The golden handcuffs in the housing industry might finally break. 🌟

Yesterday the HUD floated offering portable mortgages💸

A portable mortgage allows a borrower to transfer their existing loan and interest rate to a new property when they move, instead of taking out a new loan. This is a beneficial option when interest rates have increased since the original mortgage was secured, as it helps avoid prepayment charges and allows the borrower to keep their lower rate.

•The borrower sells their current home and purchases a new one, moving their existing mortgage to the new property.

•The borrower typically keeps the same interest rate and loan term from their original mortgage.

•If the new home requires a larger loan, the borrower may need to apply for a second mortgage or a new segment of credit to cover the difference.

This would be huge for move up home buyers and also home builders! 🏠

Did you know that there are 56 million mortgages in the United States?

Currently somewhere between 20.4% and 23.5% of those mortgages are under 3%. That is over 11 million people.

There are another 52.5% to 55.2% that have mortgages under 4%. That's over 29 million people.

Many of these people want to move but feel stuck because of their low rate. To spend over 2% more on a rate is hard for them to swallow even when they could be selling off their home and capturing huge equity.

There is no downside to this.

It allows the market to become more fluid.

It will increase listings, open up new inventory as well as encourage older clients to finally sell off and downsize or move to a condo thereby helping more first time buyers.

What do you think of this proposal?

"While there are clearly broader macro concerns worth debating, the mortgage policy elements of this package are, on balance, clearly constructive," said Isaac Boltansky, managing director and head of public policy at Pennymac.

https://t.co/R49L4nMH5p

Comentario poco popular

Partidos políticos son casi irrelevantes porque la maquinaria económica en la que vivimos funciona a-políticamente.

Requiere de más liquidez vía deuda/crédito para funcionar

Políticos pueden traer cambios marginales pero máquina funciona de una sola manera

Expect some mortgage rate relief in 2024! Our forecast shows rates beginning to move lower by year's end. Get the full forecast: https://t.co/oQpAnvCCZZ

Today, FHFA announced that it has rescinded the upfront fees based on certain borrowers’ debt-to-income ratio for loans acquired by @FannieMae and @FreddieMac. FHFA will also issue a Request for Input on the Enterprises’ pricing framework.

Read more: https://t.co/BKsSLWKsRN

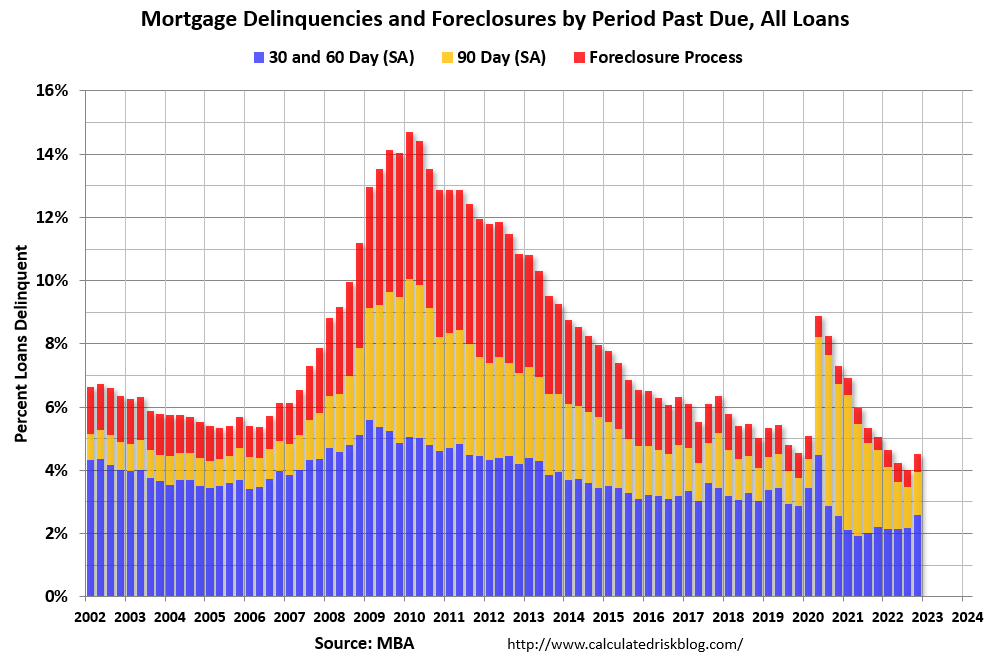

Fannie "Real Estate Owned" inventory increased in Q4; Expected to increase further in 2023 https://t.co/Arh5hyC75w

Still very low ... no foreclosure wave coming.

