@GrahamHaynes11@MPelletierCIO Not sure what your point is in bringing up “The market” I think the point is that many investors advocate for passive investing in the indexes and the exposure to the S&P 500 is significant.

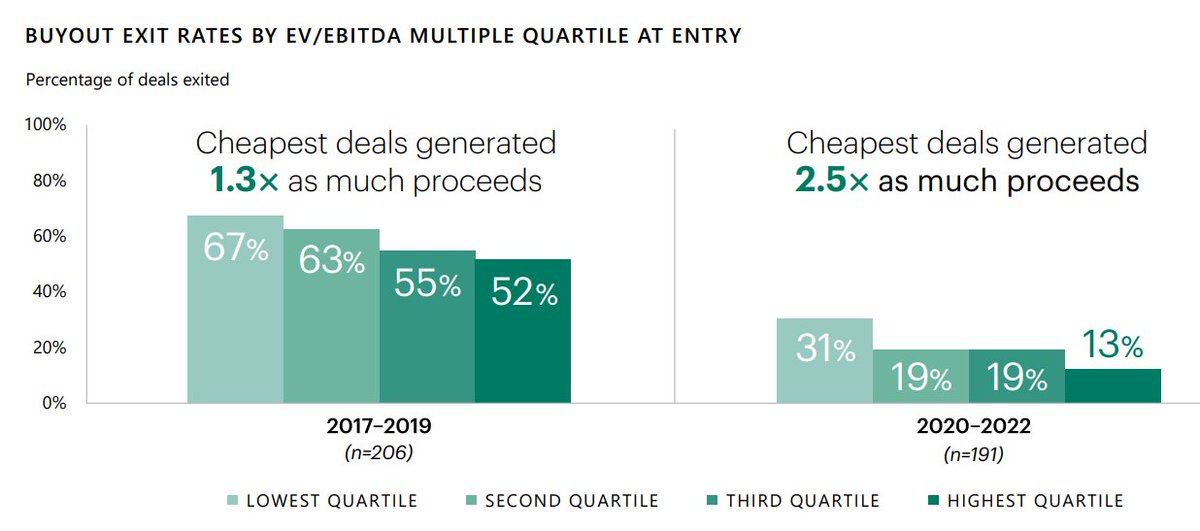

Some incredible data from Apollo highlighting the correlation between private equity returns and entry multiples paid for deals

The lowest multiple deals exited as much as 1.3x during the 2017 to 2019 period, and that outperformance has gone up to 2.5x since 2020

Turns out the best way to generate returns and proceeds for LPs is actually very simple and intuitive, even in private equity

Just buy low and sell high. Easier said than done.

Leatt $LEAT Q4 & FY 2025 results:

Q4:

▫️Revenues +43%

▫️Net income +204%

FY 2025:

▫️Revenues +41%

*International +47%

*Dealer direct +22%

*Customer direct +44%

▫️Net income +248%

▫️Double-digit revenue growth in all major product categories and sales channels

"Again, we are very enthusiastic about our future. With a growing portfolio of innovative products in the market and in the pipeline, a focus on elevating and amplifying our brand, and a robust balance sheet to fuel the growth, we remain confident that we are well-positioned for future growth and increasing shareholder value."

The Warsh-Treasury Accord - US government has a massive debt about $35 trillion, which is 121% of everything the country produces in a year (GDP).

The interest payments alone are $1 trillion/year, which is half the annual budget deficit. This is unsustainable.

So how do you deal with a debt you can't realistically pay back? You have three options:

Cut spending / raise taxes - politically impossible at this scale

Default - would blow up the global financial system

Inflate it away - make the debt worth less in real terms by letting inflation run hot while keeping interest rates artificially low

Option 3 is the plan, and Kevin Warsh (Trump's pick for next Fed Chair) is the guy who'll execute it.

What is Yield Curve Control (YCC)? Think of it with a simple example.

Imagine you lend me ₹100 at 8% interest. I owe you ₹8/year. Now imagine inflation is running at 12%. In real terms, I'm actually paying you negative 4% the money I pay you back buys less than what you lent me. I'm getting richer at your expense.

YCC is the mechanism to engineer exactly this at a national scale.

Here's how it works - The Fed announces, "We will not allow the 10-year Treasury yield to go above, say, 2.5%."

