Most people are learning about memory stocks through AI news or their favorite financial influencers, who themselves only recently discovered the sector.

Here’s my edge: I’ve actually bought memory directly from these suppliers. During my time at a Fortune 50 tech company, I worked as a Memory Operational Commodity Manager, giving me firsthand knowledge of how the industry operates and how the major semiconductor suppliers think.

That direct relationship with their largest clients and understanding of their supply chain constraints, is something you can’t get from Twitter threads or financial media.

Recently, major tech firms are now offering to pay for SK Hynix’s equipment capex. If you understand semiconductor economics, you know this is absolutely unprecedented. It signals desperation for supply and is massively bullish for the memory supercycle ahead.

By subscribing, you’re getting analysis from someone who actually lived inside this industry not just someone reading about it. That’s the difference between surface-level commentary and real conviction. Join the LRMI community today! $MU $DRAM $NVDA $SMH $SNDK $WDC $SKHYNIX

https://t.co/M0wObBIyIx

TSMC is raising prices 5% - 10% on all leading-edge 7nm and below chip manufacturing processes (N7/5/4/3/2 etc.), which account for ~75% of TSMC’s total revenue, reports @tculpan on Culpium, adding: “Since early this year, business development and sales teams at TSMC have been told by senior leadership that they need to find ways to charge more, according to multiple sources…” $TSM $INTC $SSNLF #Samsung #semiconductors https://t.co/a9Eo5NnbNB

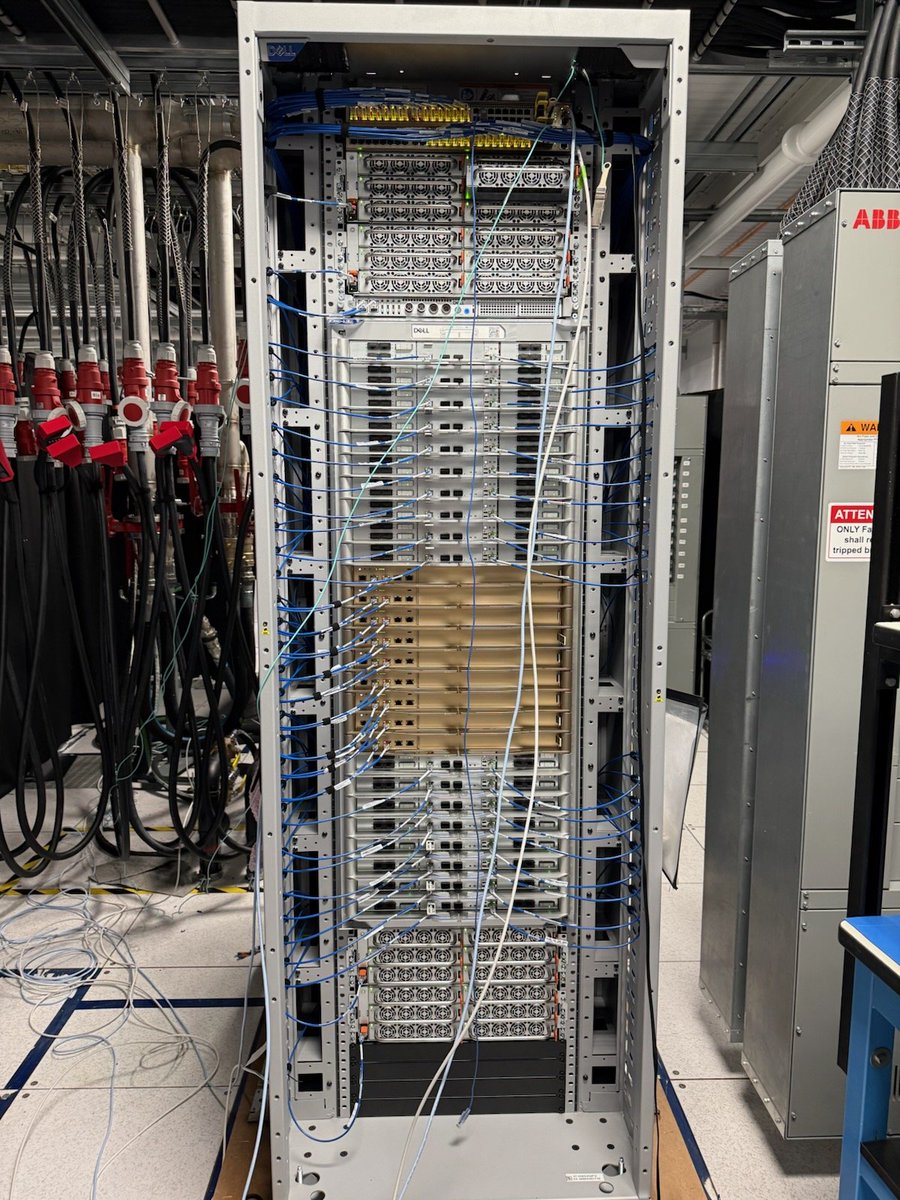

@damnang2 For their fucking server racks lollllll

Qualcomm buys DRAM for the racks hence why they need test engineers to test they’re capabilities in their racks they will sell

$RMBS & $SIMMTECH

Both SIMMTECH and Rambus play key supporting roles in SOCAMM/SOCAMM2 production, though they supply different critical components rather than the DRAM chips themselves (which come from Micron, SK hynix, and Samsung).

$DRAM $MU

Glass core substrates are being evaluated as one possible solution for future high-end packages because they may help support larger package sizes, finer interconnects, and improved dimensional stability compared to conventional package-substrate materials. According to Semi, initial production could begin around 2028 in selected high-performance applications.

Some cool visuals.

Dell Delivers world's first Nvidia Vera Rubin NVL72 rack to CoreWeave.

It packs 72 Rubin GPUs, 36 Vera CPUs, 3.6 exaFLOPS of FP4 inference, 75 TB of fast memory, and 260 TB/s NVLink bandwidth

BREAKING NEWS: COREWEAVE & DELL IS THE FIRST CLOUD TO ANNOUNCE THAT THEY HAVE RUBIN VR200 NVL72 WITH FULLY PASSING L11 DIAGS. Next Step is to get multiple racks burnin in a couple & do software level bringup like sglang, vllm, dynamo, etc.