Love art, tech & science. Quality inputs and here to learn having been in digital assets since 2017. Mistakes, I've made a few but learnt a great deal.

@Stellar_Rippler The years that Ripple had to endure the SEC and Warren antagonism has set them back such that others have been able to accomplish financial gains which would not have otherwise been achieved

@mrnguyen007 Hopefully my explanation helps curb expectations and set full understanding.

The bill is NOT set for floor vote. The General Orders folder is nothing more than an eligibility to consider for the floor. This screenshot should help support what I have said:

Today we go live on mainnet with the Fusion Rollup, the world's first multi-ledger rollup, connecting 74 blockchain networks in one unified environment, built for institutions.

When I started @quantnetwork in 2015, the vision was simple: make blockchain work for institutions at scale across any network, without the complexity and fragmentation that's held the industry back.

For years, institutions had two bad options: bet everything on a single chain, or stitch together insecure bridges across many. Fusion refuses that trade-off. It connects to many networks at once, moving assets, settling transactions, and messaging across chains as built-in capabilities, not workarounds.

The breakthrough is unified assets. A example of a stablecoin like USDC or tokenised fund like BUIDL or any other digital assetspread across 7 chains collapses into one: uUSDC or uBUIDL. One asset, one liquidity pool, instead of 7 copies and 7 fragmented pools. Each stays anchored to its origin chain and is withdrawable anytime. No custody or compliance trade-offs.

This isn't another layer 2 or a blockchain. It's a new category of infrastructure and it's live.

Read more on: https://t.co/MGfs1FgA6T

→ https://t.co/OQBfu2CEZb

→ https://t.co/4o9nnaA7zc

#QuantFusion #EnterpriseBlockchain #MultiLedgerRolleUp #FusionRollup

Love your posts, but all that matters to me is that we keep moving forward with regulations globally and that the governments, with the financial institutions, begin to use this fintech. Been in crypto since 2017 and have never been so excited about the next few years. I'm not sure that the charts can reflect this in total as we are still so early and so much growth to come

🧿💥 $QNT Fidelity International just launched FILQ, their first fully tokenized fund.

To settle in sterling with UK institutions, they’ll need a proper digital cash leg. That infrastructure is being built right now.

