The Holy Trinity is dead. Sadly due to the Orchard Pool exploit, I had to dump our entire $ZEC bag.

- While I think it's extremely unlikely of any minting, it cannot be formally cryptographically proved impossible

- The privacy from AI, govt, big tech narrative demands perfection not improbability

- I read about the exploit yday, and didn't appreciate how it violated my narrative mental map. The 30% dump, made me rethink, and I had to take profit on the entire position

- We will consistently re-evaluate our thinking and if my assumptions are proven incorrect, will rebuy, hopefully at lower prices.

- Privacy is priceless and I have no issue eating humble pie and rebuying much higher.

We still hold $WLD and are excited for Lord Elon to pump our bags.

@ArtofConviction Too bad they’re leading subnets don’t agree

Interesting yes, but most subnets are unprofitable without Tao emmisions as far as I can tell

crypto is best market ever

- savage beyond words

- insane ups and downs

- crazy characters

- we do in cycles in 8 years what the stockmarket does in 100 years

- i can be a psychologist to 50.000+ people with profound existential problems

why would you wanna be somewhere else?

i find it very entertaining to be honest

Cosmos Labs is acquiring the @mintscanio product suite and welcoming select Mintscan personnel to the Cosmos Labs Ecosystem team.

This business expansion adds new team members to the Ecosystem team across product, engineering, and operations.

It also allocates dedicated resources to the Cosmos Hub and key ecosystem infrastructure to support reliability and growth.

https://t.co/FEiE9rRw6M

I joined Cosmos Labs last year because they were already building towards a paradigm shift in blockchain that I knew was about to take over the space. Enterprise adoption of blockchain represents our first real chance at bringing the industry into the mainstream, and the Cosmos Stack continues to be the best solution on the market for making that happen.

That bet is paying off. The Cosmos stack and IBC have quietly become the home for a growing number of the most successful enterprise-specific blockchains in the space, and the value settling across them is climbing. The market is finally catching up to what this ecosystem has understood for years, and it’s all because resources were allocated to making that happen at an opportune time.

Now it’s the Hub’s turn to have substantial resources allocated to building out our place in a growing market segment of opportunities around interoperability, enterprise finance, and RWA markets. To facilitate this, we’ve acquired the Mintscan product suite and hired a large portion of the team to accelerate development on the Cosmos Hub and public goods for the ecosystem.

A few weeks ago I wrote on the forum that the Hub is moving through three phases: from chaos, into stability, and toward growth. I said that getting there would require growing the team dedicated to the Hub and stabilizing the critical infrastructure upon which this ecosystem relies (Mintscan, Skip:Go, Eureka, and much more).

Bringing on @yongjoojung , @gyunit_ , and the rest of the team crosses both of these items off of the list. They bring some of the deepest and longest-running experience with the Cosmos stack and its infrastructure that exists anywhere to the Cosmos Labs ecosystem team. I have had the pleasure of working alongside them in one capacity or another across my six years in this ecosystem, and there is no group I would rather have in the room as we take on this next phase.

With them joining the ecosystem unit, the Cosmos Hub and the ecosystem around it finally have their dream team. The team will begin onboarding over the coming weeks so that we can prepare to lay the groundwork for the Cosmos Hub’s roadmap and the core primitives we’ll need to achieve it.

Ethereum is one of the most misunderstood assets because it is the most miscategorized. Depending on the day, the market keeps trying to price ETH as a currency, a tech stock, a bet on transaction fees, or a Bitcoin follower, and on every one of those frames, it looks overvalued or underwhelming.

History has a habit of repeating itself whenever a new foundational technology emerges. Before society fully understands its significance, the technology is often dismissed, undervalued, misunderstood, and judged by the wrong metrics. The Internet followed this pattern. Blockchain, and especially Ethereum, is following it today.

In the 1980s and early 1990s, the Internet was widely viewed as an academic curiosity rather than a commercial opportunity. Its users were primarily researchers, government agencies, military institutions, and hobbyists. To the average person, it appeared complicated, slow, and irrelevant. Major newspapers questioned why anyone would want to read news on a computer screen rather than in print. AT&T reportedly passed on opportunities related to ARPANET because it saw little commercial future in the technology.

Even prominent thinkers failed to grasp its potential. In 1995, Clifford Stoll famously argued that online commerce, digital communities, and electronic publishing were largely fantasies. Three years later, economist Paul Krugman predicted that the Internet's economic impact would prove no greater than that of the fax machine.

Their mistake was not a lack of intelligence. It was a failure to recognize that foundational infrastructure creates value indirectly before it creates value directly.

The Internet was initially evaluated as a product. In reality, it was becoming a platform. It was not merely another communications tool; it was a new coordination layer for society. It would eventually become the foundation upon which entirely new industries, business models, and forms of human interaction could emerge.

The same misunderstanding exists today with blockchain networks.

Many observers evaluate blockchains as if they were standalone applications. They ask how much revenue they generate, how many fees users pay, or whether transaction costs are rising or falling. These questions are useful, but they often miss the larger picture.

