Thrilled to share a project I've been refining: a complete, open-source repository on "Deep Learning for Solving and Estimating Dynamic Models in Economics and Finance."

I've cleaned up the materials from my PhD classes and summer schools into one coherent resource. 🧵 1/6

Since I have posted so much on Marx vs. Weber, modernity, and development over the last few weeks, I have posted an updated slide deck of my lectures on Karl Marx and the Marxian Tradition (together with @ferarteaga) here:

https://t.co/TOGm7jXMKG

This is a long deck: 437 slides in the last compilation! (It also takes a few seconds to upload.) If I were to teach it carefully, with plenty of class discussion, I would require a whole semester. Even then, some topics (e.g., the Frankfurt School) receive only a cursory treatment because I focus more on economics and political economy, broadly construed. I hope to extend the discussion of those someday.

However, I cover topics rarely seen in these courses, such as Hans-Georg Backhaus and the Neue Marx-Lektüre, because most of the work is not translated into English and must be read in the original German.

I don’t have an equivalent slide deck on Max Weber, as I haven’t lectured on him. Hopefully, one day I will.

Comments and feedback are very welcome.

Super happy to see Dynamic Programming by Sargent & Stachurski out in the world — rigorous, elegant, and full of applications. A beautiful piece of work❣️❣️❣️

🚀 Draft chapters my forthcoming MIT Press book:

𝗛𝗲𝘁𝗲𝗿𝗼𝗴𝗲𝗻𝗲𝗼𝘂𝘀 𝗔𝗴𝗲𝗻𝘁 𝗠𝗮𝗰𝗿𝗼𝗲𝗰𝗼𝗻𝗼𝗺𝗶𝗰𝘀: A Tractable New Keynesian Framework

A modern, analytical roadmap to TANK & HANK models for researchers, students and policy institutions

https://t.co/La1oqEmGEY

👇

New paper w/ Thomas Norman (Oxford):

*** A game-theoretic foundation for the Fiscal Theory of the Price Level ***

We show that the FTPL can be placed on firm theoretical footing, justifying it in the same way Walrasian eqm has been justified [1/11]

Amazing paper about Local Projections and its relationship with VARs, with a focus on practical implementation. Everyone in the business of estimating impulse-responses should be aware of these issues. Main message: there is no-free lunch, but LP is generally more robust 1/3

The natural interest rate (r*) is the real rate that would prevail in the long run.

The standard view in macro is that r* depends exclusively on structural factors such as productivity growth or demographics.

A short 🧵 a new paper

1/n (n=6)

https://t.co/PcIzhZvDcx

A personal assessment of the evolution of macroeconomic research over the last 40 years (informed by the opinions of many of the main researchers in the field). https://t.co/hWRVp8MYh0

Conclusion: Strong convergence, mostly for the better. Not everything is perfect but, then, nothing ever is.

I even venture (and I can already see the scathing comments; please refrain if you are in insulting mode) that macroeconomics has become a mature science.

@QuantEcon has released an updated version of the Julia lecture notes, with updated manifests and packages for Julia 1.11 support: https://t.co/QgudW2C6dc

Nemmers Prize to Mike Woodford for:

“advancing the New Keynesian approach to understanding economic fluctuations in general equilibrium, bridging the theory and the practice of monetary policy, and incorporating bounded rationality in macroeconomics.”

