$SPX is down 190pts and fixed strike vol is hardly up 1pt and VX 2pts. This is what you get when we see skew at extremes and historical spot/vol correlations.

“I wanna be a trillionaire… so frickin’ bad, buy all the things I never had”

VOO crosses Elon territory…

Some stats: 43% was due to asset appreciation, 57% from inflow — 62% of flow came from just the past three years

@t1alpha

In the short term, the U.S. market is filled with end users who are forced to transact. Their urgency to fulfill specific mandates creates numerous small price fluctuations across derivatives and equities, this naturally has a ripple effect across a wide range of time horizons.

Over the long run, many market participants consistently underestimate and underprice outlier events in the derivatives market.

Put those two principles together, and I believe you end up with something both special and robust.

Today's lesson from NVDA earnings: Heavy call buying into earnings was a supply problem

I keep coming back to this one into earnings season.

When you see skew flatten in a stock ahead of a print, that's telling you there's been call buying. And with that setup, there's a problem waiting on the other side.

When vol resets after the earnings, all the delta that's sitting hedged against those calls, that delta needs to be sold. So if the result doesn't justify a massive move higher, just the reset lower in vol provides a load of supply of stock to the market post-earnings.

So you've got this hurdle the stock has to climb just to stay higher, even if it's a beat. That amount of shares has to come back to the market, unless you go through the strikes and the calls go in the money.

If you get a knee-jerk higher, there's pressure to sell into that knee-jerk. And if you don't get a good number, all those calls evaporate pretty quick, and the stock comes to sale very fast.

For me, that's the base case. Whatever the earnings are, you probably get that supply of shares, and it takes the stock down or at least makes it hard for the stock to stay up.

That's the vanna effect.

Good morning my loves, happy Saturday. Sorry I've been quiet, obviously been busy, but thought it'd be nice to give you all the details on the multi-strategy absolute return program that experienced the 28% drawdown this year. (1/n)

Spot/vol beta continues to break: only upside volatility for you! To explain why we’ve been seeing market up + vol up over this past week and what that can mean for the future, you have to go back to the most recent decline in Feb-Mar. Essentially throughout that entire $SPX drawdown, we never saw a big pickup in realized vol as daily mean reversion was the name of the game. Gamma hardly performed at the index level and dispersion traders were just printing PnL.

You can pick whatever catalyst you like for why SPX bottomed but it has literally gone just vertical since. The right tail was clearly suppressed (partly from overwriting) and the market was well hedged during the decline, illustrated best in skew. Last week SPX was up another 200pts and it’s caused vol to carry with it and for basically the first time since last year, we see gamma performing extremely well. This is for 2 main reasons. When the market just rips up the curve, it causes skew to steepen which will mechanically drive vol higher. It’s also due to the persistent buying of long calls in which dealers will raise the vol surface to account for this.

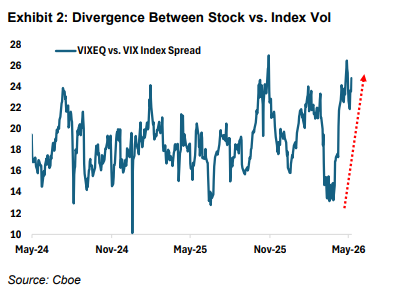

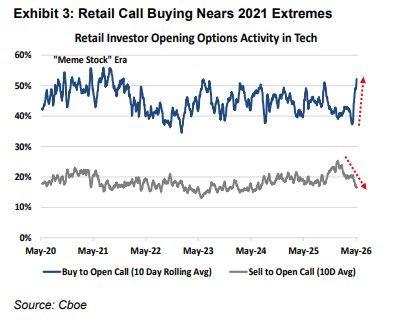

CBOE notes that retail call buying is approaching the 2021 meme stock frenzy levels, “As Tech has outperformed, so has the demand for optionality in Tech stocks, particularly on the call side. We’ve seen a sharp uptick in call buying activity from retail investors on our exchanges, with over 52% of all retail opening activity in 10 mega-cap Tech stocks (Mag-7 plus AMD, PLTR, and AVGO, which collectively make up the Cboe Magnificent10SM Index, or MGTN Index) consisting of call buying.”

