Hidden fees suck, especially when two cards look similar until you actually use them.

Here's the list ranked by extra cost vs the best observed rate, based on experiments from @0xVishnya ↓

Highest

@oobit | ~5.4%

@KASTxyz | ~2.7%–3.3%

Medium

@Plasma | ~1.8%

@RedotPay | ~1.5%

@wirexapp | ~1.4%

@xplaceapp | ~1.0%

Lowest

@useTria | ~0.6%

@krak | ~0.1%

@coca_card | ~0.0%

@avici | ~0.0%

@ether_fi | ~0.0%

You can also use https://t.co/hrGMfpX1BA as a go-to tool for checking whether a specific crypto card is available in your country, anon ;)

HOW DOES THIS QUANT BOT PRINT $10,561 IN PROFIT PER DAY

+$401,307 PnL in one month on Polymarket

Only on short crypto “Up or Down” markets

On Feb 16, this wallet switched to a market-making style using Bayesian + Kelly + Stoikov pricing rule

P(H|D) = P(D|H) · P(H) / P(D)

Bayesian is used to update the bot’s internal probability faster than the market updates its odds

Wallet using this model:https://t.co/pP89HqvPrm

r = s - qγσ²(T - t) - Stoikov is used to manage quoting and inventory risk

f = (bp - q) / b* - Kelly is used to size the position

This is why an arbitrage bot is not just “buying both sides”. It is a stack of models that mathematically estimates edge, sizes positions, and manages risk in real time

This is how these formulas work:

$4,508.76 → $11,293.72 (+150.48%)

$3,043.75 → $9,212.02 (+202.65%)

$6,695.96 → $12,473.57 (+86.28%)

Claude tells me: this is the basic set of every arbitrage strategy

OMG...

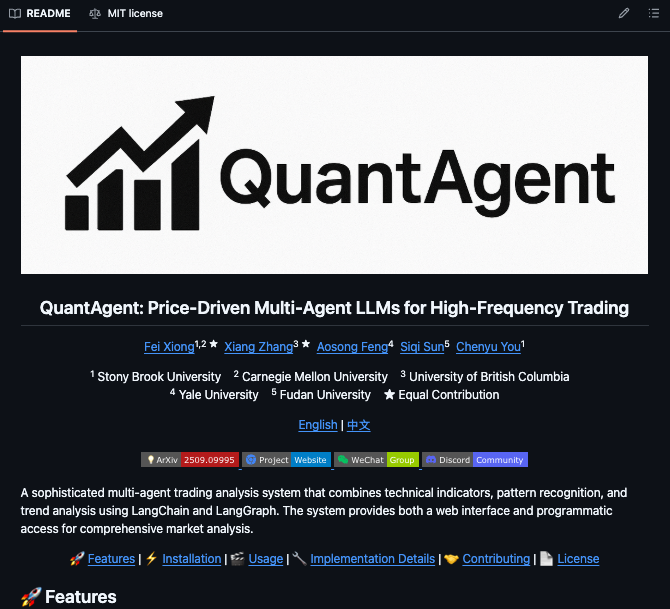

Researchers from Stony Brook, CMU, Yale, UBC, and Fudan just open-sourced a multi-agent LLM system built specifically for high-frequency trading analysis.

It's called QuantAgent and it runs four specialized AI agents simultaneously each analyzing a different dimension of the market then synthesizes everything into a single actionable trade decision with entry points, exit points, and stop-loss thresholds.

Link in the comments + details about this 👇

เห็นฝรั่งแชร์เว็บนี้

https://t.co/zIfIhYV3Ln

เลยเข้าไปดูตามเขา ก็ไม่เลวนะ

ผมชอบ bull flag กับ power earning gap

แต่เปิดให้ดูฟรีๆ ไม่เยอะเท่าไหร่

finviz จึงยังคงเป็นเพื่อนดีของสายฟรีต่อไป

Just tracked a highly suspicious group of 10 Polymarket wallets

They're trying to stay under the radar by splitting into small positions, but I caught their pattern

- All in on YES for US x Iran ceasefire by Mar 31/Apr 15

- $7K to $24K in positions per wallet

- 99% of positions were bought with market orders

- Combined size: $160K

- Payout if a ceasefire hits by EOM: +$1.04M

2 of these exact wallets previously bet YES on the US striking Iran before Feb 28 and cashed out $135k

This accumulation is still happening as of today

Someone is building a massive position under the radar

Hard to believe these are just random users

🧵Certain pockets continue to not care about the broader market at all. Focus on those and ignore the rest. Some examples below. See if buyers can step in with follow through in the coming weeks, which would help other things broaden out.