If the market tries to sell bonds (pushing yields up), the Fed steps in and buys unlimited quantities to force yields back down. It's a price ceiling on interest rates, enforced by the printing press.

Fed doesn't need to actually buy that much. If the market believes the Fed will defend the peg, nobody bothers fighting it.

It's like a currency peg - the credibility does most of the work. But if credibility breaks, it can get very ugly very fast (ask the Bank of Japan about 2022-23).

The Historical Parallel: 1942-1951

During WWII, the US needed to borrow enormous amounts. The Fed and Treasury made a deal (the 1942 Accord): the Fed would cap Treasury yields at 2.5% for long-term bonds and 0.375% for short-term bills.

This meant the government could borrow at rock-bottom rates regardless of how much it spent.

What happened after the war - Debt/GDP was 125% in 1946. Inflation ran hot - sometimes 15-20% in the late 1940s

But borrowing costs stayed pinned at 2.5%. Real interest rates were deeply negative for years. By 1980, debt/GDP had fallen to 30%

The debt didn't disappear. It was transferred from the government to savers and bondholders, who earned returns below inflation for decades. This is what economists call financial repression.

Why This Matters Now?

Step 1: US debt/GDP is 121% - almost exactly where it was post-WWII.

Step 2: Warsh has called for a new "Fed-Treasury Accord" literally reviving the framework that enabled financial repression last time.

Step 3: Trump attacked Powell for being too hawkish (rates too high). The idea he'd pick someone more hawkish was never credible. He wants lower rates to reduce government interest costs and boost the economy.

Step 4: If real rates go negative (inflation > nominal interest rates), the debt gradually melts away in real terms.

Step 5: The losers are anyone holding fixed-income assets denominated in dollars. The winners are holders of hard assets - gold, commodities, real estate, equities with pricing power.

Why Central Banks Are Buying Gold?

This is the crucial signal. If you're a foreign central bank (say China, India, Saudi Arabia) and you hold $500 billion in US Treasuries, and you see this playbook coming, what do you do? 😇😇

You sell Treasuries (which will be inflated away) and buy gold (which can't be printed). That's exactly what's been happening - central bank gold purchases have surged since 2022.

They're front-running the devaluation.

A few days ago, the US ambassador to India was sitting with the Indian RBI. What does that mean? Do you understand now?🙃

Every major debt crisis in history has been resolved through currency devaluation.

The US did it in 1933 (Roosevelt devalued the dollar vs gold by 40%), in 1971 (Nixon ended gold convertibility entirely), and it's happening again now through YCC.

The India Angle (Since This Matters for Everyone)

This has direct implications for your portfolio thinking. If the US pursues financial repression:

The dollar weakens over time in real terms → the rupee's recent weakness to 91-92 may actually reverse or stabilize as the dollar loses purchasing power

Gold in rupee terms benefits doubly, dollar gold rises AND if rupee stabilizes, you capture most of the move

Export-oriented Indian companies benefit from a world where the US is deliberately running loose monetary policy (more global liquidity)

US Treasuries become a terrible hold, exactly why you'd want to avoid dollar-denominated fixed income

A Contrarian View to Consider

Not everyone agrees this will play out smoothly. The 1942-1951 period had unique conditions: the US was the world's dominant creditor nation post-war, the dollar had no real competitor, and capital controls were widespread.

Today:

Capital is globally mobile, investors can flee to other currencies/assets much faster

The dollar faces nascent competition (gold, potentially other reserve alternatives)

Inflation expectations are much more "unanchored" people are inflation-aware in a way 1940s Americans weren't

If the market sniffs out YCC, it could front-run it, causing a bond market dislocation before the policy is even implemented

So the thesis could be right directionally but the transition could be far more volatile than the smooth 1945-1980 grind.

If the Fed implements YCC and pins the 10-year yield at 3%, but inflation is running at 6%, what is the real return to a bondholder?

And why does this specific dynamic reduce debt/GDP over time, think about what happens to the numerator (debt in nominal terms) vs the denominator (GDP in nominal terms) when inflation is running hot but interest costs are capped>?

@EugeneNg Thanks for the thoughtful reply…#1 is really interesting to me. It maybe the most difficult to evaluate or measure, but to your point perhaps the most important to consider