Zircuit Finance is now live.

Institutional-grade yield. Transparent structure. Security-first design.

Targeting 8–11% APR with no deposit minimums and 0% management fee.

🚨 There’s a large-scale supply chain attack in progress: the NPM account of a reputable developer has been compromised. The affected packages have already been downloaded over 1 billion times, meaning the entire JavaScript ecosystem may be at risk.

The malicious payload works by silently swapping crypto addresses on the fly to steal funds.

If you use a hardware wallet, pay attention to every transaction before signing and you're safe.

If you don’t use a hardware wallet, refrain from making any on-chain transactions for now.

It’s still unclear whether the attacker is also stealing seeds from software wallets directly at this stage.

Excellent report here: https://t.co/5CtiZJHYsN

A new chapter begins… 🦬🦄

ETHDenver 2026 is officially on the horizon…

🫡 Captain Ethereum and the Rise of New BUIDL City

New venue. New vibes. New era. Whether you’re a 10-year Ethereum OG, an 8-year ETHDenver veteran, or new to the ecosystem, we look forward to BUIDLing the decentralized future together.

ETHDenver has somETHing for everyone.

New BUIDL City awaits 🧵👇🏼

Key points from Chairman Paul Atkins’ remarks today at “DeFi and the American Spirit,” SEC’s Crypto Task Force Roundtable on Decentralized Finance – a 🧵

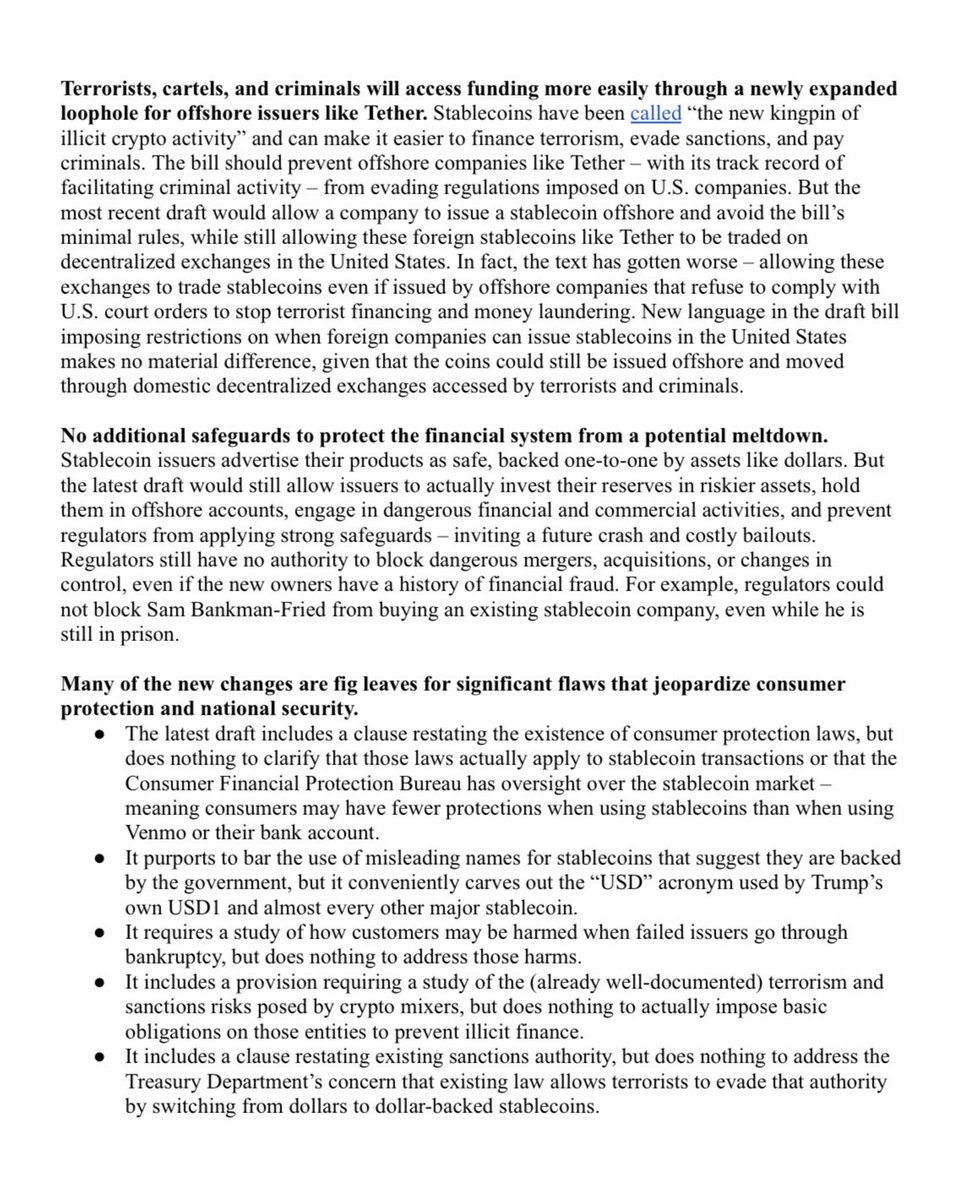

🚨NEW: Senate Banking Committee Democrats just dropped a scathing staff analysis of the latest GENIUS Act draft ahead of this evening’s cloture vote.