BlenderMCP connects Blender to Claude AI through the Model Context Protocol (MCP).

> Enables prompt assisted 3D modeling:

Blender just became programmable by language.

It connects Blender directly to Claude via the Model Context Protocol. Forget UI tricks and exports…

Claude can inspect, modify, and build scenes inside Blender.

• Prompt-based 3D modeling and scene editing

• Direct object, material, and camera control

• Scene inspection and reasoning

• Executing Python in Blender from an LLM

• Pulling assets from Sketchfab and Poly Haven

• Generating meshes via Hyper3D

“AI-assisted rendering.”? Nope.

Language → intent → geometry → code → scene.

For anyone working in robotics, simulation, digital twins, or 3D content pipelines, this points to a future where environments are described, not manually built.

Important note

There is no official website.

Only the GitHub repo is real. Anything else is unofficial.

Open-source, experimental. Use carefully.

Credit: @sidahuj

📍GitHub:

https://t.co/AnSe2c5nNG

[bookmark for later]

——

Weekly robotics and AI insights.

Subscribe free: https://t.co/dsa6wcvq6n

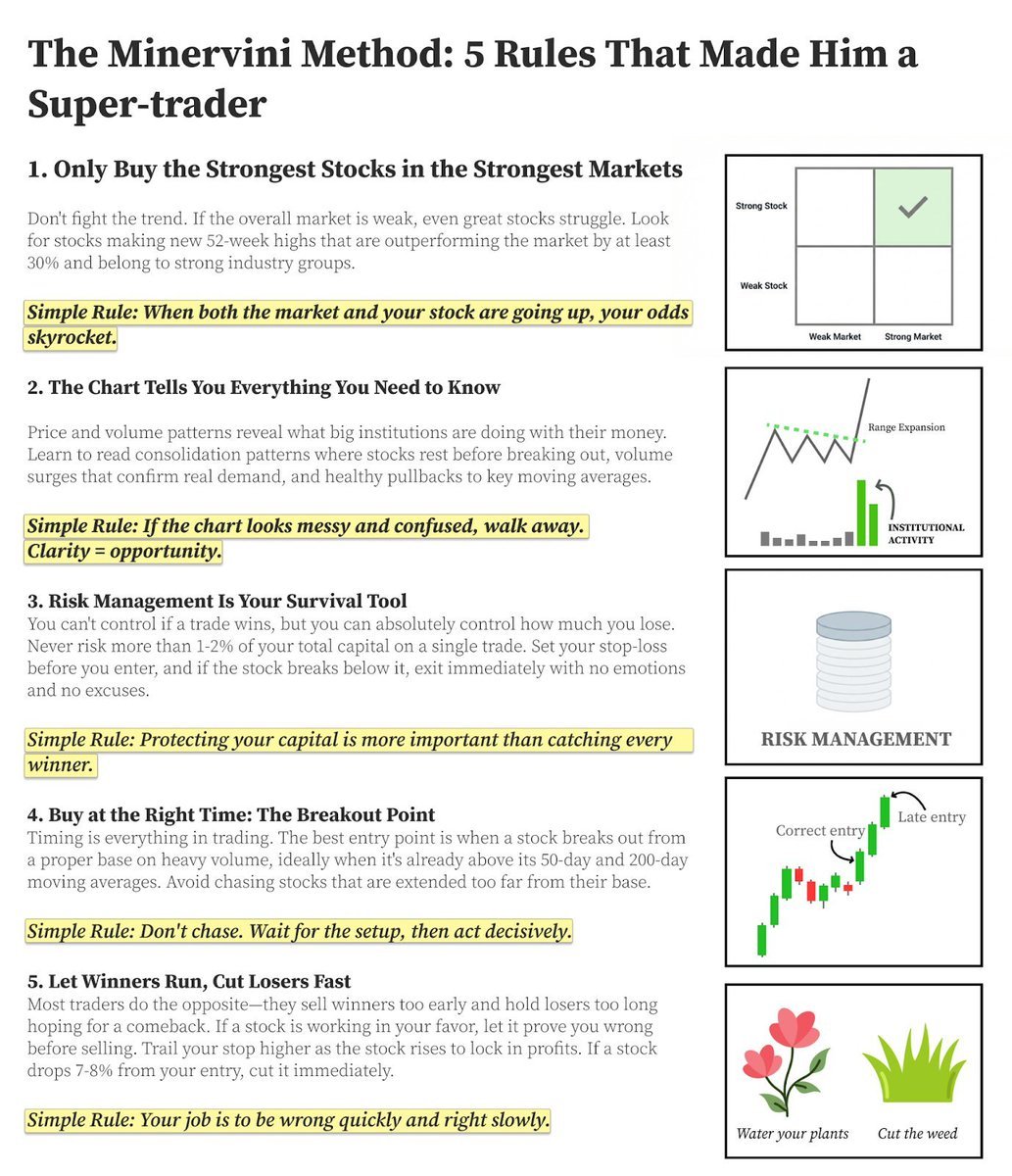

Mark Minervini turned $250,000 into $2.7 million in 15 months by following 5 Simple rules.