@fenderjazz1978 Early Payment Defaults tend to be the leading indicator, but I don't have a recent graph of EPDs. But here is a graph of delinquencies based on the MBA data (next best): https://t.co/cL3zzfriPz

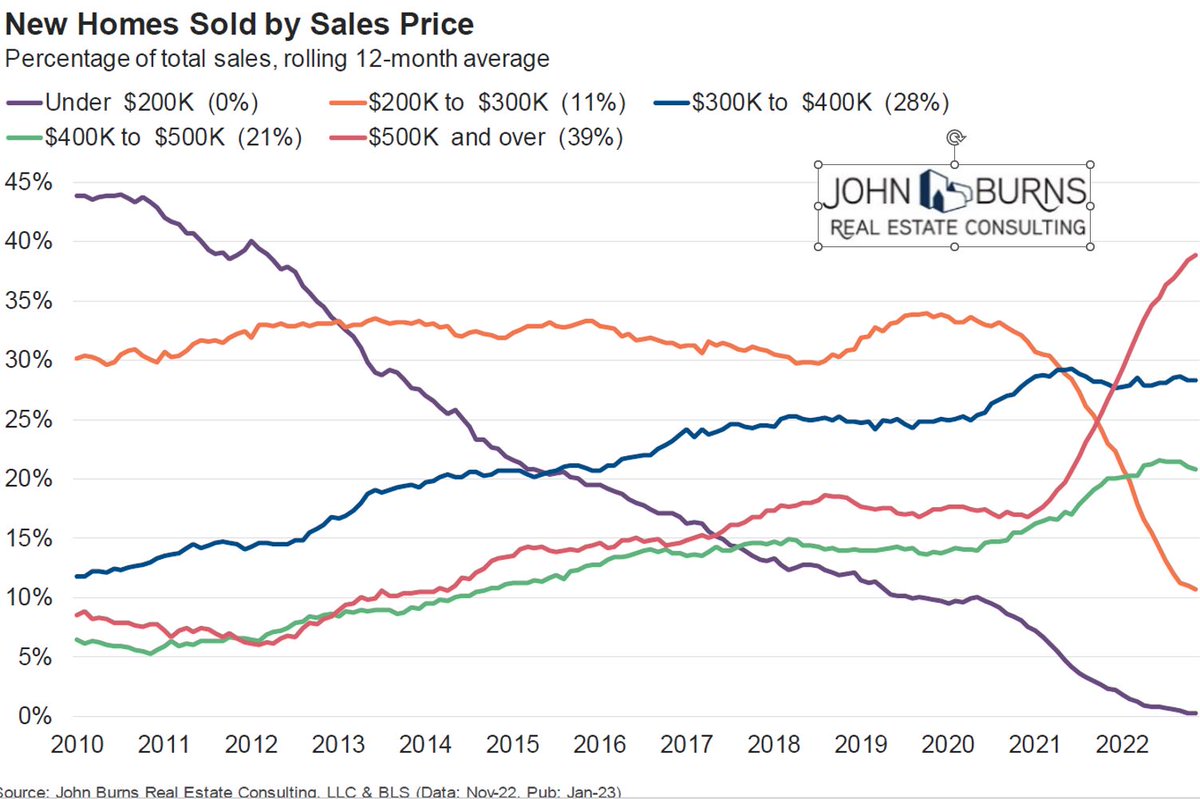

New homes priced below $200K are now 0% of the market.

They were 40% of the market one decade ago.

$500K+ homes have grown from 17% of the market to 38% of the market during Covid.

Expect both of these trends to reverse this year.

Today, HUD announced a proposed rule to fulfill the promise of the 1968 Fair Housing Act mandate to affirmatively further fair housing (AFFH).

This proposed rule would create places of opportunity where every resident can thrive.

The Housing Market Has Started To Recover: The housing market has begun to recover after hitting a low point in the second week of November. We’re not out of the woods yet, but homebuyers are coming off the sidelines.

https://t.co/gItXnJOYsR