Somewhere deep in the Nevada desert.

Past the last gas station and left of the blinking light in the sky.

Sits a tiny diner, where the coffees are hot, the pies are fresh and the staff knows not to ask too many questions… 🛸

Coming this Friday.

#TheFlyingSaucerDiner

With Pending Acquisition of Siiibo Securities, Metaplanet Poised to Bring Bitcoin Yield to Japanese Households; Would Represent First Step in Plan to Create of Bitcoin-Centric Ecosystem in Japan - Benchmark Equity Research

June 11: Japan’s lower house passes bill moving crypto from payments law to financial-product rules, effective within a year.

June 12: Metaplanet acquires 100% of Siiibo Securities, adding a regulated Type I securities platform to build and distribute BTC-linked yield products.

I did a bit of a deeper dive on @Metaplanet acquiring Siibo and rolling out Metaplanet securities. Siibo has an online retail base and has typically sold bonds with a 1-3 year duration at a 2-8% coupon. The coupon is paid annually or semiannually, and the bond is paid back at maturity. The payment of the coupon and the repayment of the bonds at maturity will be covered by the income generation business and will scale as the $BTC treasury grows.

Because metaplanet has the highest level licensing to issue bonds, they have a very exclusive engine and can use the revenue to purchase more bitcoin for the treasury with zero common equity dilution.

They will also be able to issue bonds for corporations and even sovereigns that are looking to build their own bitcoin treasuries. This will also generate income from the fees for issuing those bonds and will serve as additional income for buying BTC. Again, all of this with zero common equity dilution.

There is no amplification with bonds, like with Preferred’s, or the need to sell the common equity to pay dividends. I’m certain they will be adding Preferred’s as well, but Metaplanet securities is going to be highly accretive to the common stock and $MPJPY.

These will be the first Bitbonds ever issued. A brilliant move by management to capture the idle cash sitting in near zero yield accounts in Japan, while highly accretive to the shareholders. 👏🫡

Good Evening Japan

The Siiibo acquisition. $13 million, small number, big deal. The timing is the entire story, and once you see it you cannot unsee it.

June 11: Japan's lower house passes an amendment to the Financial Instruments and Exchange Act, the FIEA. For those who don't live in Japanese regulation, the FIEA is Japan's securities law, the rulebook that governs stocks, bonds and investment trusts. Until this week, crypto sat outside it, regulated as a payment method under the Payment Services Act, basically the same legal bucket as a gift card. The amendment moves crypto into the securities rulebook. That one reclassification changes everything downstream: regulated crypto investment products become legally possible for the first time, run by licensed securities firms, and the tax on crypto gains is set to fall from a maximum 55% to a flat 20%, the same rate as stocks.

June 12: Metaplanet announces it is acquiring Siiibo Securities, a Type I Financial Instruments Business Operator.

A Type I license is the top tier of permission under that exact law. It is what lets a firm deal in securities, run a brokerage, and sell financial products to ordinary Japanese investors. The FSA does not hand these out, you either wait years for one or you buy a company that already holds one. Metaplanet bought one. For $13 million.

One day apart. Gerovich bought the exact license category the new law empowers, the morning after the law cleared its biggest hurdle. He front-ran the regulation. That is what "pieces being put in place" meant.

Now read the filing language closely, because they told you the product roadmap in one line: BTC-related instruments, security tokens, and digital credit. Digital credit. Saylor's exact vocabulary, now sitting in a Japanese regulatory filing. Metaplanet is importing the Strategy capital stack into the largest pool of idle savings on earth, ¥1,190 trillion in household deposits earning nothing, right as the tax penalty for touching crypto gets cut from 55% to 20%.

And understand the arbitrage window. SBI has already filed for Bitcoin ETFs targeting ¥5 trillion in AUM, but the regulator is targeting fiscal 2028 for first approvals. That means for roughly two years, between Siiibo closing and ETFs arriving, a licensed Metaplanet Securities can be effectively the only regulated channel selling Bitcoin yield products to Japanese retail. First mover, in a market with no incumbent, with the regulator actively paving the road.

So here is the map I think from today

Late June or July: the bill goes to the upper house, where passage is widely expected. No vote date is set yet. My call is it clears before the parliamentary session ends. This is the starting gun.

July: Siiibo closes, renamed Metaplanet Securities, pending regulatory sign off on the change of control. The Metaplanet Card launches this summer alongside it. The retail front door opens.

Q3 to Q4: the first BTC-linked bond issues through the Metaplanet Securities platform. This is my highest conviction call. Siiibo's entire specialty is online corporate bond issuance, over 100 offerings for 40+ companies. The fastest product to market on those rails is a yen bond with BTC-linked yield, backed by the 40,177 BTC treasury. Digital credit.

Q4: the Mars and Mercury re-filing with the Tokyo Stock Exchange. Eight quarters of income business track record by the November print, an in-house securities arm to support distribution, and a regulator that just reclassified the underlying asset as a financial instrument.

October: TOPIX decision. A licensed securities subsidiary, a card business, a media arm and an options desk is the counter-argument, filed and operating.

Q1 2027: Mars and Mercury list. First perpetual preferreds in Japanese market history.

Fiscal 2027: the new securities framework takes effect. Crypto becomes a financial instrument in law, and the Tokyo Stock Exchange has signaled crypto ETFs could list as early as this window.

Winning.

Big news from Metaplanet.

The acquisition of Siiibo Securities gives them direct distribution for their Bitcoin-backed fixed income products straight into the Japanese market.