https://t.co/jk4IH5quqA

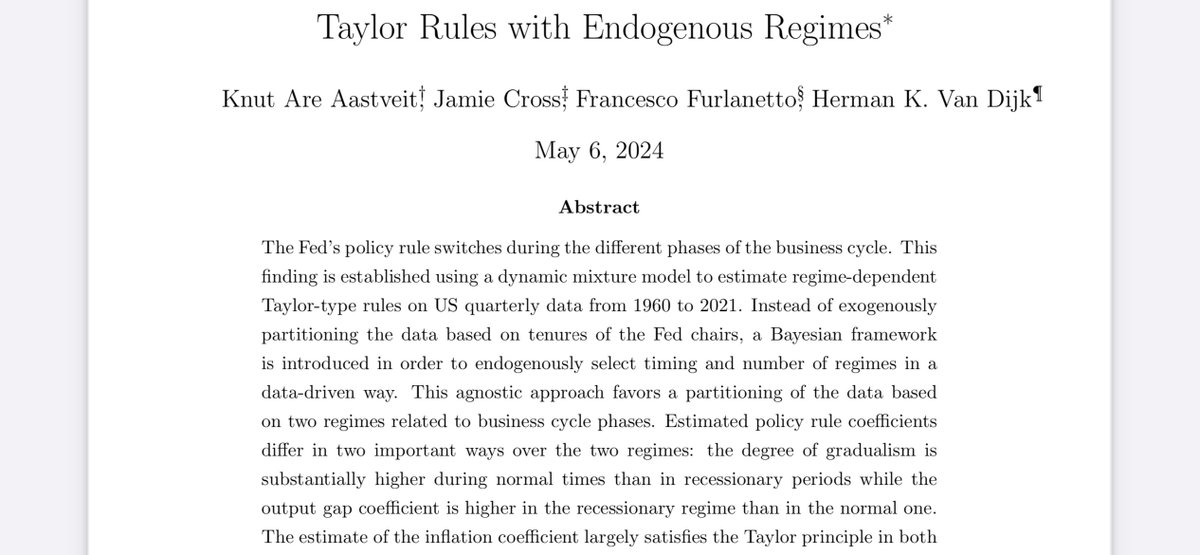

🥁🥁NEW WORKING PAPER ALERT🥁🥁

Taylor Rules with Endogenous Regimes

with Knut Are Aastveit 🇳🇴, Jamie Cross 🇦🇺 and Herman Van Dijk 🇳🇱 https://t.co/w7EtpDEdZh

Main result: monetary policy gradualism is high in recoveries and low in recessions.

#econtwitter 1/N

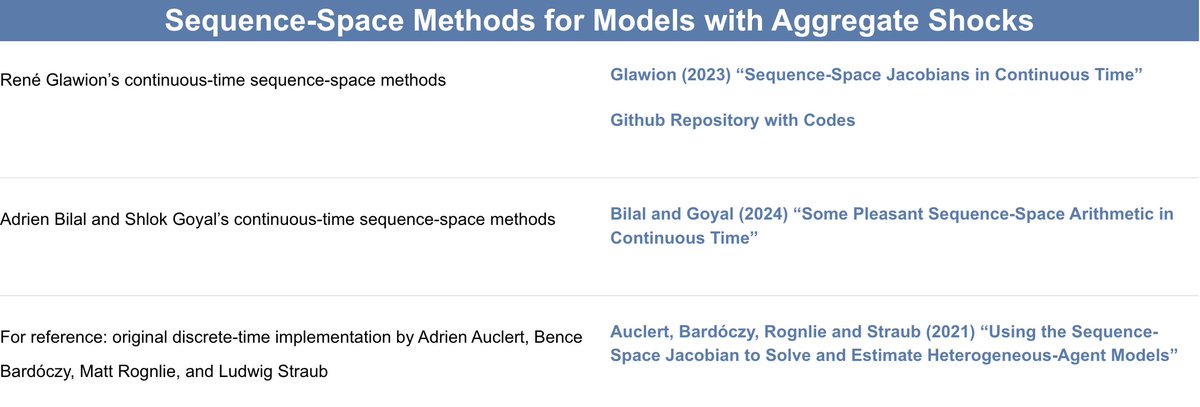

🤓 Nerd tweet for the heterogeneous-agent macro crowd

You like sequence-space Jacobians? But you also like working in continuous time?

Then I have just the thing for you! 🤓

Two very nice recent papers and some code:

![timwillems85's tweet photo. New paper w/ Thomas Norman (Oxford):

*** A game-theoretic foundation for the Fiscal Theory of the Price Level ***

We show that the FTPL can be placed on firm theoretical footing, justifying it in the same way Walrasian eqm has been justified [1/11] https://t.co/QEIdieuRt1](https://pbs.twimg.com/media/GwJHQi5W4AMUyya.jpg)