to bring the bill down. Those two things can't coexist for long. GitHub Copilot switched to token billing two days ago and users burned through a month of credits in hours. Ramp data already shows Anthropic passing OpenAI in enterprise spend, which means the competition for these customers is heating up at the exact moment the customers are pushing back on cost.

IBM's CEO said this week the industry needs $6 to $8 trillion in capex and the revenue to justify it probably doesn't exist. Altman is previewing autonomous agents that would multiply current token consumption without anyone requesting it. Either the cost per token drops fast enough to make that affordable, or enterprises start capping their AI spend. One customer already exceeds 100 billion tokens a month. Scale that across autonomous agents at every enterprise and nobody has budgeted for what comes next. Altman is selling a vision of infinite demand while admitting the customers paying for current demand are already flinching at the price.

Hedgie🤗

The EU has released hundreds upon hundreds of pages, a chunk of it tied to the Chips Act. Here's a summary by Claude. Next up I'll dig into the changes and key items that tie into stocks.

First, be precise: this is an update, not law yet. The Commission published it today, now Parliament and Council negotiate, with a final deal targeted for 2027. It's one of four pieces in the broader Tech Sovereignty Package.

The honest backdrop: the 2023 Chips Act set a 20% global market share target for 2030. The European Court of Auditors already called that out, the EU sat at 9.8% in 2022 and is projected to hit just 11.7% by 2030. The review got accelerated under pressure from a Dutch-led coalition. This is a mid-course correction, not a victory lap.

The core pivot is supply-side → demand-side. New tools: Grand Challenges for AI chips, Demand Accelerators (linking suppliers and users via offtake agreements), innovation procurement, EU-preference in public tenders. Logic is local demand pulls local supply.

Crisis powers got teeth. Per leaked drafts (FT, Reuters), once the Commission triggers a crisis stage it could force chipmakers to prioritize crisis-critical orders, overriding existing contracts, buy chips centrally for member states, and fine firms up to €300k for refusing to hand over information or giving misleading data. That's the part industry will fight.

Supply side: FOAK State aid now covers the whole chain, raw materials to packaging. New Strategic Projects for EU co-investment, a Semiconductor Region of Excellence label, permitting capped at 12 months. Flagship is the EU's first leading-edge + chiplet + 3D-packaging fab, pilot production targeted 2030–2033.

The catch, and it's the big one: the proposal itself carries only ~€70M plus staffing. The real money sits in the next EU budget (2028–2034) via the Competitiveness Fund, to be requested later. Industry wanted a dedicated semiconductor budget in the tens of billions. They got a framework, not a number.

TL;DR: the EU admits v1.0 built the lab not the fab, and is on track to miss its own target. 2.0 bets on demand-pull, emergency powers, and one flagship fab, but it's an early-stage text with negotiation ahead, leaning on funding that isn't committed yet.

$MRVL CEO Matt Murphy made the case at Computex that the copper wall is moving inside the rack, and CPO is the only way through.

At 200G per lane, copper is still sufficient. But Murphy stated that is the last generation where it will be. Beyond that, rack-scale connectivity requires optical, and the transition specifically requires CPO – the optics need to be co-packaged on the chip itself.

Murphy quantified it precisely: at 200 Gbps per lane, copper reach shrinks to about 2.5 meters. That pushes optics inside the rack. There is no alternative path.

Marvell also announced an expanded partnership with NVIDIA under NVLink Fusion. Murphy explicitly cited optical DSP, silicon photonics, and high-performance analog as the pillars of that collaboration.

Which is exactly where $SIVE sits – confirmed in the AyarLabs ecosystem, confirmed in the GlobalFoundries SCALE platform, and now confirmed as a direct node in the architecture Murphy is describing.

The last month has been rough for the photonics ecosystem. I told my subscribers weeks before Computex that this was coming. Price action does not move me. Technological advancement and forward projections do. This is a game market makers play before major catalysts, and it works every time on people who anchor to charts instead of thesis.