This is about owning the entire pipeline from issuance to distribution.

Metaplanet is positioning itself to dominate Bitcoin credit in Japan and become core infrastructure for the entire Bitcoin ecosystem in the country.

Monopoly is not too strong a word.

Bullish on $MTPLF | $MPJPY.

Metaplanet Securities / Siiibo acquisition

It's been a minute since #Metaplanet gave us something fun to talk about.. So here's what happened, and my read on it in case anyone's interested.

Today, Metaplanet announced its first acquisition: ¥2.1 billion (~$13M) in cash for 100% of Siiibo Securities, an online corporate-bond platform that will be renamed Metaplanet Securities. Closing July 13, wholly owned by August. The impact on 2026 consolidated results will be minor, at 0.46% of the company’s ¥457.6 billion Bitcoin NAV. The strategy behind it though, is anything but minor.

Start with what they paid. Siiibo earned ¥156M of revenue in FY2025 and lost ¥175M doing it; net assets are ¥587M. Metaplanet paid 3.6x book for a business that has never been profitable. The filing explains the premium in its own pricing rationale, and the first factor listed is telling: the total costs and time-to-market benefits of obtaining a new Type I Financial Instruments Business registration from scratch. A Type I license is what lets a firm structure and sell securities to the Japanese public. This is a license acquisition. So they bought time, not earnings. And that can be worth a lot.

And 3.6x book is cheaper than it looks. Most of Siiibo’s ¥587M net assets is regulatory capital any Type I operator must hold regardless. The cleaner read: Siiibo’s capital stock alone is ¥1.6B and it burned ¥497M over the last three years — the VCs behind it are exiting a seven-year build at roughly cost. Metaplanet paid less than it cost to create the asset. The caveat though is that the headline isn’t necessarily the full commitment: the filing flags capital injections and parent loans for the growth phase, on top of the ¥175M annual burn.

The reference deck shows what the license is for. Its cover promises to bring “Yield” to Japan, against a dormant ¥1.190 quadrillion opportunity: total household financial assets, ¥1,140 trillion of which sits in cash and deposits. And the first product category, issuance planned: Digital Credit — perpetual preferred shares backed by Metaplanet’s 40,177 BTC.

On May 13, Metaplanet flagged that the TSE listing of its MARS and MERCURY preferred shares is taking longer than expected. Japan has never listed a perpetual preferred — Metaplanet’s would be the first — and the exchange wants preferred dividends backed by recurring cash flow proven across market conditions before they allow it. On June 9, the company cut the floor exercise price on its 27th-series warrants from ¥298 to ¥187, with nothing exercisable below 1.01x mNAV. So while Metaplanet works through the regulatory roadblocks to get the prefs listed, it needs to start building the operating cash flow the exchange wants to see — and with the equity engine parked too, both routes need an answer.

Siiibo is the route that needs neither. Its entire platform is selling unlisted, privately placed bonds online to vetted investors — and today’s notice says Metaplanet will explore “the offering of private placement debt products leveraging the Group’s credit profile and Bitcoin treasury strategy.” The JPY yield products don’t have to wait for the TSE. Better still, the distribution and structuring fees a securities arm earns are exactly the recurring cash flow the exchange asked to see. The acquisition routes around the listing delay and answers the exchange’s objection at the same time.

It also completes a stack. Metaplanet issues preferred shares — Class B is outstanding, the perpetual shelf was filed in August 2025. Metaplanet Asset Management, established in the US in March, structures. Metaplanet Securities distributes — “a direct channel to develop and distribute Bitcoin-related financial products to investors.” And the deck draws the flywheel openly: platform cash flow funds preferred dividends and expands preferred issuance capacity — “More BTC. More Cash Flow. More BTC.”

The language signals more to come. The filing calls this the “first major M&A transaction” under Project Nova, and the deck lists the registrations under consideration next: crypto-asset exchange, OTC derivatives, custody, lending, asset management. Funding is cash and borrowings.

If this feels familiar, it should. In July 2025, Simon (@gerovich) floated using the Bitcoin stack as collateral to buy cash-generating businesses — a digital bank in Japan was the example — and the idea was widely panned as a loss of focus. Eleven months later, that exact playbook just executed: borrow against the BTC if needed, buy a regulated financial business, point it at the treasury. The instrument changed — a securities firm is a faster, cheaper license than a bank — but Phase II didn’t die.

The downside is a small, money-losing broker burning ¥175M a year — 0.04% of NAV. The upside is a regulated sales channel into the largest pool of yield-starved savings on earth, and a second engine for BTC-per-share growth that doesn’t need mNAV above 1 or a TSE rulebook that doesn’t exist yet. If Digital Credit launches, Metaplanet sells yen yield to Japanese households and converts the proceeds into Bitcoin at the HoldCo layer.

The Pharaoh’s view: most treasury companies talk about adoption; Metaplanet spent 0.46% of its balance sheet on its own distribution because Japan’s market infrastructure is holding them up. I’m (very) long the stock with a long term view, and expect the team to continue executing and building what will become the most valuable company in Japan. Not financial advice - don’t do what I do.

Filings (TDnet):

Share transfer agreement (EN): https://t.co/ptVQcA7mEf

Supplemental deck (EN): https://t.co/8ynNg19W8o

Japanese original — notice: https://t.co/qkl5RtRyIT

Japanese original — deck: https://t.co/GCN05SbzxO

All disclosures: https://t.co/NHqR6xN3qf

$MPJPY $MTPLF

The strategic meaning of the Siiibo acquisition may go far beyond Metaplanet’s own financing needs.