Ethereum is not primarily an application. It is infrastructure.

Just as the Internet created a global network for the exchange of information, Ethereum creates a global network for the exchange of value, ownership, trust, and programmable agreements. It provides a neutral settlement layer upon which thousands of applications, protocols, financial products, stablecoins, tokenized assets, and digital organizations can operate.

The Internet's most important value did not reside within TCP/IP, HTTP, or email protocols themselves. Its value emerged from what others built on top of those standards. Amazon, Google, Facebook, Netflix, Shopify, and countless other companies captured enormous economic value because the Internet provided an open platform for innovation.

Ethereum operates according to the same principle.

Its value is not limited to transaction fees. It derives from securing trillions of dollars in future economic activity, enabling decentralized financial markets, supporting stablecoin ecosystems, facilitating tokenized real-world assets, and serving as the trust infrastructure for a new digital economy.

The Internet also experienced its own cycle of misunderstanding. The dot-com boom correctly identified the technology's importance but wildly overestimated the short-term value of many companies built upon it. The subsequent crash led critics to declare the Internet overhyped and disappointing.

Yet the crash did not invalidate the technology. It merely removed speculation while leaving behind critical infrastructure. Fiber-optic networks, data centers, software tools, and developer talent continued to improve. The result was the emergence of Web 2.0, cloud computing, social media, and eventually the modern digital economy.

Today, many governments worldwide have officially reclassified broadband internet as a critical public utility, on par with water and electricity. The digital economy now accounts for over 15% of global GDP, driving exponential growth in visual and financial markets. The COVID-19 pandemic permanently proved that the global economy could not function or survive without internet infrastructure.

Blockchain is experiencing a similar phase today. Speculative excesses have obscured genuine innovation. Failed projects have led critics to dismiss the entire sector. Yet beneath the surface, the infrastructure continues to mature. Scalability is improving. Security is strengthening. Stablecoins are growing rapidly. Tokenization is accelerating. Institutional adoption is increasing.

The market's challenge is that infrastructure is difficult to value before its full utility becomes obvious.

Few people in 1995 could imagine that the Internet would become essential to commerce, communication, entertainment, education, and work. Today, global society would struggle to function without it.

Likewise, many people still view Ethereum as a niche technology for traders, speculators, or technologists. But if blockchain becomes the trust layer for global finance, digital identity, asset ownership, and machine-to-machine commerce, then today's valuations may ultimately look as shortsighted as the skepticism once directed toward the Internet.

The lesson of history is simple: transformational infrastructure is rarely understood in real time. The Internet was underestimated because people measured what it was rather than what it could become. Ethereum faces the same challenge today. Its greatest value lies not in the activity we can already see, but in the vast economic and social systems it may eventually support.