1/3 🧵 👇

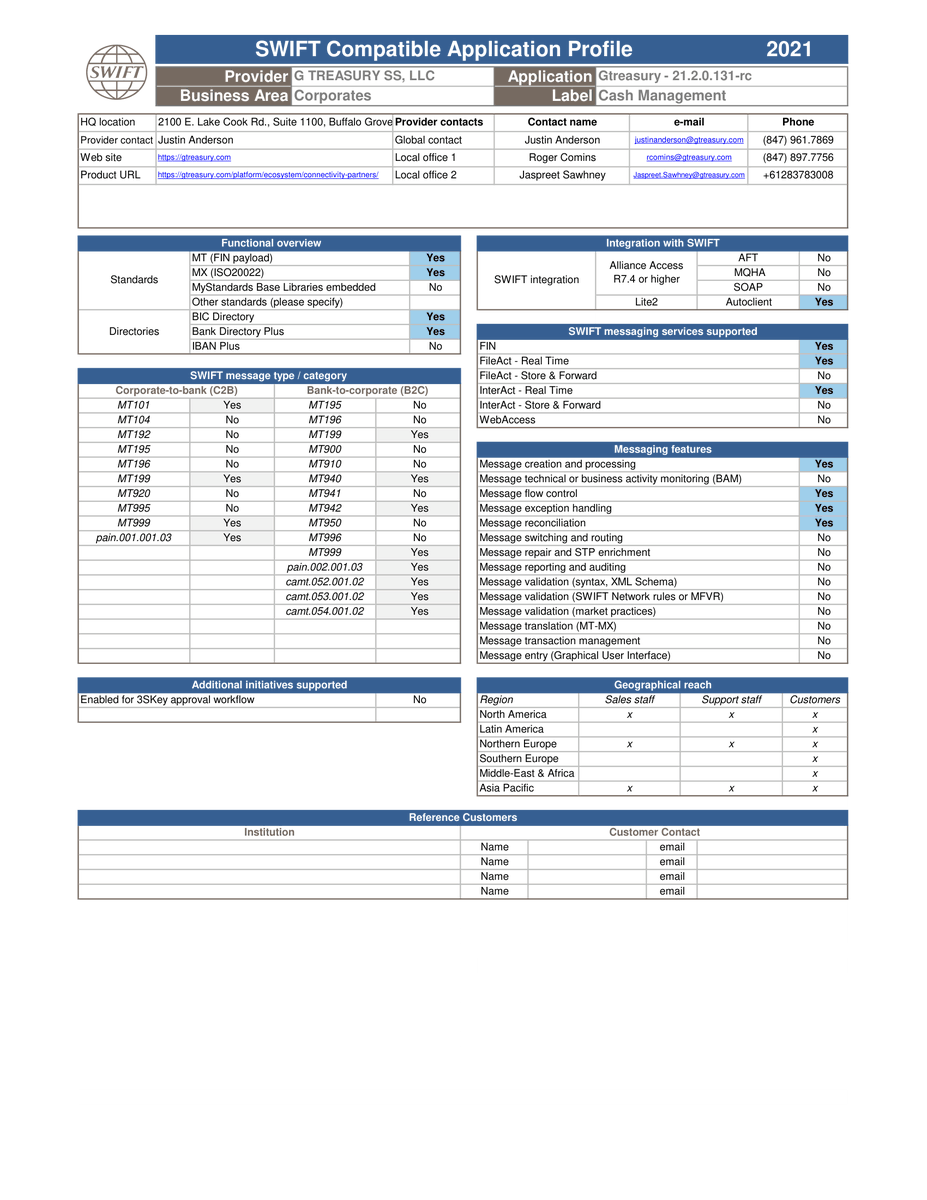

🚨 KNOW: A Quiet 2021 SWIFT Document Just Revealed The Deepest #Ripple Connection Most People Never Knew Existed.

• What This Document Is

This is an official SWIFT Compatible Application Profile from 2021.

It certifies that GTreasury was a fully integrated SWIFT-compatible application provider — three years BEFORE Ripple acquired it for $1,000,000,000 in October 2025.

• Why This Changes Everything

#Ripple Treasury (the rebranded GTreasury) inherited this SWIFT certification on Day 1 of the acquisition.

That means Ripple Treasury is officially SWIFT-integrated.

Not through a partner.

Not indirectly.

Directly.

• What The Document Confirms

GTreasury was certified to operate across every major SWIFT integration layer in 2021:

▪️ SWIFT Standards Supported

• MT (FIN payload): Yes

• MX (ISO 20022): Yes

• BIC Directory: Yes

• Bank Directory Plus: Yes

▪️ SWIFT Integration

• Alliance Access R7.4 or higher: Yes

• Lite2: Yes

• Autoclient: Yes

▪️ SWIFT Messaging Services

• FIN: Yes

• FileAct Real Time: Yes

• InterAct Real Time: Yes

▪️ SWIFT Message Types Supported

▪️ Corporate-to-Bank:

• MT101

• MT199

• MT999

• pain.001.001.03

▪️Bank-to-Corporate:

• MT199

• MT940

• MT942

• MT999

• pain.002.001.03

• camt.052.001.02

• camt.053.001.02

• camt.054.001.02

Translation In Plain Language

GTreasury could already:

• Send SWIFT messages

• Receive SWIFT messages

• Validate payment flows

• Reconcile banking data

• Operate across the global financial messaging network

Including ISO 20022 — the new global payment standard SWIFT is migrating toward.

• The Geographic Reach Already Built

In 2021, GTreasury already had SWIFT-certified operations across:

• North America

• Latin America

• Northern Europe

• Southern Europe

• Middle East & Africa

• Asia Pacific

That is a global SWIFT footprint covering nearly every major payment corridor in the world.

• Why This Matters For ripple:native

When Ripple acquired GTreasury for $1,000,000,000, they didn’t just buy a treasury platform.

They bought:

• A SWIFT Certified Application

• SWIFT Alliance Access integration

• SWIFT FIN messaging integration

• SWIFT Lite2 integration

• ISO 20022 readiness

• Multi-corridor global infrastructure

• Connections to 13,000+ banks worldwide

And now they layer:

• #Ripple infrastructure

• RLUSD

• The XRP Ledger

directly on top of it.

• The Hidden Architecture

Stop and think about what this actually means.

Ripple Treasury is now potentially the only platform combining:

• Native SWIFT messaging

• ISO 20022 compliance

• XRP Ledger settlement

• RLUSD stablecoin settlement

• Goldman Sachs Mosaic integration

• Connections to 13,000+ banks

inside one treasury environment.

A corporate CFO could theoretically initiate a payment through SWIFT messaging rails while settlement occurs on blockchain infrastructure like the ripple:native Ledger using RLUSD.

Without changing existing banking infrastructure.

• The Bigger Picture

People kept asking how #Ripple would bridge SWIFT and the ripple:native Ledger.

The answer may have been sitting inside a 2021 SWIFT certification document the entire time.

Ripple didn’t necessarily have to build a bridge.

They bought one.

• The Bottom Line

While crypto Twitter argues about Ripple vs SWIFT, public infrastructure documents suggest something far more strategic may be happening.