Siiibo is not just a small securities company. It brings a regulated bond platform, a Type 1 Financial Instruments Business registration, and direct access to Japanese income seeking investors.

Metaplanet now has the potential to build a regulated distribution layer for Bitcoin related credit products in Japan.

The obvious first step could be Metaplanet’s own products, such as private bonds, Bitcoin linked income products, or future digital securities.

But the larger opportunity may come from third party issuance.

Companies, funds, or large Bitcoin holders could potentially issue Bitcoin backed bonds through Metaplanet Securities into the Japanese market. They would receive yen liquidity without selling their Bitcoin, while Japanese investors would gain access to income products supported by Bitcoin collateral.

In that scenario, Metaplanet Securities would sit in the middle as the regulated platform for origination, distribution, investor access, and possibly the collateral structure.

This would turn the acquisition into something much bigger than a simple financing tool.

It could become the foundation for a Bitcoin backed credit market in Japan.

That is why I think the next important announcements to watch are not only about Metaplanet’s own balance sheet, but about product structure, custody, collateral enforcement, third party issuers, and the first Bitcoin linked securities distributed through Metaplanet Securities.

Confessions of a Haunted Bitcoiner

Nobody warns you about the part that actually gets to you. It isn’t the volatility. It’s the loneliness of the volatility. I can stomach watching half the number evaporate — a 50% drawdown isn’t a crash, it’s a sale on the scarcest monetary asset humanity has ever invented. What I can’t stomach is sitting in a Bavarian lakeside town this summer, the water so still it looks photoshopped (no, I’m not German, I just enjoy the cooler weather) — while my brother-in-law explains to me, slowly, like I’m a golden retriever, that bitcoin “isn’t backed by anything.” This, while he carries a currency backed by the feelings of a committee that meets eight times a year and has never once been early.

Because I’ve done the work. Thousands of hours, between podcasts, books, articles etc. And then you’re stuck. You sit across from people you genuinely love, who built businesses or went to top universities, but you still can't hand them the one thing you’re surest of in this life. You watch the words leave your mouth and die in the air. “Inflation is policy.” Nothing. You’ve said something profound to a man squinting at the bill to see if service is included.

So you stop. Not because you stopped believing — because you’ve learned, at real cost, that conviction and evangelism are different muscles, and the second one only ever cost me. The early bitcoiner’s true discipline was never holding through an 80% crash. It’s holding your tongue at brunch while someone calls your life’s thesis a Ponzi between bites of a croissant they bought with money engineered to be worth less by the time they finish it.

And here’s the confession underneath the confession — the haunting part. A small, ugly corner of me wants the price to keep bleeding. Not for me. For the vindication. So they’ll finally see. And I despise that corner, because I already know the ending: the converts arrive years late, exhausted, having “figured it out themselves,” and I’ll have to swallow the most expensive three words in the English language — I told you — smile, and pour the wine. Because being right early and being right late feel exactly the same from the inside. The only difference is who got paid, and whether you stayed someone people still wanted at the table.

That’s the trap nobody mentions. It’s lonely being the only one who sees the iceberg. But you can’t save the ship by screaming “ICEBERG” louder — you just become the iceberg guy, and now you’re not even right anymore, you’re exhausting, and exhausted.

So you make a quieter peace with it. The math doesn’t need their approval. 21 million is 21 million whether anyone claps, whether your brother-in-law ever comes around, whether the number is at 60K or 600K this particular haunted Sunday.

But here’s the part I didn’t expect. You spend years being the only one at every dinner table — and then you find the others. Not at the table. But here on X. It turns out the whole time I was losing the argument at brunch, there was a deck full of people on the other side of this screen squinting at the same iceberg, doing the same math, biting the same tongue at their own family dinners. We’re not an echo chamber — an echo chamber agrees on conclusions. We argue about everything: cycle tops, treasury structures, whether Saylor’s a prophet or a margin call away from his next podcast appearance. What we share isn’t an answer. It’s the humility to question everything we once knew, and the foresight.

I used to think being early meant being alone. It just meant being early to the wrong room. This is the right one.

Now let's ride this bear to zero or a million 😎

#Bitcoin $MSTR $MPJPY $MTPLF

A lot of pieces are being put in place right now at Metaplanet. Individually, none of them tell the full story. Together, they will. We are working harder than at any point I can remember to get them right. I wish I could share more. Soon enough, the picture will speak for itself. We are building this company for the long term, and for every shareholder who is along for that journey.

いまメタプラネットでは、様々な取り組みが少しずつ形になりつつあります。個別に見ても、全体像は見えてきません。すべてが揃ったとき、初めて意味を持ちます。私たちは、これまでにないほど真剣に、その一つひとつに向き合っています。今はまだ多くを語れないのが歯がゆいですが、時が来れば、自ずと見えてくるはずです。私たちはこの会社を長期視点で築いています。そして、その歩みを共にしてくださるすべての株主の皆様と共に。