Staffers describe the latest GENIUS Act draft as a blueprint for ‘Trump crypto corruption’ and Big Tech dominance over digital currencies, urging additional changes to address unresolved issues.

The concerns they cite:

📌 No ban on Trump profiting from his own stablecoin

📌 Lets Elon Musk’s X create “X Money”

📌 Expands loopholes for Tether, aiding terrorists/criminals

📌 No real consumer protections or financial safeguards

The Senate is voting on stablecoin legislation today.

SWC will be scoring this vote as a KEY VOTE.

Tell your senator to stand with the over 52 million crypto owners in the USA - click here: https://t.co/VXGm7i8Ezx

Back in DC with @coinbase to bring energy, innovation, and purpose to the conversation about crypto’s future. It’s all about the builders working on real-world use cases that will shape what’s next 💪

@standwithcrypto#StandWithCrypto

I'm thinking about a potential exemption from registration that would allow firms to use DLT to issue, trade, and settle securities. A sketch of the idea is here: https://t.co/FwqKvVbhOy

I just had the honor and privilege of chatting with the Crypto Task Force and SEC Commissioner @HesterPeirce about a critically important topic. And truthfully, I had lost hope a while ago that this day would ever come.

As recently as last year, crypto projects were being sued left and right. You were lucky if you were just able to build, let alone talk about what you were building. But the tides are turning. I went to DC because I believe that America can and will usher in a new Golden Age if it embraces the good that Web3 can bring.

We had a very simple agenda: talk about the good that a group of us as builders in the US have already seen, and the ownership opportunities we are pioneering as DAOs and onchain cooperatives.

A full episode on the learnings and our experience going where few crypto projects have before will be coming to @coinage_media - but for now, I am so hopeful for the country and for crypto.

We’re finally moving on and ready to focus on the good that Web3 can bring and I can’t thank both Commissioner Peirce and her tireless staff enough for leading the charge.

Forward. 🇺🇸

Had a thoughtful conversation with @BoHines, Executive Director of the President’s Council of Advisers on Digital Assets of the White House, about Ethereum and the broader impact of ETHDenver.

Exciting times ahead!

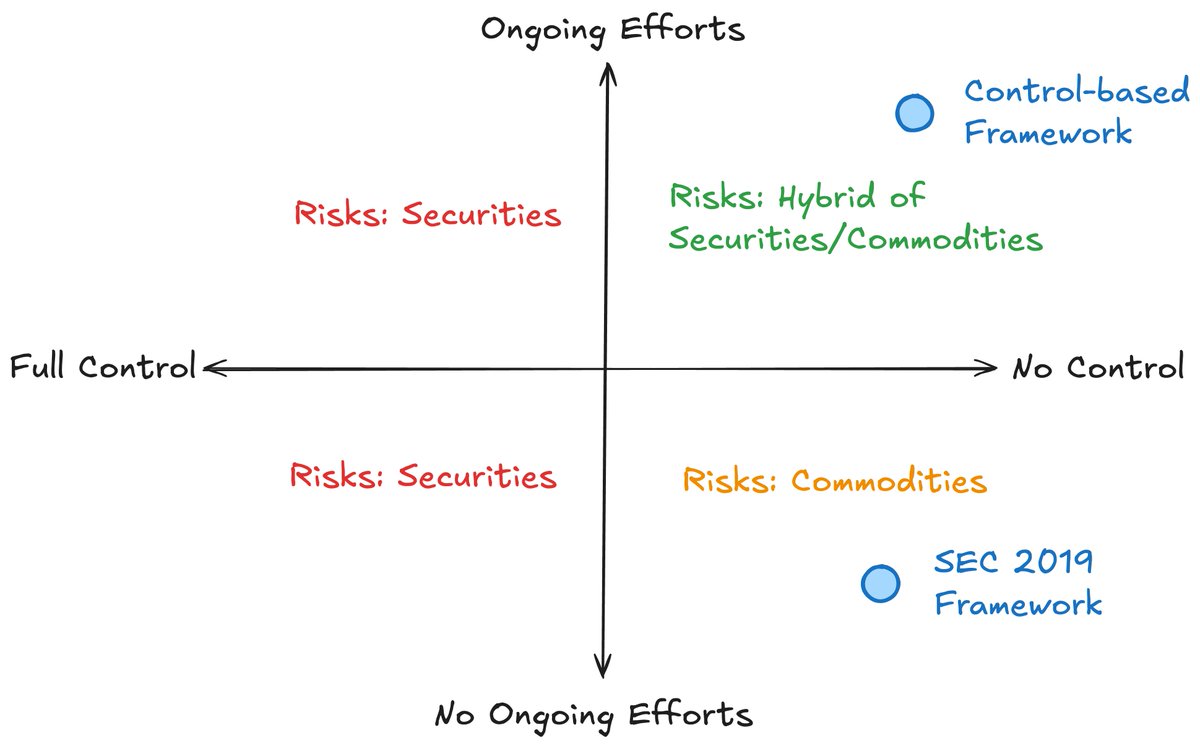

The SEC’s decentralization framework has been corrupted and used to persecute builders —incentivizing rug pulls over value creation.