I hope the CPO bears are taking notes. This is one more data point in the 20-plus papers and projections I have shared over the past months on photonics and CPO.

Build your conviction on the architecture, not the price. Watch Murphy’s Computex keynote and build your own conviction.

Bullish AF photonics.

Bullish AF AI infrastructure.

$MRVL $TSEM $SIVE $AEHR $LITE $AAOI $SOI $IQE $COHR $TRT

Sam Altman said AI budgeting has recently become a "huge issue" for some companies, something that "never came up" earlier this year. https://t.co/P2zODBNmDp

J'ai publié tout à l'heure l'analyse complète du Chips Act 2.0. J'ai essayé également de traduire les mesures réglementaires en un score.

L'objectif : identifier quelles sociétés cotées européennes ont le plus d'alpha face à ce nouveau cadre réglementaire.

Le score est construit sur 6 critères directement tirés du texte de loi et pondérés selon leur impact sur les flux de commandes :

A. Demand-side (25%) : exposition aux mécanismes de création de demande (Demand Forum, Grand Challenges, procurement public souverain). C'est le pivot central du Chips Act 2.0.

B. CADA / AI Gigafactories (20%) : capacité à fournir le hardware des datacenters souverains et des AIGF (200 Mds EUR d'investissements, triplement de la capacité datacenter EU).

C. FOAK / Strategic Project (20%) : éligibilité au statut First-Of-A-Kind élargi à toute la chaîne de valeur (permitting accéléré à 12 mois, guichet unique).

D. IPCEI AST (15%) : positionnement sur les technologies couvertes par le 3e IPCEI semi-conducteurs (AI chips, photonique, packaging avancé, EDA).

E. Region of Excellence (10%) : ancrage physique dans les clusters semi EU labellisés (Dresde, Grenoble, Eindhoven, Leuven, Catane, Villach).

F. Photonique / Quantum (10%) : exposition aux deux ajouts structurels du Chips Act 2.0 (PIC comme 6e composante, pont vers le Quantum Act).

Chaque société est notée de 0 à 3 sur chaque critère. Score pondéré sur 18 points maximum.

le Top 20 est en image

Ce qui en ressort : les large caps (ASML, Infineon, STM) scorent haut grâce à l'infrastructure et aux clusters. Mais l'alpha asymétrique est dans les small/mid caps exposées simultanément au demand-side ET au CADA. Le marché price déjà les premières. Pas encore les secondes.

Je vous invite à consulter l'article si le détail vous intéresse.

⚠️ Analyse basée sur des documents réglementaires publics. Aucune recommandation d'achat ou de vente. Vous êtes seul maître à bord de vos investissements.

@laadred No, its because CHIPS ACT 2 was just published now and photonics was added.

"photonics and photonic integrated circuits to the reinforced Chips for Europe Initiative 2.0"

$XFAB is mentioned in some reports. The documents are too long still going through everything now.

Today a crazy quantum story just got wilder.

On March 31, the Google Quantum AI team published a landmark result on Shor's algorithm for elliptic curve cryptography. Technically, the paper was a bombshell: a dramatic 10x improvement over the state-of-the-art. As a stunt and wakeup call to the blockchain space, those optimisations were illustrated on secp256k1, the elliptic curve underlying Bitcoin and Ethereum signatures.

But perhaps the most striking part of the paper was sociological, not technical. Instead of following standard academic process, the optimisations were kept secret, hidden behind a zero-knowledge (ZK) proof. Google's accompanying blog post mentions they "engaged with the U.S. government". The ZK proof demonstrates the existence of algorithmic improvements without leaking details. Academic censorship with ZK, a historic first!