Ripple is not trying to replace banking infrastructure overnight.

It appears to be integrating directly into it.

Quietly.

Strategically.

Through infrastructure that was already certified years before the acquisition.

The infrastructure connecting blockchain settlement to global banking rails may already exist.

And it may have existed long before most people noticed.

The dominoes keep falling.

One quiet document at a time.

Follow @RippleXity for the deep links nobody else is connecting in the ripple:native ecosystem.

@InvestWithD We will soon find out what is more important to Trump - making billions for his family or ensuring that the USA is at the forefront of this new technology?

Visa 💣 Mastercard💥☠️

❤️ XRP ❤️

In January 2026 two of the most powerful executives in the world sat down with investors.

Visa. Mastercard.

The question was simple.

Are stablecoins a threat?

The answer was confident.

"Little current product-market fit for stablecoins in everyday payments."

"Most crypto is trading and speculation."

"Not a near-term threat."

Wall Street nodded.

Everyone went back to their desks.

Somewhere in Omaha an 95-year-old man was reading the same transcript.

He'd held Visa since 2011.

Mastercard since 2011.

Fifteen years. Bought at $40. Watched them go up 2,000%.

He didn't sell when crypto appeared.

He didn't sell during COVID.

He didn't sell when Bitcoin ETFs launched.

He held. Because Visa and Mastercard had a moat.

86% of all US card transactions.

4.7 billion active cards.

130 million merchants.

You can't disrupt that overnight.

Or so everyone thought.

February 2026.

A research note landed on institutional desks.

AI agents — autonomous programs making purchases on behalf of humans — are optimized for one thing.

Cost minimization.

Visa and Mastercard charge 2-3% on every transaction.

The note was direct.

AI agents will systematically route around them.

Not because they hate them.

Because they're programmed to find the cheapest path.

And the cheapest path costs fractions of a cent.

March 2026.

Mastercard spent $1.8 billion.

Largest stablecoin acquisition in history.

The rails they said weren't a threat six weeks earlier.

$1.8 billion says otherwise.

Q1 2026.

Berkshire Hathaway filed their 13F.

No press release. No explanation.

Visa — Sold. 100%. Gone.

Mastercard — Sold. 100%. Gone.

Fifteen years. Two thousand percent return.

Sold both.

Completely.

Same quarter the executives said nothing to worry about.

Buffett doesn't invest in products.

He invests in moats.

When Mastercard spends $1.8 billion trying to rebuild on stablecoin rails —

The moat is already gone.

He saw it. He just didn't make a speech.

He filed a document.

May 6 2026.

Mastercard's network routed an instruction.

Ripple settled the transaction on the XRP Ledger.

Under 5 seconds. Fraction of a cent.

The new pipe processed its first institutional Treasury settlement.

While the old pipe was being sold by the greatest investor alive.

The AI agents don't care about brand loyalty.

They care about one number.

Cost per transaction.

Fractions of a cent beats 2-3% every single time.

The executives said stablecoins weren't a threat.

Then spent $1.8 billion on stablecoin infrastructure.

The greatest investor alive said nothing.

Just filed a document.

And walked away from 15 years and 2,000% returns.

When the smartest money in the world moves quietly —

Pay attention to where it's going.

And pay very close attention to where it's leaving.

🛡️ ISO Ledger

🚨 KNOW: Why #Ripple Just Quietly Built An Alternative To State Street For The Crypto Era.

Let @RippleXity break it down for you 👇

★ What's Happening

State Street is one of the world's largest custodians, managing $46 trillion in assets. Alongside JPMorgan, Citigroup, and BNY, it forms the backbone of traditional asset custody.

In Ripple's own institutional materials, #Ripple acknowledges that traditional custody has been dominated by these legacy players.

Now Ripple is building the digital asset version of that infrastructure.

★ What Ripple Has Built

➥ #Ripple Custody — bank-grade digital asset custody for institutions

➥ Acquired Palisade — wallet-as-a-service infrastructure (Nov 2025)

➥ Acquired Standard Custody & Trust (NYDFS Trust Charter holder)

➥ Acquired Metaco — institutional custody pioneer (acquired for $250M)

➥ Partnered with Securosys — for hardware security modules (HSMs)

➥ Partnered with Figment — for institutional staking

➥ Partnered with Chainalysis — for compliance and transaction screening

➥ Partnered with IBM Cloud — for highest-grade security infrastructure

➥ Partnered with Kyobo Life Insurance — for institutional digital custody and on-chain settlement

★ Why This Matters

State Street and BNY built their dominance over centuries holding stocks, bonds, gold, and cash.