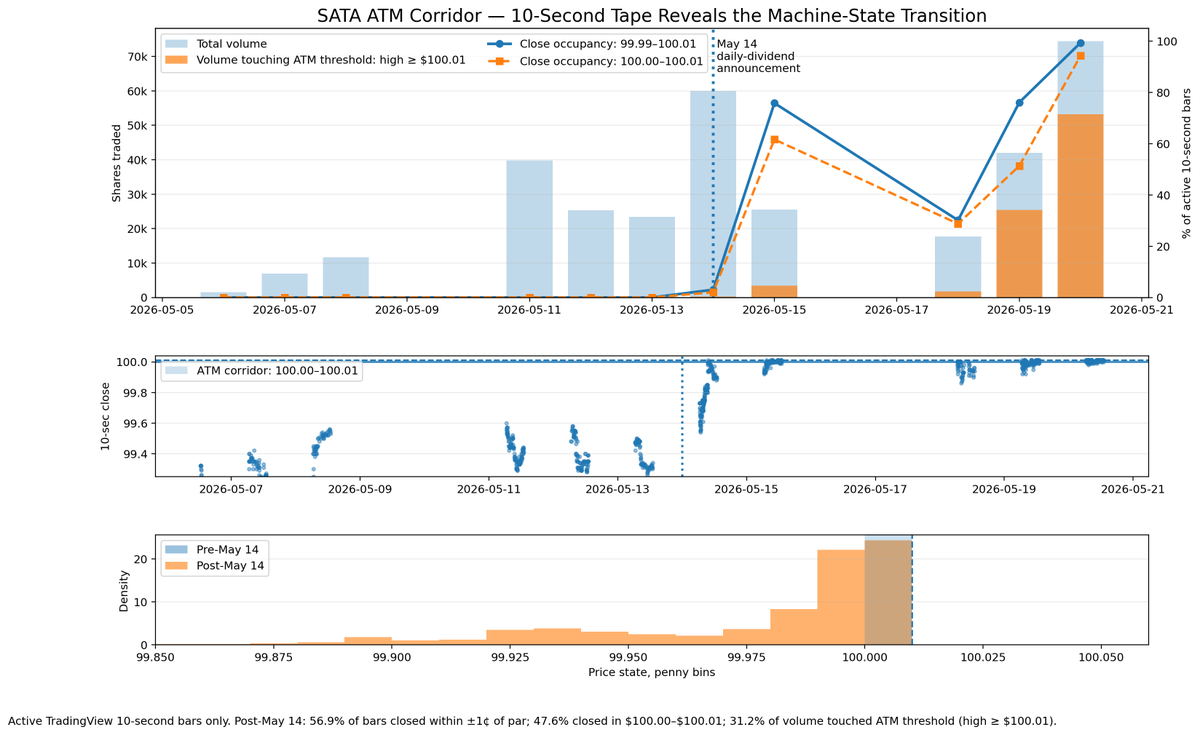

Everyone missed what $SATA and @Strive actually did.

The easy narrative was: “people want to get paid more frequently, like a money market fund.” That’s retail framing and perfectly fine.

That’s not how sophisticated capital allocators or high-frequency systems think.

Looking at SATA at the 10-SECOND level reveals something much more important:

Post–May 14, the stock entered a machine-readable equilibrium state around par.

Volume increased while price behavior compressed into an ultra-tight ATM-active corridor around $100.00–$100.01.

56.9% of bars closed within ±1¢ of par

47.6% closed specifically inside the ATM corridor

31.2% of all volume touched the issuance threshold

This is not “lower volatility.” It’s state compression.

Humans hear: “daily dividends.”

Algorithms see:

deterministic corridor

persistent liquidity

continuous issuance optionality

low entropy

machine-friendly equilibrium

SATA may not just be a preferred stock.

It may be the first Bitcoin treasury instrument intentionally optimized for algorithmic trading microstructure. @ColeMacro@PunterJeff@Werkman@AdamBLiv@hillery_dan

Metaplanet's US Strategy: What Metaplanet Is Building in the US — Connecting Every Dot

Over the past couple of weeks, #Metaplanet management have been dropping clues that they are preparing something significant on the US side. We can all guess what it is (and there are several possibilities) but it’s becoming increasingly clear that something is in the works. Here’s what I’m seeing.

The chronological US buildout

A 13-month progression that doesn't look incidental when you line it up:

→ April 2025: Metaplanet Treasury Corporation (Miami) established — highlighted by COO Yoshimi Abe on May 7: "One year ago, we established Metaplanet Treasury Corporation in Miami, our first US entity." https://t.co/HchHevtxFs

→ July 2025: Establishment of US Holding Subsidiary and Share Transfer by Way of Contribution in Kind

→ September 17, 2025: Metaplanet Income Corp (US) established — specifically to operate the Bitcoin Income Generation business out of US jurisdiction

→ December 12, 2025: Form F-6 filed with SEC — registration of Sponsored ADR shares

→ December 19, 2025: SEC declares the F-6 effective. Sponsored Level 1 ADR launches under ticker $MPJPY with Deutsche Bank Trust Company Americas as depositary and MUFG Bank as custodian.

→ March 12, 2026: Strategic-disclosure day. Three coordinated filings drop together: • Establishment of Metaplanet Asset Management (US subsidiary) • Establishment of Metaplanet Ventures K.K. (Japan venture arm) • Investment in JPYC Inc. via Metaplanet Ventures

I want to pause here for a minute and share a excerpt from their own filing: https://t.co/q2L58LJaRY

This is the actual language from Metaplanet's March 12 filing announcing Metaplanet Asset Management:

"The Company sees an opportunity to establish a dedicated asset management platform to serve this market, bridging Asian and Western capital markets."

The same filing goes further. It explicitly names the product set: "perpetual preferred securities and related fixed income instruments, a category increasingly referred to as Digital Credit" — alongside "actively managed strategies… derivatives and structured positions, equity and credit strategies focused on Bitcoin treasury companies… index products and benchmarks."

