Blume Ventures’ Indus Valley Report 2025-

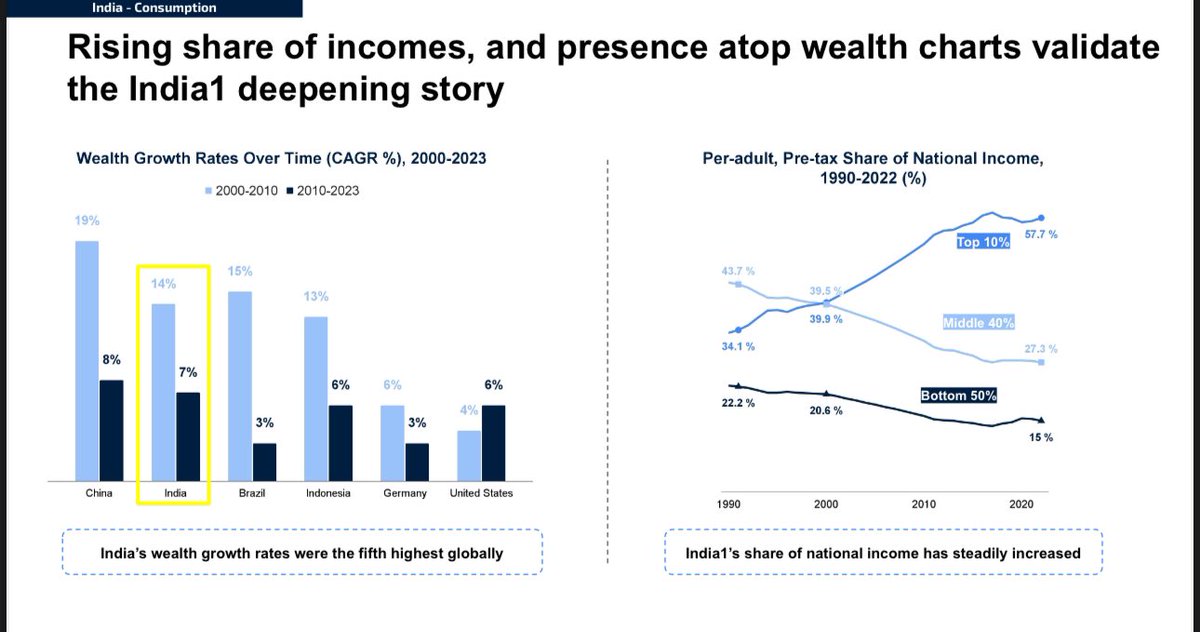

>> India’s consumption paradox,wealth is concentrating. The top 10% now hold 57.7% of income (vs. 43.7% in 1990), while the bottom 50% share has dropped to 15%.

Read more: https://t.co/ILO5vOQHMk

#Indusvalleyreport#Blume #2025

We're thrilled to announce that we have raised $234M in the first close of our $300M Series B at a $1.5B valuation.

@HCLTech and @BessemerVP have joined us in this round, alongside continued support from @khoslaventures and @peakxvpartners

For countries and companies, sovereign control on the AI stack is no longer an optionality. Sarvam will be the partner of choice for this aspiration. The capital allows us to accelerate our momentum towards this full stack of models, compute, and deployments.

A huge thank you to our customers, partners, investors, and the Sarvam team for your trust and belief in what we are building. We’re just getting started.

Read more: https://t.co/VmLtpnj8gx

BREAKING: The European Central Bank officially hikes interest rates by 25 basis points, citing renewed inflation amid the Iran War.

This marks the first major central bank interest rate hike since 2023.

Rate hikes are officially back.

Vishal Sikka was vilified by all and sundry.

He was ahead of his time.

Infosys could have been the first to get into AI in India setting the trend for other Indian software companies to follow.

That was 9 years ago.

India Macro Dashboard

The latest macro dashboard presents two sharply divergent narratives, depending on where you look.

Three key takeaways stand out:

1) Inflation optics vs reality Inflation appears artificially subdued. While CPI is at 3.48%, WPI has surged to 8.30%, a 42-month high. This divergence reflects earlier fuel price suppression, with hikes in petrol and diesel prices today we will see CPI climb. As highlighted in our previous update, producers have been absorbing cost pressures; we expect this to compress margins in Q2, with negative implications for both earnings and valuation multiples.

2) Weakening flow dynamics Foreign capital continues to exit, with six consecutive months of FII outflows, approximately ₹2.83 lakh crore. At the same time, the domestic institutional cushion appears to be thinning, reducing a key source of market support.

3) Conflicting growth signals The macro data is sending mixed signals. On one hand, GST collections grew 8.7%, PMIs remain expansionary, hiring is up 6% year on year, and rural PV sales have risen 20%. On the other, core sectors are losing momentum. Cement growth has slowed from 13.7% to 4%, and steel from 10.1% to 2.2%, even as capital flows weaken. The economy appears bifurcated.

Policy transmission remains ineffective Rate cuts alone may not resolve this divergence. System liquidity has expanded and bank credit continues to grow at 16%. Yet, heavy industry is decelerating sharply, while unsecured lending still grows at 12.8%, pointing to a skewed credit distribution.

Outlook The next two quarters will be critical in determining whether this divergence resolves into a slowdown or a re-acceleration.

@NRIZENOnline

In every board meeting I've sat through, the pricing conversation is the same.

List price. Proposed increase. 45 minutes of debate.

Nobody asks the one question that matters.

What did the customer actually pay?

🧵 on discount discipline.

Within 5 years India will be short of plumbers, electricians, carpenters, drivers, nurses and care givers etc as they will migrate to high income countries.

High income countries are facing demographics collapse and Indian blue collar is the answer.

But don’t worry… we will be left with kids who have white collar degrees with no jobs in India and no requirements in high income countries.

THE STOCK MARKET IS SOMETIMES A CRAZY PLACE

A YEAR AGO, SANDISK SHARES WERE TRADING AT $30 PER SHARE

YESTERDAY, SANDISK SAID IT EXPECTS TO MAKE $31.50 PER SHARE IN PROFIT IN JUST THE NEXT QUARTER

$SNDK