As a co-author of the Google paper I witnessed some of the context surrounding this censorship. To be honest, multiple aspects of that context don't sit well with me. As much as I believe the general public ought to know more, I am limited in my ability to whistleblow. Though let me be clear about one thing: the Google team's professionalism has been absolutely exemplary, and they deserve nothing but praise.

Censorship has a way of backfiring. The Streisand effect, where an attempt to bury something only draws more attention to it, is exactly what's unfolding today. First, Google's key optimisation has been rediscovered by the French. And in a thrilling turn of events, a collaborative Shor-at-home challenge just launched. The initiative, available at ecdsa[.]fail, breached a new Shor world record in a matter of hours.

Let's start with the rediscovery. Just two months after Google's paper, French quantum expert André Schrottenloher cracks the main secret optimisation. His paper, titled "Optimized Point Addition Circuits for Elliptic Curve Discrete Logarithms", landed on the arXiv today. Big congrats to André, who beat several other nerdsnipped experts to it. In a blog post also published today, Craig Gidney, the world expert on Shor optimisations, revealed that he'd been sitting on this very optimisation for a whole year under censorship pressure.

Interestingly, André missed a handful of minor optimisations, both from Google's original publication and from improvements found since. It's plausible there's still plenty of juice left to squeeze out of Shor, and this is exactly what the ecdsa[.]fail challenge is about. The verifier program developed for the ZK proof does double duty, automatically filtering for valid submissions. Dozens of compounding small and micro improvements are rolling in. As of the time of writing there's an 8.4% improvement to Google's circuit, as measured by the product of logical qubit count and Toffoli gate count. Nice!

The nerdsnipping ran deeper than anyone expected. Over the last few weeks it became clear it extended well beyond André and other quantum experts. Behind the scenes, a small army of amateurs quietly got to work. Inspired by Karpathy-style autoresearch, they turned AI on Shor. Ironically, the verifier program for the ZK proof makes an ideal reward function for AIs. The barrier to entry for this modern style of research is refreshingly low, with several non-experts, even a teenager, finding nice optimisations. Get in touch if you'd like to join a Telegram group with fellow autoresearchers :)

Part 2: neutral atoms and qday

The story doesn't end with Google. On the same day Google went public, a stealthy startup called Oratomic published its own Shor paper in a coordinated release. It made a splash, ultimately becoming the most upvoted paper on scirate[.]com, a website ranking arXiv papers.

Oratomic's claim was wild. By building on Google's logical optimisations and applying custom physical optimisations for neutral atoms, they claimed just 10K physical qubits were sufficient to run Shor's algorithm on secp256k1. That number is mind-bogglingly low.

Knowing essentially nothing about neutral atoms when Oratomic's paper landed, I was intrigued and decided to learn more about the tech. I fell straight down the rabbit hole and spent a couple hundred hours on the topic. I got a little obsessed and watched every YouTube video I could find and spoke to a bunch of experts.

My conclusion? The tech is real, very real. Even Google recently decided to start a neutral atom lab, a notable pivot from their sole focus on superconducting qubits. If you care about qday, i.e. the day a quantum computer will break the first piece of cryptography in production, neutral atoms demand your attention. I shared some of my learnings on Shor and neutral atoms in a 30min talk at the ZKProof cryptography conference. You can find it on YouTube by searching "zkproof neutral atom".

Here's an interesting observation about this duo of breakthrough papers: neither Google nor Oratomic say a word about what their results mean for qday. No timelines. Zero. Nada. That is especially baffling given that the whole point of whitehat quantum cryptanalysis is to inform qday estimations and help the general public make good decisions.

So let me attempt to partially fill the silence, similarly to what Scott Aaronson did in his April 29 post. Given everything I know, including scary non-public information, I now put the odds of qday by 2032 at 50%. 10% by 2030.

Anecdotally, the US government has its own date: 2035. Originating at the NSA and later adopted by NIST, it's when branches of the US government will be disallowed from using quantum-vulnerable cryptography. In plain language: with hindsight, that date is a joke and should be discounted entirely. I don't see how NIST avoids being forced to pull it forward by years.