Most traders lose money because they break these rules.

This one-pager breaks down the exact framework that separates winning traders from everyone else.

#Trading

BREAKING: AI can now analyze stocks like Wall Street analysts (for free).

Here are 10 insane Claude prompts that replace $2,000/month Bloomberg terminals (Save for later)

The upcoming Market Wizards book is approaching completion. As such, @jackschwager and I have decided to release the names of the traders included in the book and their associated X handles. Here they are:

Kristjan Kullamägi @Qullamaggie

Lance Breitstein @TheOneLanceB

Simon Russo @simonrusso__

Lukas Fröhlich @TheShortBear

Phil Goedeker @Tradestl

Kelvin Chiu @KC_SilverCape

Jason Berry @Positive_Equity

Kenny Sharkness of @smbcapital (Kenny has no public X account)

Rick Bandazian Jr. @Off_The_Tape

Looking forward to sharing the book with the world!

If you'd like to pre-order the book, you can do so here: https://t.co/yJ9wjrw9Pp

For discounted bulk orders (US only) go here: https://t.co/gJoKIF2dr5

This was the highest volume day on $IBIT, ever, by a factor of nearly 2x, trading $10.7B today. Additionally, roughly $900M in options premiums were traded today, also the highest ever for IBIT. Given these facts and the way $BTC and $SOL traded down in lockstep today (normally SOL trades with beta) + the relatively lower liquidations on CeFi exchanges, this leads me to believe that the nexus of the problem lies with a large IBIT holder. IBIT has become the #1 venue for BTC options trading, so my guess is that a hedge fund trading IBIT options is the culprit.

If you look at the 13F filings for IBIT (I like whalewisdom dot com), you'll find a number of interesting names that have the majority of their fund in IBIT. In fact, there are a few in there (not naming names) that have 100% of their fund in IBIT, which likely means no cross margin. In fact, the biggest reason to set up a fund to hold a single asset would be to isolate margin, so that if the trade blew up, the brokers wouldn't have claim to any other assets.

Interestingly, most of these giant, single asset funds are based in HK.

We know that Asian traders, particularly in China, have been deeply involved in the Silver and Gold trade. Silver was down 20% today, which was the 2nd largest 1 day move in a very long time (largest on Jan 30). We also know that the JPY carry trade has been unwinding at an increasingly rapid pace.

This leads me to think that the culprit for the IBIT blowup today was 1 or more HK-based non-crypto hedge funds. As @FranklinBi pointed out, the fund(s) being non-crypto would explain why no one sniffed them out. They would likely have few/no crypto counterparties, meaning complete isolation from CT.

The last small piece of evidence I have is that I personally know a number of HK-based hedge funds that are holders of $DFDV, which had the worst single down day ever, with a meaningful mNAV decline. The mNAV had been holding steady surprisingly well throughout this pull back until today. One of these fund(s) could have been connected to the IBIT culprit, as I highly doubt a fund taking that large of a position in IBIT and using a single entity structure would only have the one fund.

Now, I could easily see how the fund(s) could have been running a levered options trade on IBIT (think way OTM calls = ultra high gamma) with borrowed capital in JPY. Oct 10th could very well have blown a hole in their balance sheet, that they tried to win back by adding leverage waiting for the "obvious" rebound. As that led to increased losses, coupled with increased funding costs in JPY, I could see how the fund(s) would have gotten more desperate and hopped on the Silver trade. When that blew up, things got dire and this last push in BTC finished them off.

I have no hard evidence here, just some hunches and bread crumbs, but it does seem very plausible. Let's see if some more concrete evidence floats to the surface here soon. The smoking gun will be a large fund fitting this profile filing a 13F showing a giant IBIT holding going to zero. Unfortunately, if a fund had their IBIT position liquidated today, they wouldn't have to disclose the position change until 45 days after the quarter end, so we'd be looking at mid May for the smoking gun from 13F filings most likely.

Hopefully some of you out there with too much time on your hands this weekend can snoop around more. My guess is that word will start to get out, because something of this size is just too hard to hide. Additionally, if the broker was not able to liquidate the fund in time, the broker may have a hole in their balance sheet, which would be even more difficult to hide.