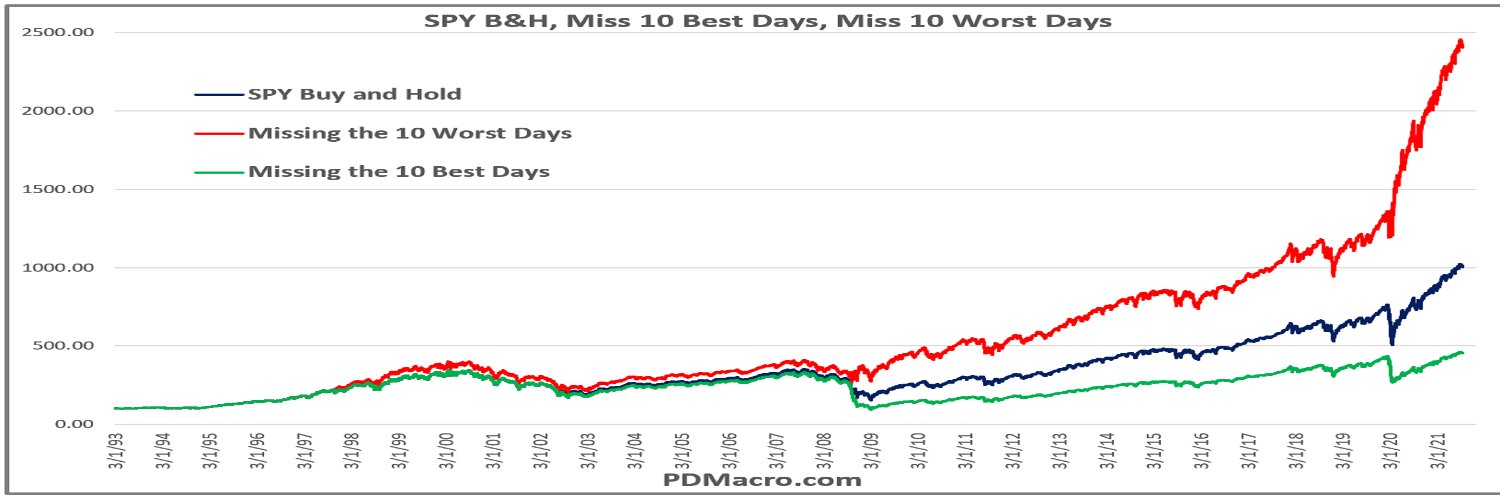

The Shit Returns Coming on All This AI Capex

AI revenues have finally overtaken depreciation, a very low bar. Getting even a decent return on all the capex planned requires the recent 100% revenue growth rate to accelerate over the next 5 years.

https://t.co/bifKj6KlvA

I suspect that gold’s correlated behavior will be temporary as gold has fallen out of favor after it went vertical last year. The fast money used to be in Bitcoin, and then it left for gold, and now it’s chasing semiconductors. The chart below shows how gold’s real rate model fell apart in 2022 when gold became a proxy for global liquidity. With global M2 now slowing from a growth rate of 12% at the peak to 7%, gold is understandably weaker. But it’s too weak considering the modest deceleration in M2.

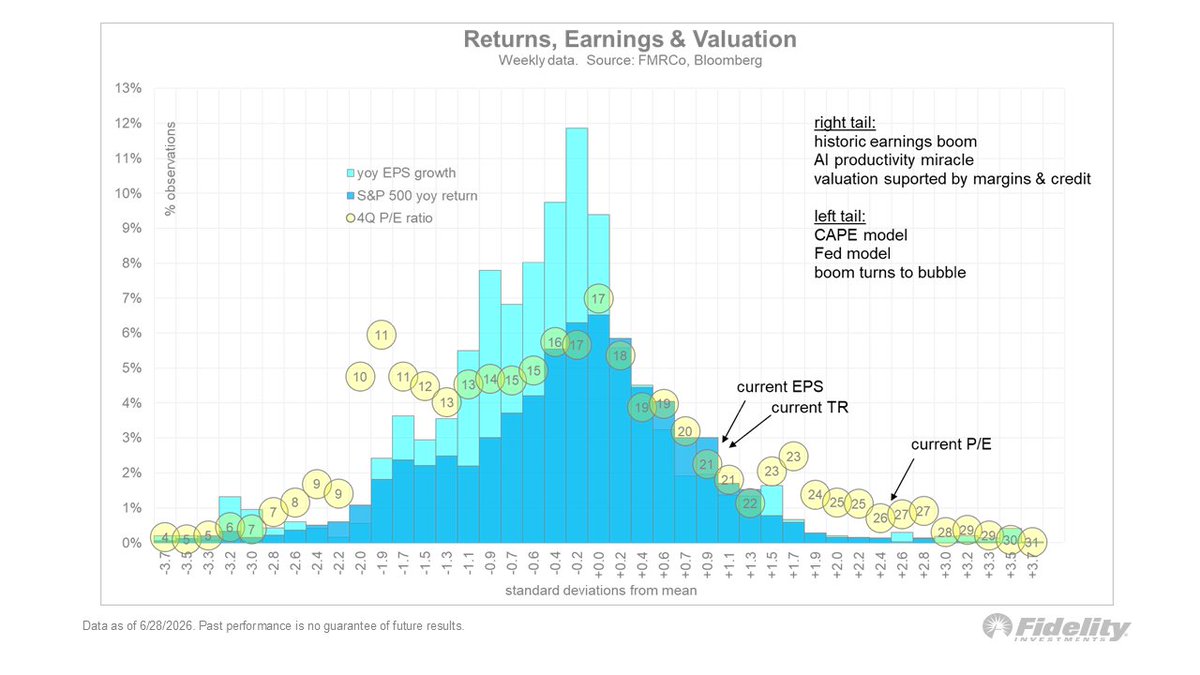

Thinking about the markets in a holistic sense, it’s clear that today’s landscape has tails on both sides. The chart below shows the distribution for the trailing P/E ratio, earnings growth, and the S&P 500 annual return. We are at or near the tail on all counts. 🧵(1/2)

The S&P 500 was down 2% last week (thank you Mag 7), but under the surface it was quite strong.

More stocks above 20-day, 50-day, and 200-day MAs than at the start of the week.

In fact, 65% of the components are above their 200-day MA, which is the most since early March.