The APR looks great. But who actually holds the assets?

What's the legal structure if they fail? What are the withdrawal terms under stress?

Most fintech teams building stablecoin yield products haven't fully stress-tested those questions. We broke down the five risks that matter most before integrating stablecoin yield into your existing product.

Read the full article below 👇

1/ Stablecoin adoption in Latin America has moved well beyond a single use case. The early wave was freelance and retail savers protecting purchasing power, followed by a re-plumbing of remittances, and then came enterprise payroll and treasury.

Global B2B stablecoin payment volumes surged 30x in 2 years, and the use case driving that growth now span the full spectrum of financial services activity across the region.

1/ The best yield isn’t tied to one product. It's the one matched to each customer’s risk, return, and liquidity needs.

A neobank protecting consumer savings and an asset manager optimizing for return need different things from the same dollar.

OpenTrade gives fintechs the full range of yield sources to choose from, Money Market Funds, Bonds, ETFs, Private Credit, CLOs, Delta neutral strategies, Staking, DeFi LP, along with the tools to combine and tailor them into exactly the product their users need.

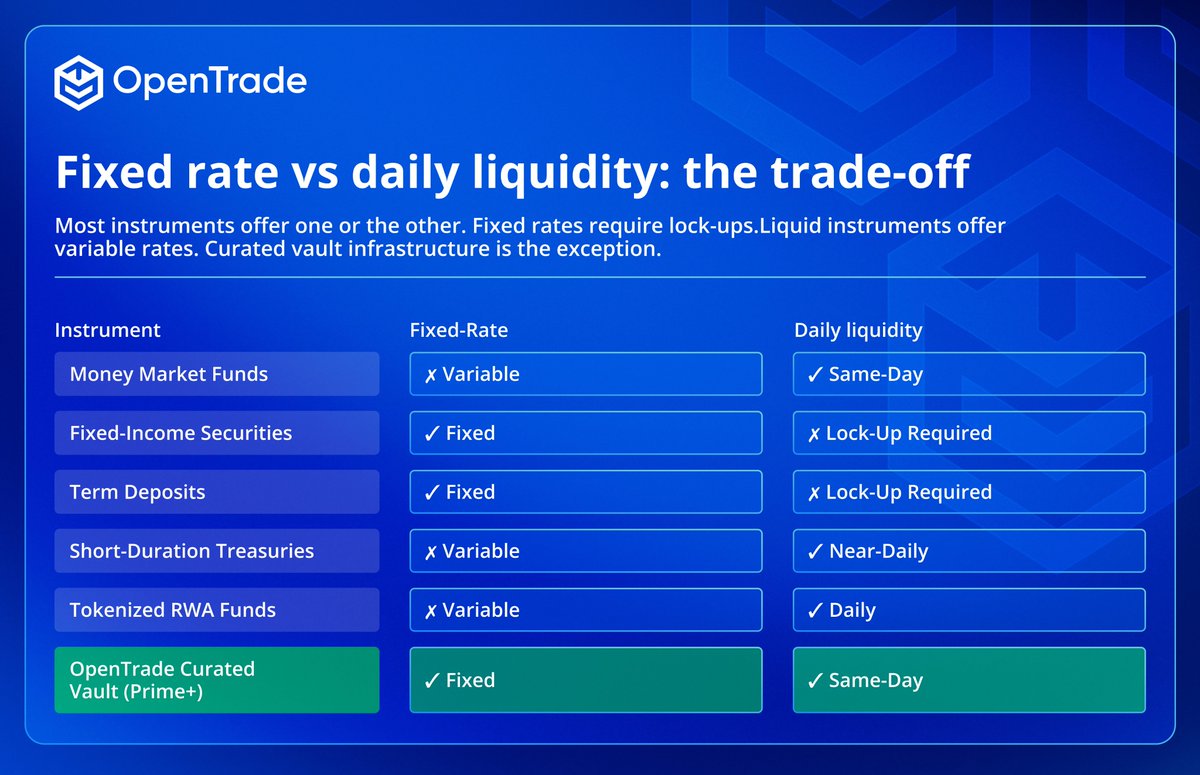

1/ Most neobanks offering stablecoin yield face the same problem: no fixed rate without an investment team to manage the exposure, no daily liquidity without giving up the fixed rate entirely

So they either offer a variable rate that changes every quarter and frustrates users, or they lock balances in and watch adoption suffer

1/ Some clients need yield built around their requirements, and a pre-made vault won't get them there

Curation+ is OpenTrade's bespoke vault design and treasury management service: every vault is scoped to the client's own collateral, risk, and liquidity needs

4/ For exchanges accumulating stablecoin float between on-ramp and off-ramp settlement, that capital doesn't have to sit idle. It can be earning institutional-grade yield through OpenTrade while it waits.

Read our full article on stablecoin FX here👇

https://t.co/NQigfEngvM

1/ Stablecoin yield is becoming a standard product feature for neobanks and exchanges. The platforms offering it are pulling ahead on acquisition and retention. The ones that aren't are starting to feel that gap

1/ Small to medium-sized businesses in Latin America face a specific set of financial problems that traditional banking has never adequately solved.

Opening a USD account through a local bank is effectively impossible for SMEs in the region. Cross-border payments absorb 10-20% in fees, and payment delays are common. Currency devaluation in Colombia, Brazil and Mexico erodes margins every month. An SME operating across Mexico, Brazil, and Argentina manages three currencies, three regulatory regimes, and a 3-5 day settlement lag on every cross-border transaction. 🧵

1/ $540M+ in transaction volume in the past 12 months. $235M+ in assets deployed. 99.9% uptime with full on-chain transparency.

Here's what fintechs around the world are building with OpenTrade 🧵

1/ May marked a defining inflection point for OpenTrade - a month in which multiple milestones converged at once, signalling a step-change in scale, visibility, and market validation.

Here's what happened 👇

We raised $17M, published our LATAM Stablecoin Surge Report, brought the story to Consensus Miami, and kept the momentum going on the Money Moves podcast.

1/ $324 billion in stablecoin transactions across LATAM in 2025. Up 89% year-on-year.

Traditional remittance services charge up to 10% per transfer and take days to settle. Stablecoins cut that cost by up to 90% and settle in seconds

Our CEO @BTC_Dave joined @TheBlock to break down why stablecoins are the killer crypto application, why emerging markets are where the most important use cases are being built first, and why offering yield in a way that is scalable, compliant, and programmable is harder than it looks.

Most financial infrastructure forces a choice: build inside a regulated, permissioned system with legal recourse, or build on open, permissionless rails that anyone can access, but nobody controls.

Neither extreme works on its own. The model that has actually scaled is a hybrid of both.

OpenTrade Co-Founder and CEO @BTC_Dave and @eppy314 swap sides on purpose in Episode 7 of @Money_Moves_Pod, with @sjolewis, and reach the joint conclusion that the hybrid model is the one that scales, creates network effects, and drives adoption.

1/ If you are a producer in Brazil exporting goods, traditional banking spreads eat into your margins on every transaction.

Cross-border payments absorb fees at each intermediary stop. Currency volatility adds another layer of risk on top.

Stablecoin rails remove all of it. Near instant settlements. Near-zero cost. Dollar-denominated from end to end.

The technology exists today to make that possible for any business, regardless of size or location.

What Felipe Galvis describes is not a distant vision. The infrastructure is being built now. What remains is putting it in the hands of the people who need it most.