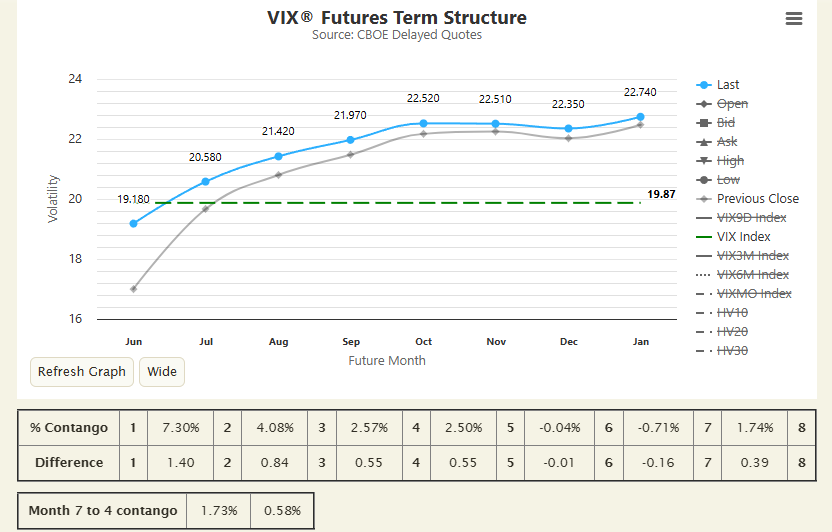

When we see a longer period of market up + vol up, what typically happens is that SPX will carve out some sort of pause/pullback into a market down + vol down situation until the complex “resets.” What’s more uncommon but would be quite telling of larger participants current positioning is if SPX pulls back into a market down + vol up situation, moreso if vol outperforms that pullback. Something like a SPX down 50-75pts and fixed strike vol up a few pts. We’re approaching $VIX expiry next week so I’d be watching how /VX performs on any SPX moves here given the proximity.

The Strait of Hormuz Reverse Uno Card

When Raji Khabbaz and I were running Silver Arrow Investment Management, whenever we were trying to figure out why something happened, he was unsatisfied the explanation that people are sometimes stupid and institutions are often stupid. He correctly thought that people usually have a good reason (at least to them) for doing something even if it appears to make little sense to an outsider. More importantly, he thought that “sometimes people are stupid” was a lazy answer that was dismissive. As investors, it was our goal to understand what was happening, not to ignore it.

Recently, I’ve written that many of President Trump’s critics are making the same error. When Iran closed the Strait of Hormuz, the narrow waterway that previously transported 20% of the world’s oil supply, the price of oil rose. Gas prices in the US have risen in response. Many screamed that this was an obvious move by the Iranian regime and insisted President Trump should have known it was something they’d do. How could he not know?!

In 2002, the US Navy conducted war games they called the Millennium Challenge. One side represented Iran. The other represented the technologically superior US Navy and included an aircraft carrier, warships, and cruisers. The US Navy side had a substantial advantage in firepower. Retired Marine Corps Lieutenant General Paul K. Van Riper used asymmetric warfare tactics to wipe out the US side in one day. Had this been a real fight, the US would have lost 20,000 servicemen. The result was such an embarrassment that the Navy re-floated the sunk ships, changed the rules of engagement to ensure a US victory, and started the challenge again.

These games were not a secret. They have been widely covered in the mainstream media and have been the subject of a New York Times documentary. Over the past two decades, I have seen the Millennium Challenge discussed in my daily financial news reading at least a dozen times. The event has its own Wikipedia page. Regardless of your opinion of President Trump, do you really believe that neither he, nor anyone in the White House, nor any of his military advisors, nor Secretary of War, Hegseth knew about this? I realize that many of you reading this have strong negative emotions regarding President Trump. I’m not asking you to like or respect him. I’m just suggesting that “he’s stupid and has no idea what he’s doing” is not good analysis. This is a point I’ve made in this space in the past.

Early in the war, Iran closed the Strait which placed economic pressure on the rest of the world. Despite the fact that it was Iran mining the Strait and shooting at the ships that attempted to navigate it, many countries expressed anger at the US and Israel. This was the outcome Iran wanted. Then, the regime decided to allow friendly ships to pass if they paid a fee. The fees were about $1/barrel of oil, or about $2MM per large container vessel. (Many of these fees were paid in Bitcoin, something macro analyst, @peruvian_bull, explained in an excellent post within the past week.)

This looked like worst-case scenario for the US. Iran succeeded in closing the Strait and causing economic problems all over the world, then found a way to profit from their own actions. Then, President Trump played his “reverse uno” card. He correctly realized that it wasn’t just the rest of the world that depended on free passage through the Strait of Hormuz, and that it was Iran that had the most exposure. Iran is a big oil producer, and oil exports account for 80% of Iran’s exports, 60% of government revenue, and 25% of its GDP. It turns out that Iran has more economic exposure to this narrow waterway than anyone else. President Trump sent the US Navy to form a blockade. He closed the Strait himself ensuring no more $2MM/vessel charges and an inability for Iran to export oil.