It’s time to fix it.

Decentralization should mean the absence of control, not the suppression of ongoing efforts.

Here’s how and why👇

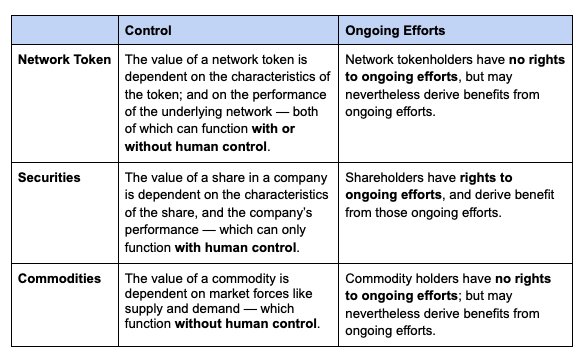

Network tokens — tokens that derive substantial value from the operation of a blockchain (eg BTC, ETH, SOL) — can have embedded trust dependencies that result in information asymmetries.

Where those trust dependencies are minimized, network tokens look like commodities with low information asymmetry risk.

Where those trust dependencies are significant, network tokens can look like securities with high information asymmetry risk — supporting the use of disclosures requirements under securities laws.

The two primary trust dependencies relating to network tokens are: (1) control and (2) ongoing efforts.

The SEC’s 2019 Decentralization Framework sought to eliminate the risk of information asymmetries by defining decentralization to mean the absence of BOTH control and ongoing efforts. Their reasoning was clear — where network tokens were “sufficiently decentralized” tokens functioned more like commodities.

But this is the wrong approach!

It’s created significant perverse incentives — builders can actually reduce their regulatory risk by abandoning their projects or by masking their ongoing efforts (“decentralization theater”).

Builders HATE this conception of decentralization.

We need to incentivize builders, not hinder them. A better two-pronged approach can achieve this:

1⃣Decentralization should be redefined as “the absence of control.” This eliminates significant risk and preserves one of the core features of blockchains – they can function without human control.

2⃣A targeted and light touch disclosure framework can be used to eliminate information asymmetries that might arise from ongoing efforts.

Collectively, this approach would foster innovation and protect users – ensuring decentralization empowers builders rather than being weaponized against them.

Full article linked below.

1/ The tide keeps turning 🌊Comm'r @HesterPeirce has been thoughtful on crypto for years. Now she's leading the SEC's regulatory efforts on crypto thru a new task force. The priorities (in /2) are on point. Grateful for the leadership from Acting Chair @MarkUyedaUS on this.

The Overton Window has been smashed.

If everything is now legal[1], many startups will try raising funds by issuing tokens as explicit cryptoequity.

As context, the SEC distorted the market for the last decade by forcing founders to obscure the obvious analogy between tokens and equity.

But there is nothing *morally* wrong with moving equity from spreadsheets and NASDAQs to blockchains.

Indeed, from a *technical* perspective it’s far better to represent equities onchain. You can hold them in a wallet, price them with an API call, and track them on an explorer. You can also easily issue dividends, execute buybacks, and manage vesting schedules.

And from a *financial* perspective, there is no contest between the global market of crypto investors and the local market of any given city.

But that shouldn’t mean short-term behavior. Founders can (and should) implement lockups, drag along, cosale rights, and the like. All these conventions align long-term interests of investors and founders.

You could get there by using AI to translate a typical Series A package into a set of smart contracts. And exchanges should step up to help retail by clearly identifying assets that implement long-term, value-aligning lockups.

At least, that’s the responsible game plan for using new technology to fund actual companies. I hope we use our powers responsibly, and will fund projects in this space as we gain more legal clarity.

But we may *finally* enter the long-overdue age of the cryptoequity.

[1]: Obviously this is a rhetorical overstatement. It’s not literally the Purge. But as with the uncensoring of X, there is an enormous range of new things that is now apparently permissible to do — some good and some bad. And a risk-tolerant community will surge into that space to explore what’s possible.

This is one of the downsides of regulating by enforcement. All the SEC did was shoot at good people rather than make good rules. Perhaps the moment was simply beyond their capabilities, and the regulation will de facto fall to the crypto exchanges.

In other words: we don’t yet have rule-of-law. All we have is rule-of-code. And that may be how it lands up.