The banking lobby has officially declared its opposition to the Clarity Act.

JPMorgan CEO Jamie Dimon went on national television this week and promised to fight the bill: "The banks will not accept it."

Here's what's at stake and what you can do about it. 🧵👇

Fat Protocol Thesis RIP. Fat App Thesis emerges, and where do agents fit in wrt value capture? Great questions for the crypto investor to monitor. We debate this a lot internally @bcap. TY @jonah_b , @CremeDeLaCrypto and the entire investment team!

Seeing blockchain fees as "extractive" is the wrong mindset imo.

Fees pay for the security of the chain.

In a proof-of-stake system, the network is secured by the value of the native asset. For Ethereum the network to be valuable, ETH the token has to be valuable too.

There's a negative feedback loop here: if ETH's value declines, security weakens, which erodes the utility of using Ethereum, which further erodes ETH, and so on.

For the token to hold value, you have two options:

1. Seigniorage. But L2s are incentivized to push stablecoins for UX reasons, and most people in trading and DeFi now denominate in stables rather than ETH. Combined with ETH's lackluster price performance and other chains taking market share, fewer people view ETH as a safe monetary asset.

2. Fee capture. Fees are burned and deflate ETH supply, accruing value back to the underlying asset.

Folks can hope ETH remains a monetary asset, but day by day, as other chains chip away at that narrative, the hope gets harder to hold. So fees matter bec they protect the value of ETH, which in turn protects the chain itself.

When you buy a pair of shoes with a credit card, the merchant often doesn’t actually receive final settlement for days, sometimes longer. Part of the reason is consumer protection: there’s a window for chargebacks, refunds, fraud checks, and disputes in case the shoes never arrive.

But internet-native goods, especially data & APIs are different. Delivery is instantaneous and verifiable. If an AI agent buys data online, the product is received immediately, so the traditional delay between authorization and settlement makes less sense.

That’s where stablecoins become interesting. They enable instant, final settlement for digital commerce in a way legacy card rails weren’t designed for.

The onchain economy needs both open innovation and deep capital

The question is how you get both when the properties that make the environment great for building also make it harder for large allocators to underwrite (!)

I think there's a market structure that emerges which actually solves for this. Wrote about it here

The cost of financial intermediation in the US hasn’t changed meaningfully since the 1880s

Now, blockchains and AI are finally letting software eat the plumbing

Finance history will look back at the 2020s as the decade when a new, cheaper, and far more powerful stack was born

For the entire history of crypto, the three biggest pools of capital in the world ($19T in bank deposits, $38T in treasuries, $100T in equities) were walled off from the onchain economy

In the last 12-18 months, all three got direct pipelines. And some of the institutions that were standing in the way are now the ones leaning in to build those pipelines

New post on what just changed and why it matters

As a former hedge fund manager - I agree. The public markets are far less forgiving than late stage private equity. They will be a public company very soon. But watching @carlosdomingo over a 10 yr period, leading their seed and A rounds, and @bcap being @Securitize ‘s first customer. I wud not bet against him!

BREAKING: @Securitize, @jumptrading, and @JupiterExchange launch fully onchain, regulated trading for tokenized equities on Solana. Real shares, not synthetics. Full legal ownership. SEC-registered broker-dealer and transfer agent backing every trade.

Payward (@krakenfx parent company) has been steadily amassing a massive range of products

Kraken - global exchange

xStocks - tokenised equities

Ninja Trader - futures trading platform

Breakout - prop trading platform

CF Benchmarks - crypto indices

Reap - stablecoins for cross border & B2B (announced today)

no one can argue Kraken is just a crypto exchange anymore

The financial system agents need is already here: it's onchain.

@Anchorage's Agentic Banking shows how infra can be designed to give AI systems compliant settlement and access to capital, helping agents operate inside the financial system, not outside of it.

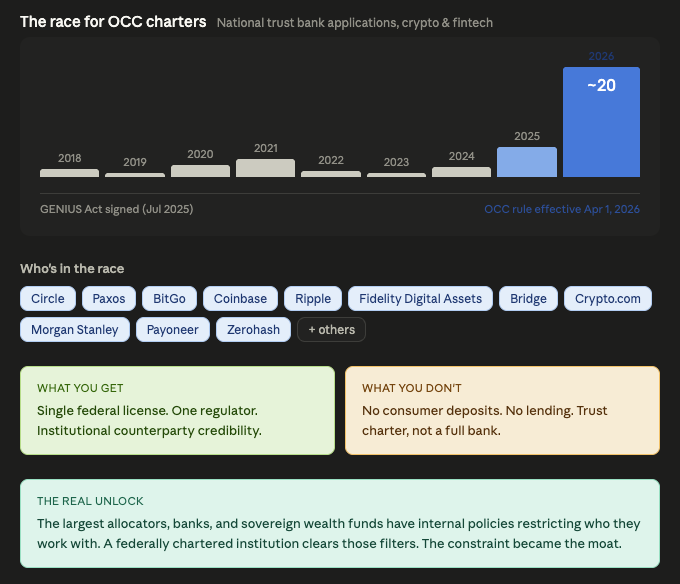

I'm old enough to remember back (a couple years ago) when every fintech company was very explicit about wanting to be bank-like but definitely, absolutely, 100% not a bank. They didn’t want the regulatory constraints, compliance burden, or the lower market multiples. They wanted to get close but not cross the line.

But now everyone wants an OCC charter. Something like 20 companies have applied or received one in 2026 alone (e.g. Circle, Paxos, BitGo, Coinbase, Ripple, Fidelity Digital Assets, Bridge)

So what changed?

The big thing is that the sponsor bank model broke. Banking partners were pressured into dropping specific (sets of) business clients and so the optionality of staying “unchartered” became a liability. And now with the GENIUS Act, being outside the chartered perimeter is more of an existential risk than it is 'strategic flexibility'

The charter itself is quite limited doesn’t actually enable you to do much in the way of ‘new things’. you can't take deposits or make loans. but what it does give you is a single federal license, one regulator and, perhaps most importantly, the credibility to be a counterparty to serious institutional capital

That last part is the big unlock. the largest allocators, biggest banks, and SWFs all have internal policies that restrict who they can work with. A federally chartered and supervised institution clears those filters much cleaner than a state-licensed model does

It’s just one of many pieces I’m seeing fall into place right now

Banks on stablecoins for the last 10 years through today: "At first they ignore you, then they laugh at you, then the fight you (bank lobby tries to undo a bi-partisan passed law - Genius), then you (the consumer) win"

Stablecoins reduce friction on capital movement

If you're confident capital wants to flow to you, that's a feature. If you're worried it wants to leave, it's a threat

Opposition to stablecoins is basically a revealed preference about which side of that equation you think you're on