Then it commits to the rollout: "The Company intends to announce specific funds, managed strategies, and structured products as they are launched, spanning the full spectrum of Bitcoin capital markets from yield instruments and fixed income to actively managed equity, credit, commodity, and volatility strategies."

This plan was disclosed two months ago in plain English in a filing on their website. This has been in the works for some time.

A perpetual preferred ("Digital Credit") is the most likely first product IMO. But it's the first product in a platform, not a one-off raise. Metaplanet Asset Management is the operating engine for a multi-product Bitcoin capital markets business — issued out of US jurisdiction, designed from inception to bridge Tokyo-listed parent equity, US institutional appetite, and Japanese yield-starved capital into a single ecosystem.

→ March 16, 2026: Capital Allocation Policy revised.

→ April 13, 2026: Metaplanet opens a 60-day fee-free window (Apr 13 to Jun 12) for converting unsponsored $MTPLF shares into sponsored $MPJPY ADRs. Removes the standard $0.05/ADR fee. More on this later.

→ April 26, 2026: Metaplanet lights up the Las Vegas Sphere with "Secure the Future with Bitcoin" — ~$450K/day for premium US institutional visibility. https://t.co/vOQO8nNQdk

→ April 27, 2026: High-tier sponsor of Bitcoin for Corporations at Bitcoin 2026 Conference (Venetian, Las Vegas)

→ May 7–13, 2026: Boston (and potentially other US cities) week-long institutional roadshow. Full senior team: Simon Gerovich (CEO), Dylan LeClair (Head of BTC Strategy), Yoshimi Abe (COO), Shinpei (IR).

→ May 13, 2026: Q1 FY2026 results filed. Same day, coordinated messaging: • Simon: Japan prefs listing "has taken longer than we initially anticipated… we appreciate that this has created uncertainty" — explicit admission of delay. Flagged monthly dividends as a structural feature that would also take time to build. https://t.co/C9lMVUZ3xy • Dylan: "Transforming capital markets is patient work. We will continue diligently, tirelessly, and without compromise, in Japan and abroad." The "and abroad" is not a slip. Shoutout to @swissBTCmaxi for catching that https://t.co/fPl7oRmc7N

Five US legal entities. Sponsored ADR with a major Wall Street depositary. Million-dollar Sphere/conference spend. CEO + COO + Head of Bitcoin Strategy + IR on a senior-roadshow tour. Coordinated same-day messaging.

The fee-waiver window is not a coincidence

Look at the calendar. The fee-free $MTPLF→$MPJPY conversion window runs Apr 13 to June 12, 2026. My projected announcement window for a US perpetual preferred (144A path) is mid-June to mid-July (more on this below). The waiver expires almost exactly when the announcement is expected to land.

This isn't coincidence. Before issuing a USD-denominated perpetual preferred under the same parent, you want the sponsored ADR — Deutsche Bank-backed MPJPY — trading with consolidated, deep, institutionally-clean float. So management compressed the MTPLF→MPJPY migration into a 60-day sprint that ends right as the new product needs the ADR liquidity to launch on top of it.

The pricing reality

A 5-6% rate works in Japan because Japan is yield-starved. It does not work in the US, where the comparable BTC-treasury perpetual prefs already clear at much higher yields - let’s just call it anywhere between 10-14% depending on the instrument and issuer.

If Metaplanet issues a USD perpetual preferred to clear at scale ($200–500M), the coupon almost certainly needs to be 12%+.

The EDGAR reality check

I went to SEC EDGAR to red-team this. Here's what I found:

→ Metaplanet Inc. (CIK 0002100603) has only TWO filings ever: the F-6 ADR registration and its EFFECT notice — both from December 2025. Zero filings in 2026.

→ Metaplanet Asset Management — no EDGAR registration. Not a filer.

→ Metaplanet Income Corp — no EDGAR registration. Not a filer.

→ Metaplanet Treasury Corporation — no EDGAR registration. Not a filer.

→ (Note: "Metaplanet AI Fund I, LP" exists on EDGAR with Estonian principals and AI focus — completely unrelated, just a name coincidence.)

This rules out an imminent NYSE/Nasdaq listing or fully SEC-registered F-1 IPO — those require scaffolding that we'd already see by now.

But it strongly supports a Reg S / 144A private placement path:

144A placements sell to qualified institutional buyers (QIBs) only

Don't require SEC pre-registration

Allow public marketing without quiet period (which is exactly what we're observing)

Can close in 4–12 weeks from pre-marketing

This is the same mechanism Strategy used for $STRC/$STRD/$STRF — initial 144A placement, eventual broader registration

The most likely scenarios, ranked

1. US 144A perpetual preferred. Issued by Metaplanet Inc. or Metaplanet Asset Management, structured like a $STRC clone (or possibly convertible like MERCURY). Sized $200–500M. Targets QIBs initially; broader exchange listing later.

2. Metaplanet Asset Management product launch. Could be a US-domiciled BTC treasury fund or managed strategy that institutional allocators buy into. Distinct from issuing securities directly. Fees on AUM become a revenue line.

3. $MPJPY upgraded from Level 1 to Level II/III ADR. Common stock dual listing on Nasdaq. Simpler, faster, no new instrument. But EDGAR shows no F-3 yet, so this would push to Q4 2026 at earliest.

Some of the scenarios may not be mutually exclusive.