Part 3: post-quantum cryptography

There are good reasons to sound the alarm today, but please do not panic. Rushing carelessly towards immature post-quantum cryptography is a recipe for disaster. IMO a good target date for migration is 2029, roughly 3.5 years out. 2029 happens to be the date selected by Google, Cloudflare, and the Ethereum Foundation.

These days most of my time goes to safely migrating Ethereum towards post-quantum cryptography as part of the broader lean Ethereum effort. There's a lot to do. We need to rip out and replace BLS signatures at the consensus layer, KZG commitments at the data layer, and ECDSA signatures at the execution layer.

The plan to get there is compelling, and is based on hash-based cryptography. Within the Ethereum Foundation we've developed a Swiss army knife called leanVM (github[.]com/leanEthereum/leanVM) powered by the magic of hash-based SNARKs. Thanks to truly exceptional work by Emile, Thomas, and others, its performance is derisked. Regarding security, leanVM is a jewel, a minimal zkVM crafted for end-to-end formal verification and maximum security.

Want to help? There are two $1M initiatives. First, the Proximity Prize (proximityprize[.]org). Solve a long-standing mathematical conjecture in coding theory, improve hash-based SNARKs, and go home a millionaire. Second, the Poseidon Initiative (poseidon-initiative[.]info), offers $1M for breaking Poseidon, the SNARK-friendly hash function.

In the last 6 months at @Ahrefs, we analyzed over 1 billion data points across 14 studies. Here's what we learned about AI search optimization:

1) "Best X" blog listicles are the single most prominent content format cited by AI chatbots. They make up 43.8% of all page types cited by ChatGPT specifically.

2) 67% of ChatGPT's top 1,000 citations come from sources marketers can't influence: Wikipedia (29.7%), homepages (23.8%), app stores (6.6%). Only 32.3% are influenceable content like educational pages, reviews, news, and blog posts.

3) 28.3% of ChatGPT's most-cited pages have zero Google organic visibility. These pages get cited repeatedly by ChatGPT despite not ranking in Google at all. A completely separate discovery layer.

4) ChatGPT only cites about 50% of the URLs it retrieves. It fetches dozens of pages per query but uses half as background context without attribution. This means that being retrieved and being cited are very different things.

5) Adding schema markup had zero meaningful impact on AI citations. AI Overviews actually dipped −4.6%, while AI Mode (+2.4%) and ChatGPT (+2.2%) showed changes indistinguishable from zero.

6) YouTube mentions have the highest correlation (0.737) with AI brand visibility out of all the factors we studied (including all the conventional SEO metrics like backlinks, page count, DR, etc). This held true for both Google-owned and OpenAI products.

7) AI Overviews reduce clicks to the #1 result by 58%. That’s up from 34.5% just 10 months earlier. The trend is accelerating.

8) 99.9% of AI Overviews appear on informational intent queries. Transactional, navigational, and local searches are almost entirely AIO-free. Shopping triggers AIOs just 3.2% of the time.

9) For a given search query, Google’s AI Mode and AI Overviews reach the same conclusions 86% of the time — but cite almost entirely different sources (only 13.7% citation overlap).

10) AI Overviews change every 2.15 days on average, with 70% of content differing between consecutive observations. But semantic similarity stays at 0.95. The words, sources, and entities constantly shuffle, but the actual meaning barely moves.

Optical interconnect names are running because $NVDA CEO Jensen Huang basically validated the future AI architecture where copper wins inside the rack but optics becomes unavoidable as AI clusters scale across full data centers.

Thats why optical components, transceivers, DSPs, silicon photonics & testing names are getting re-rated today:

• $MRVL +30%

• $AEHR +21%

• $COHR +16%

• $LITE +12%

• $VIAV +11%

• $AAOI +10%

• $CRDO -1% (due to earnings)