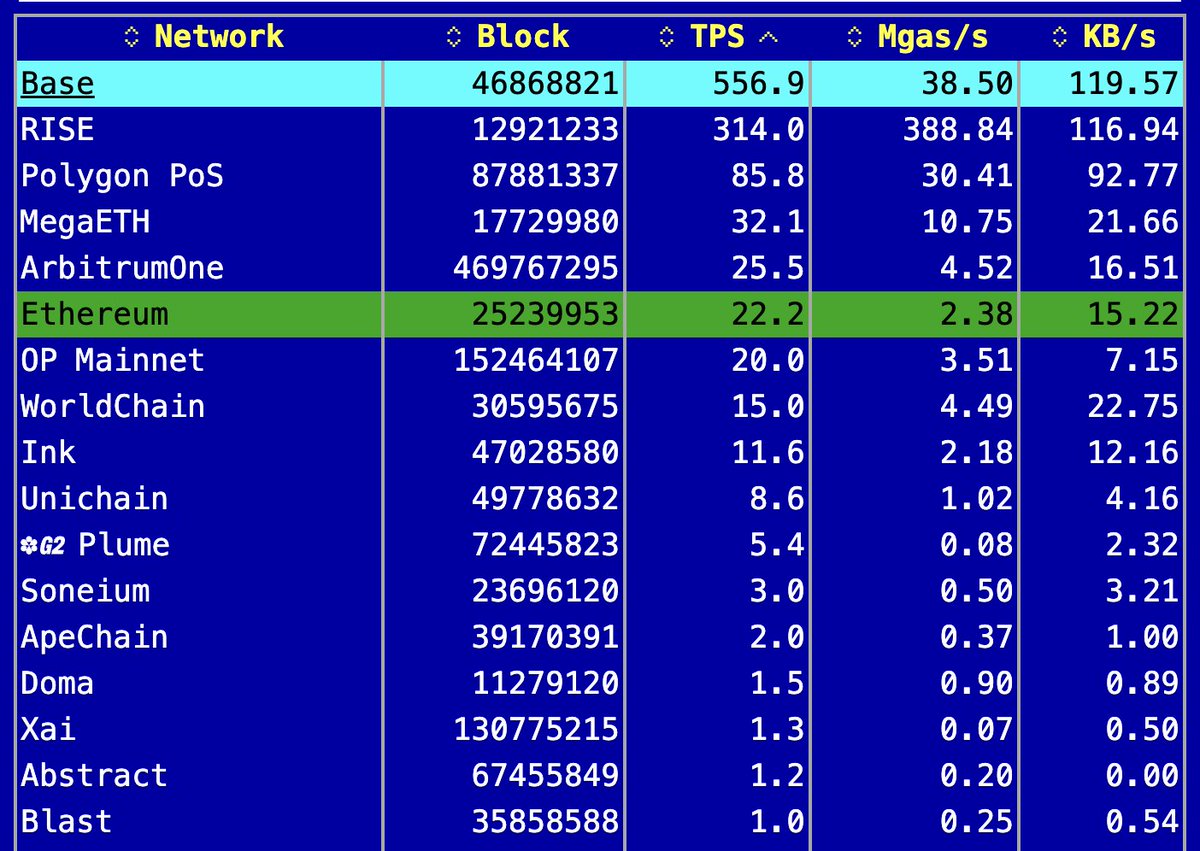

nice to see @base cruising at 550 TPS

the chain can now burst up to 5K TPS, with a bunch more headroom coming in the months ahead now that we're on our own stack post-Azul

team has been doing an incredible job scaling

2/6) The core breakthrough seems to be a technique they wrote a paper on a few months ago: Residual Bottleneck Model (ResBM, arXiv:2604.11947)

The fix is to compress what gets sent across each boundary. ResBM adds a compression layer at each handoff point that squeezes the data 128x before it crosses the internet, then decompresses it on the other side, cutting a large activation transfer down by two orders of magnitude.

Just orchestrated a 128 node permissionless decentralized training run, in 5 minutes, for 5 TAO, via @IOTA_SN9

They can do this up to 100B param models.

Unbelievable.

https://t.co/hJGZ6O5NrU

@MikeIppolito_ BTC.D trended upwards for the entire cycle. Most revenue generating crypto apps barely went up (in crypto terms.)

Could be btc.d crashes and the applications have their moment

Thanks for sharing!

My point is that long-term holders are trending higher. Even if we exclude the 6m to 1y cohort, which includes some Coinbase noise, the trend still looks clear.

I think the bear market may have a few more months left. It could last until late this year or early next year, imo.

@griffey247_7@BittBurger@AshCrypto Remember LaserDisc? It was supposed to be the next big thing after VHS but it was a flop and the world moved to DVDs and later Blu Ray. And now we rarely use either and simply stream everything. Bitcoin is LaserDisc.

We're finally shedding the .so (thank you Somalia!), and using the .com for @NotionHQ. And for this beautiful moment, I want to share a fun story:

Back in 2018, I had just joined Notion, and one of the first things @ivan asked me to do was figure out how we could own https://t.co/BxoFvc83VG. I had never done a big domain purchase before, so I reached out to a few domain brokers to understand the landscape. We tried different brokers, kept things anonymous, and attempted to surface a price the seller might consider.

A year went by… nothing. Meanwhile, it was pretty clear this was only going to get more expensive as we grew. We needed a different approach. A fellow founder connected me to a broker who took a very different tack. Less transactional, more long-term relationship builder. He spent months getting to know the domain owner. Turns out owner was a fellow entrepreneur in the west coast… and a huge Grateful Dead fan.

So we figured, why not get creative? Something beyond just price. So I called up our investor Ronny Conway and asked if there was any way he could help set up a private meeting between the domain owner and the Grateful Dead. Ronny is one of those people who somehow makes impossible things possible. A week later he calls me back: “New York City. Halloween. 15 minutes after the concert. Done.”

The broker went back to the owner with an offer: some cash, some equity, and a private meeting with the Grateful Dead. That got his attention. He didn’t take the band meeting in the end, but he did lean into the equity (great call, in hindsight). We shook hands, and a few weeks later, the deal was done.

I’ve been waiting years for the day we move our product to https://t.co/BxoFvc83VG. Looks like 2026 is finally the year. Safe to say I’m unreasonably excited about this update!

the first time i visited Anthropic it was a 160-person start-up in Jackson Square with no products and no revenue. there was an office throne made of empty Liquid Death cans and everyone seemed vaguely allergic to making money.

that was THREE YEARS AGO.

now they're going to go public at $400 quadrillion and bring about the teleological end of capitalism. what a world.

Something I cannot quite understand

Why people take losing trades personally

The markets don't know you. They have no idea who you are. They could care less what your hopes, fears and aspirations are. The markets are totally cold. Unfeeling

So why take a losing trade personally

Probably because you have misplaced assumptions and expectations. You assume the market cares about you enough to offer a profit. Your expectations are falsely placed

When I enter a trade I expect it to be a loser. I assume it will be a loser. This way I take risk management seriously

I know my trading stats. Over 200 trades I can come within a 10% on my estimate of ROR, win rate, PF, etc

But on any given trade or series of trades I do not have a clue. I may think I know where a market is going, but in reality I have no idea

So why would I take a loss personally. A trade is nothing more than a datum point in a series of data points subject to random probability theory. A loss is not a personal indictment