Timeline

If 144A path (most likely):

Roadshow start: May 7 ✓

Anchoring institutional orders: 3–6 weeks

Announcement window: mid-June to mid-July 2026

Pricing and close: 2–4 weeks post-announcement

144A listing / QIB trading start: late July to early August 2026

Closing thoughts

@Strategy is running the best capital markets playbook in financial history. @Strive is doing a fantastic job and punching above its weight.

But the loudest stories aren't always the biggest ones.

Metaplanet is building something none of the others have. Don't write off the dark horse just because there is a new flavor of the month.

They've been training. And they're ready to sprint.

I have some thoughts on the Metaplanet raise + shareholder response:

These retail Metaplanet holders scream for capital raises only at sky-high premiums (3x+ mNAV during BTC euphoria phases), yet when Bitcoin corrects 45-50% - precisely the window where the company must opportunistically issue equity to keep stacking sats....

...they pivot to pearl-clutching over "terrible terms."

The March 16 private placement ($255M at a mere 2% premium + warrants for another ~$276M, total ~$531M war chest) triggered the outrage precisely because it arrived amid the drawdown.

They refuse to wait through the cycle for the next premium-rich window, but demand the company magically time raises to avoid any dilution pain.

That's wanting to eat the flywheel's upside without swallowing a single rotation of its downside.

This is the same cognitive trap that plagued Strategy critics for years. Saylor was relentlessly roasted for "buying every top" and refusing to chase dips aggressively, because the old toolkit (straight equity, convertibles) forced raises when markets were open, not when BTC was cheapest.

The result was consistent accumulation, but never the hyper-aggressive dip-scooping people claimed they wanted.

Only literally two weeks ago, with the scaling of STRC did Strategy finally gain the structural flexibility to hammer dips harder.

That tool didn't exist before and the flywheel was always volatile by design.

Capital raising terms will suck during corrections (more shares issued per BTC bought) and they will become god-tier during rallies (leverage on the balance sheet explodes the mNAV premium, compounding BTC-per-share at rates no static holder can match).

Exactly the same dynamic is playing out at Metaplanet.

Issuing equity at a 1% premium to buy Bitcoin right now is logically optimal even if the terms feel "sucky" on paper, because Bitcoin at deep correction prices is still profoundly undervalued on a multi-year view, and sitting on cash earns you nothing while the window closes.

The alternative (waiting forever for 3x premiums) means you raise less overall, buy fewer sats during the very periods when forward returns are highest, and let the balance sheet atrophy.

I commend ACTION during this dip over paralysis.

Conversely, when BTC rips and the stock premium expands, the same leverage that felt punitive on the way down becomes rocket fuel. Each new dollar of capital buys BTC that then drives mNAV higher, attracting more capital at better terms, ad infinitum.

That's the entire flywheel. It is definitionally volatile.

Premiums compress in corrections (terms suck) and expand in expansions (terms print).

Shareholders who demand raises exclusively at peak premiums while refusing to endure the -45% phases are essentially asking management to violate the cycle itself - to raise only in the green and hide during the red.

That's not how compounding BTC exposure works. It's how you stay small and irrelevant.

The math is merciless. If you only ever raise at "excellent terms," you never scale through full cycles. If you complain every time terms are merely "logical" (1% premium equity for BTC when the alternative is zero BTC), you reveal you never understood the strategy in the first place.

Saylor's pre-STRC era proved the point. Metaplanet's current raise is proving it again.

The patient capital that accepts the full volatility arc wins on net BTC-per-share growth.

The rest are shareholders who never wanted to be flywheel participants - they were tourists who mistook a leveraged BTC accumulator for a stablecoin ETF.

End of story. This is just proof that a lot of people cannot handle the VOLATILITY SUPER DRAGON that is Metaplanet. If you can't comfortably hold it for at least a year, you probably can't hold it for 4 years.

Either diamond-hand the rotations or step off the ride.

The engine doesn't negotiate with feelings.

#Metaplanet Valuation Framework

Market and sentiment-driven noise aside, I wanted to share some thoughts on how I look at #Metaplanet’s valuation. As far as I can see, there isn’t any proper valuation framework published anywhere. Only posts obsessing over whether it trades at a premium or discount to NAV, and even the sell side reports don't really say much. So with that in mind, here's a sketch if you’re interested in some weekend reading to help you get through the Bitcoin winter and/or make up your mind about what MP is really worth.

1. The Starting Point

Metaplanet’s EV per their dashboard: $2.51B

That implies roughly $170M in cash holdings (MCAP + Debt - EV = Cash); this is made up of the ~$100M collateral pool allocated to BIG since the start of the year (which may have been assigned already and the BTC worth a bit less at current prices) plus the ~$80M received Feb 13 from the placement, likely earning options income and/or being deployed into BTC.

BTC holdings: 35,102 BTC

BTC NAV at ~$68K: ~$2.39B

mNAV: ~1.04x

So, you’re paying roughly the value of the BTC they hold by buying/holding MP here. Except you’re not. Because that EV number contains multiple businesses inside it, and significant optionality — and the market is pricing all of them at zero.

2. The Bitcoin Income Generation (BIG) Business

MP monetizes part of its stack (5-10%) through an options-based income strategy that generates ~95% of revenue.

FY2025 actuals:

• Revenue: ¥8.9B (~$58M) — +738% YoY

• Operating profit: ¥6.3B (~$41M) — +1,695% YoY

• Operating margin: 70.6%

FY2026 guidance:

• Revenue: ¥16B (~$104M) — +80% YoY

• Operating profit: ¥11.4B (~$74M) — +81% YoY

• Operating margin: ~71%

This is real cash-generating operating income. Not unrealized BTC gains. Not fair value accounting adjustments. Actual revenue from a scaled, repeatable business that no other Bitcoin treasury company (thus far) has replicated.