#Ripple Custody is being built right now to do exactly that — but for digital assets, tokenized real estate, stablecoins, and on-chain securities.

★ The Bigger Picture

When tokenized assets hit $16 trillion by 2030, every institution will need a custodian.

State Street, JPMorgan, BNY are scrambling to enter the digital asset space.

#Ripple already has the infrastructure live, regulated, and operational — including the BNY partnership for $RLUSD reserves.

★ The Bottom Line

While the legacy giants are catching up to crypto custody, Ripple is already building the digital version of State Street.

The custodial backbone of the future on-chain economy is being constructed in real time.

The dominoes keep falling. Custody is just the next layer.

Follow @RippleXity for the deep links nobody else is connecting in the ripple:native ecosystem.

🚨 Clearing your cookies does nothing.

That is not how they track you anymore.

Texas A&M and Johns Hopkins just published the first peer-reviewed proof.

It is called browser fingerprinting.

Here is what they found and what actually stops it:

🚨NEW: UK FCA OFFICIALLY PUBLISHES New Cryptoasset Guidance — Trading, Custody & Stablecoins Under FULL REGULATION FROM 2027 🤯🇬🇧🔥

The UK’s Financial Conduct Authority (FCA) has now officially PUBLISHED its Cryptoasset Perimeter Guidance (CP26/13) — clearly defining WHICH crypto activities REQUIRE authorization to operate legally in the UK. 👀

The guidance draws a clear line around WHAT CRYPTO FIRMS will need FCA authorization for if they want to operate legally in the UK. ✅

The guidance does NOT focus on just one sector — it covers the ENTIRE crypto stack, including trading platforms, custody providers, stablecoins, and staking services. 😳🔥

👉 Crypto exchanges will REQUIRE FCA authorization

👉 Custody & safeguarding of assets becomes REGULATED

👉 Stablecoin issuance falls under STRICT oversight

👉 Staking and deal-making activities are INCLUDED

The FCA says firms have until June 3, 2026 to submit feedback before the FINAL guidance is published. 📅

More updates coming.

Elon Musk just told the world Universal High Income is coming. Part 2

Let's break it down.

Not Universal Basic Income. Universal "High" Income.

The vision sounds generous. AI takes the jobs. Government sends the checks. Nobody goes hungry. But before you celebrate —

ask yourself, how will I receive this money?

What form does that check arrive in?

It won't be cash. They won't call it a CBDC — that word carries too much political weight now. They'll call it a digital wallet. A smart dollar. A government payment account.

But every major stablecoin already has the architecture built in.

Traceable.

Every transaction on a public ledger.

Freezable.

No court order needed.

Expiration dates.

Cornell professor Eswar Prasad confirmed at the World Economic Forum that programmable money can be coded to expire if unspent — forcing consumption, eliminating saving.

The Bank of Russia's deputy governor already gave a real world preview: "Imagine giving your kids money in digital rubles and restricting their use for the purchase of junk food."

That wasn't a warning. That was a feature announcement.

Now connect it to the infrastructure already being built around you.

16 cities worldwide have already implemented 15-minute city concepts. Paris. Milan. Barcelona. Madrid. Edinburgh. Sweden is testing it nationally with a target of every street by 2030.

Pair programmable money with 15-minute zones and the architecture changes entirely. Your digital wallet knows where you are. It knows what you bought. It knows how far you traveled. Carbon taxes get enforced automatically — not as a fine you pay later. As a transaction that simply gets taken from your account.

It gets more personal than geography.

Your medical records are moving to AI-managed systems right now. You have diabetes. Your doctor said no sugar. You tap your wallet at checkout to buy a piece of cake.

Transaction declined.

The AI doesn't make exceptions. It doesn't care about your birthday. And it doesn't need to violate any privacy HIPPA laws — because when your medical data and payment data run on the same government-managed system, it doesn't share your records. It just runs the logic.

Another example. Your account gets flagged for a terms of service violation. Your wallet is quietly restricted from purchasing airline tickets. No court. No hearing. The transaction just fails.

This is where XRP is different.

XRP — the native asset of the XRP Ledger — has no issuer. No central authority controls it. No government can freeze it. No algorithm can program it to expire. Once a transaction settles it is final and irreversible in 3-5 seconds.

To be precise: the XRPL does have a clawback feature — but it applies only to issued tokens, not to XRP itself. XRP cannot be clawed back. There is no entity to subpoena.

No expiration date.

No spending restriction.

No government can decide you bought the wrong thing with it.

The system being built around you needs you inside it to function.

Your XRP sits outside it.

When XRP eventually goes to 10$ and your at a 7x and its time to turn that XRP into fiat so you can take that vacation to Hawaii, and the institutions on the other side are buying it all up just ask yourself....

Was it worth it?