Iran is close to filling its own storage. Once its oil tanks are full, the regime has two choices, either capitulate and come to an agreement with the US, or to stop producing from its own wells. The problem with the second choice is that it’s difficult to reverse. Stopping production on an active oil well tends to damage it and it’s hard to re-start later. Iran now has a limited amount of time to find a course of action before 25% of its GDP becomes permanently(ish) impaired.

While no one in the US likes paying more for gas, prices were much higher just four years ago in 2022 and around $4/gallon in 2008, 2011, and 2012 when $4 had more purchasing power than it does now. The US is a net energy exporter with an economy that has survived higher prices in the past. Foreign ships are turning away from the Strait of Hormuz and sailing to Texas and other southern US ports to fill up at premium prices. I’m not suggesting that this is great for the US; but rather, that the US is well-suited to manage the situation while Iran is about to be faced with a massive long-term problem.

Finally, Iran maintains control of the country using extensive human infrastructure. There are police everywhere monitoring protests, internet usage, the attire of citizens, and the hair of Iranian women. That level of control is expensive and the government just lost 60% of its revenue. I’m wondering how long they’ll keep doing their jobs without paychecks.

I don’t know how this conflict will end. What I do know is that President Trump and the US Navy have turned Iran’s biggest strategic strength into a giant weakness. Sometimes people do stupid things. And sometimes, we just aren’t seeing the reasoning behind those actions. Last week, one of DKI’s interns wrote, ”The bottom line is that (financial analysis) can tell you what the market’s pricing in, but it’s your job to figure out why”. Right now, the mullahs are facing a difficult decision. It will be interesting to see what comes next.

The most retarded thing about the war was liberals taking statements from representatives of Iran at face value just because they contradicting Trump‘s 😂😂😂

SPX recovered back to 7100 in a straight line and index vol is refusing to die.

Normally, a 5% vertical rip on "peace" headlines would incinerate index vol. Instead, it’s sticky. Fixed-strike vol is materially higher on the move.

Here is why: The Implied Correlation Floor.

We just saw one of the fastest SPX recoveries in history. Implied correlation followed the skew down so fast that it’s already back at the "hard deck" near 10.

Here’s the mechanics...

We are heading into the heart of earnings season. Single-stock vol is staying bid, which is normal but because implied correlation is already at 10, it has no real room left to drop. It can’t go to zero, and it sure as hell can’t go negative, especially when realised has been quite high lately.

So when single-stock vol refuses to come down, and implied correlation can't drop any further to offset it, the math forces a "scramble bid" into index vol just to keep the surface aligned.

The more we rally, the more index vol has to float higher to maintain that 10 floor in COR1M.

This isn't a "fear" bid. It’s a structural squeeze. The dispersion trade: short index vol, long single-stock vol is hitting a mathematical limit. The "correlation discount" has been fully harvested, leaving index vol as the only release valve.

What this tells me is...

Index vol will continue to perform in a rally and it will only be able to come down materially after earnings season has played out.

I'm going to be brutally honest here

I pay almost no attention to news headlines

they almost never feature in my market analysis-

and if they DO, my outcomes are almost always worse

(short thread)

This rally is being driven by forced buying.

Hedgies were short.

CTAs are being forced back in.

It’s not people buying because they want to. It’s buying because they’re forced to.

If the news flow deteriorates, the same people will have to sell it again.

So the question is what happens when the flow stops.

You’re not only trading market direction but instead this is more trading positioning.

This is not where you want to be short gamma.

I see it as:

Deal gets done: market keeps ripping.

Deal fails: market sells off.

Supportive flows are fading.

Event risk is rising.

Do I want to be running short gamma into the weekend with Monday's straddle priced at less than 1%. Probably not.

This is exposure to uncertainty, not a view.

@BenKizemchuk This isn’t a collar move. That was last weeks news. Look at the vix curve. Vols down across the board 8 months out. What does that do to the delta hedging on any customer bought put.

@BenKizemchuk Brother do you understand how delta and gamma work? Dealers are long those calls, the collar acts as an accelerant into 6850. Not a ceiling.

Like I said, the collar JUST rolled last week. Its effect is not as pronounced as it is closer to JuneQ exp.

you watch the vid lol