And critically, MP's income business scales directly with its BTC stack. A bigger stack means more collateral for options writing, which means more premium income. As they go from 35,000 to 100,000 to 210,000 BTC, the business compounds inline with that growth (unlike other companies where their operating business may not keep up).

3. Valuing the Bitcoin Income Business

A business growing 80% YoY at 71% operating margins in a financial services context would typically command 15-25x operating income (sometimes higher).

Using 15x as our base case (conservative for this growth/margin profile):

$74M x 15 = $1.11B

For reference:

• 10x = $740M (very conservative)

• 20x = $1.48B (still reasonable for this growth and margin)

4. So What Are You Actually Paying for the Bitcoin?

Enterprise Value: $2.51B

Less BIG value (15x): −$1.11B

Residual EV: $1.40B

BTC NAV (35,102 BTC x ~$68K): $2.39B

You’re buying 35,102 Bitcoin (worth $2.39B) for $1.40B. That’s a 41% discount to NAV. An implied BTC purchase price of ~$40K.

And we’ve only accounted for one business line. But there's more.

5. The Capital Markets Flywheel

This is a significant piece of value most people overlook entirely: their ability to leverage capital markets for accretive BTC accumulation.

When Metaplanet trades above 1x mNAV, every dollar of equity raised buys more than a dollar of BTC per share. That’s the flywheel that took Strategy from its first $250M purchase to 717K BTC. And took Metaplanet to >30K BTC.

What makes Metaplanet’s version potentially more powerful is that the BIG provides an operating income floor that supports the mNAV premium even in soft markets. If the business is worth $1.1B+ on its own, that justifies a structural premium to NAV — which makes equity issuance structurally accretive — which drives BTC per share higher — which supports a higher premium. It’s a self-reinforcing loop that the income business anchors.

This capital markets capability is worth billions of dollars. It's already generated billions for shareholders in <2 years. Between now end of next year, if they achieve their 210K BTC target and realize a BTC gain of 50% of that accumulation, we're looking at 87.5K BTC, worth $6B at today's prices. Let's take that as the valuation, and not assume anything else in the future.

6. The Perpetual Preferred Platform

This might be the most underappreciated piece of all, because it is not yet fully proven in Japan.

Mercury has already raised $150M via private placement at a 4.9% fixed yield. It’s pending TSE listing approval. Mars is also expeted to list simultaneously and grow organically from there.

Japan sits on ¥7.5 trillion in household savings earning ~0.5% at banks. Mercury yields 4.9% — nearly 10x that. So the potential demand pool is enormous.

Now let's think about how this scales with the BTC collateral base:

• Today at 35K BTC (~$2.4B NAV)

• At 100K BTC and $80K BTC price ($8B NAV): ~$2B in prefs keepign to the 25% NAV soft cap, though this can be revised up

• At 210K BTC and $100K BTC ($21B NAV): $5B+ in capacity

For context, Strategy raised $5.5B through preferred equity in 2025 alone. The preferred platform has arguably created billions in franchise value for $MSTR.

Metaplanet is building the same thing for Japan and potentially broader Asia — with a huge first mover advantage. Permanent, non-maturing leverage, without diluting common shareholders.

Near-term value (once listed, initial scale): $500M-$1B

Medium-term (as collateral base scales to 100K+ BTC): $1-3B

Long-term : $5B+ easily

So putting a reasonable value on it: $1-3B

7. Project Nova

Described as the “gateway to everything BTC in Japan.” Expected to encompass trading, lending, custody, and broader Bitcoin financial services for institutional clients.

Japan is the world’s third-largest economy. Institutional Bitcoin infrastructure there is practically nonexistent. Metaplanet has by far the leading BTC stack, the brand, the regulatory relationships, and the first-mover advantage.

Even at modest adoption, there could be significant revenue potential:

• $50-100M in annual revenue within 2-3 years is very reasonable

• At 8-12x revenue (high-growth fintech/financial services): $400M-$1.2B valuation

• Apply a 50-70% discount for pre-revenue/execution risk

Present option value: $200M-$500M

If it scales across Asia: multiples of that

8. The Media Arm

https://t.co/f1TVbDDOnk — premium digital real estate. Bitcoin Magazine Japan. The Conference.

Revenue potential at maturity: $15-45M annually. At 5-8x: $75-360M

Conservative present value: $50-200M

The Hotel — probably not much beyond the land value and some intangible community value. Let's say $20-50M.

9. SOTP Valuation

Bitcoin Income (15x OP): $1.1B

Capital Markets Flywheel: $6.0B (at least)

Total Current Business: $7.1B

Perpetual Preferred Platform: $2.0B

Project Nova: $350M

Media Arm: $125M

Hotel: $35M

Total Non-BTC Value (incl future business lines: $9.6B

BTC Holdings (35,102 BTC): $2.4B

Total SOTP (current business): $9.5B

Total SOTP (incl future business lines): $12.0B

Current EV: $2.5B

Implied upside to fair value: 278% (conservative) to 380%, not accounting for growth in BTC price.

10. What Are You Actually Paying Per Bitcoin?

This is where it gets interesting.

If the non-BTC businesses are worth what the conservative SOTP says ($7.1B), then:

$2.5B EV − $7.1B non-BTC value of current business only = -$4.6B

You’re not just getting the Bitcoin at a discount. You’re effectively being paid $4.6B to take 35,102 BTC off the market. That’s the equivalent of receiving Bitcoin at negative $131K per coin

Even if you haircut the non-BTC value aggressively, you still have a significant buffer. The market is giving you the Bitcoin and then some of their businesses all for free.

11. Closing Thought

My point here is not senseless bull posting, but rather to break things down factually and in a way that is devoid of sentiment and emotion. And always remember, the markets can stay irrational much longer than you can stay solvent. It wouldn't be the first or last time. But in Metaplanet, you have an exceptional team, with integrity I have rarely seen, going after one of the biggest opportunities for wealth transfer in modern history.

The opportunity is great — to put it mildly.

$MPJPY $MTPLF

Thank you to every Metaplanet shareholder. When we started this journey, we had a handful of believers. Today we have hundreds of thousands of shareholders around the world. That growth reflects trust, and we don't take it lightly for a single day.

This has not been an easy period. Bitcoin is volatile and anyone holding it needs to accept that truth. Bitcoin's fixed supply, growing global adoption, and unique properties as a store of value are why we are convicted. But conviction doesn't make drawdowns painless, and I want to acknowledge that honestly.

Our strategy remains unchanged. We exist to accumulate Bitcoin and grow Bitcoin per share, which we increased by over 500% in 2025. We will never sell our Bitcoin. Our derivatives strategy allows us to acquire Bitcoin at better prices than simply buying at spot, capitalizing on volatility in a sophisticated and risk-managed way, to the benefit of every shareholder.

On where Bitcoin goes from here: I personally believe Bitcoin may have found a floor around $60,000, though I hold that view with humility. Nobody knows. What I do know is that it doesn't change our strategy. Over the long term, I have no doubt Bitcoin will be dramatically higher than it is today. Irrespective of near term price, we will continue to accumulate, continue to grow Bitcoin per share, and continue to lean into income generation through derivatives as a core pillar of how we operate.

Short sellers, and critics of Bitcoin and Bitcoin treasury companies will always be loudest when prices are down. But that is rarely the right moment to abandon conviction. It is usually precisely the wrong moment.

The future is bright. Every decision we make, every day, is made with gratitude toward our shareholders and with one goal in mind: to reward those who believe in this strategy for the long term.

#Metaplanet released several disclosures today.

Here are the key items:

a) Completed the Mercury private placement: $135M raised ($150M notional)

b) Purchased 4,279 BTC at an average price of ~$105k

→ Q4 BTC yield: 11.9%

→ Total BTC holdings: 35,102 BTC

c) Q4 Bitcoin Income Generation (BIG) revenue up 74% QoQ to ~$27M

→ FY2025 BIG revenue: ~$55M

OK, so that's what we already know.. now what does it all mean?

1. Bitcoin Income Generation (BIG)

According to the Q3 financials, Oct 1 began with:

~$134M in BTC collateral (~1,175 BTC)

~$18M in cash & deposits

Source: https://t.co/05SJWuFAlt

Capital movements during Q4:

Oct 6: +$5M (20th Series MSWs)

Oct 14: −$5M EVO debt (partial redemption)

Oct 31: +$100M credit facility draw

Nov 21: +$130M credit facility draw

Dec 1: +$50M credit facility draw

Dec 29: −$19M EVO debt (full redemption)

Dec 29: +$135M Mercury placement

Dec 30: +$27M Q4 BIG income

Dec 30: −4,297 BTC transferred to treasury (acquired for ~$450M)

Net cash balance in BIG at end of Q4: ~$125M.

What does that imply?

→ Q4 BIG revenue: ~$27M

→ Collateral base:

Started at ~$152M

Peaked at ~$432M (excluding Dec 29–30 activity)

Estimated average collateral deployed: ~$295M

→ That implies:

~9% return for the quarter

~36% annualized return

Some important implications:

→ If no additional capital is raised in Q1, and they generate similar returns on the existing $125M, that alone implies ~$11.5M of revenue.

→ They still have ~$220M of undrawn credit capacity, which can be activated opportunistically.

→ This is not necessarily “recurring” income — since returns depend on collateral size and volatility.

At current levels, Q4 BIG revenue could theoretically support >$2B of preferred equity paying 5%, equivalent to >65% of current NAV.

That means the previously communicated 25% of NAV soft target is not really relevant. What will matter instead is dividend coverage.

→ Current amplification level: ~5%

2. BTC Treasury

Oct 1: 30,823 BTC

Q4 additions: +4,297 BTC

Dec 30: 35,102 BTC

Result:

BTC yield: 11.9%

Net BTC gain: 3,672 BTC

That implies:

Accretion rate: 3,672 / 4,297 = ~86%

Equivalent mNAV: ~7.1x

And to put things in perspective:

Adding 4.3k BTC in a single quarter for Metaplanet is roughly equivalent to MicroStrategy adding ~93k BTC, adjusted relative to their size.

3 .Closing Thought

These results were delivered during a quarter when:

BTC fell ~23%, and

mNAV compressed to ~1.0x (and briefly ~0.85x)

Despite that, Metaplanet expanded BTC per share >11%, delivered record options income +74% QoQ, and strengthened balance sheet optionality with the addition of new mNAV-agnostic tools.

All of this happened in adverse conditions.

Now imagine what Metaplanet can do with a supportive BTC backdrop and a re-expanding mNAV. There's a lot to look forward to in 2026, and despite the share price, the company has never been in a stronger position.

$MPJPY $MTPLF