$IONQ Whats going on at IonQ? "They keep getting excluded from government initiatives". Heres a reality check for those not paying attention:

1. IonQ just confirmed its a partner in the Genesis Mission

2. IonQ confirmed it cant give government equity until Skywater deal closes due to non-solicitation restrictions.

3. IonQ was the only hardware vendor chosen by DARPA under the HARQ program. Only vendor capable of providing the interconnect backbone to make quantum data centers and reality.

4. IonQ currently in phase B of DARPA QBI program (unlike RGTI and others) and expects to advance to Phase C in near term. Currently only hardware vendor to publish detailed blue print on how it will achieve fault tolerance (main objective of Phase B).

5. Member of Special Competitive Studies Project for Quantum along with Google, IBM, DARPA, Sandia National Laboratories, Los Alamos National Laboratory, and Senators.

6. IonQ was the only quantum company invited to the White House to meet with King Charles, despite several others (Quantinuum, INFQ) having footprint in UK.

7. Involved in pretty much every leading state initiatives leading the charge on quantum (Chicago, Maryland, Colorado, Florida, Texas, etc.)

8. Strong foothold in more leading countries government efforts than any other pureplay qc company (US, UK, Italy, South Korea).

What exactly is IonQ not involved with?

BUILDING THE INFRASTRUCTURE OF TOMORROW

1. $RKLB building the vertically integrated logistics layer of the space economy through launch vehicles, spacecraft buses, satellite components & propulsion systems backed by a $1.8B backlog & a growing government manifest.

2. $ASTS building the communications layer that connects directly to standard smartphones with BlueBird 7 set to launch April 19 & more than $1B in contracted revenue commitments already in place.

3. $OKLO building the “local nuclear plant” for the AI economy through its Aurora microreactor with $META targeting up to 1.2 GW in Ohio & federal momentum around advanced nuclear continuing to build.

4. $ONDS building the autonomous defense stack across drone communications, counter-drone systems, robotics & secure ISR networks with FY2026 revenue guided to $375M.

5. $IONQ building quantum as the overflow compute layer for problems classical silicon cannot solve with native availability on $AMZN AWS, $MSFT Azure & $GOOGL Cloud plus a recent $54M AFRL contract for quantum networking research.

6. $PL building the real-time geospatial intelligence layer from orbit with a $900M growing backlog & expanding traction across NATO & U.S. government programs.

7. $NBIS building sovereign AI compute infra outside the hyperscaler stack with $46B in contracted AI infra deals, a $2B $NVDA strategic investment & connected data center capacity guided to 900 MW by the end of 2026.

🇺🇸 ABD’li bir girişimci, çöpten topladığı viski şişelerini keserek yaptığı lüks bardakları tanesi 200$ dolara satıyor. üstelik neredeyse hiçbir maliyet olmadan.

$IONQ

Niccolo de Masi told investors how to judge IonQ.

Three things decide each quarter. Revenue, technology, and execution.

Start with revenue. Is the company meeting or beating numbers? Is interest turning into paying customers? For a young tech company, revenue is proof demand is real.

Then technology. Are the systems getting better? More performance, more scale, stronger networking, and products customers can use.

Then execution. Can the company grow without getting messy? This is where many growth companies break down. Slow delivery, weak operations, poor go-to-market.

Most young companies are only strong in one area. Some have technology but no sales. Others sell but cannot scale. Some are just stories.

de Masi's point is that IonQ has to improve across all three at once. Better numbers, better products, and better operations.

For investors, the quarterly question is simple.

Is IonQ getting better across all three, or not?

2028: The Year the Lights Go Out for AI Clusters?

The AI industry has officially shifted from a "Compute Crunch" to a "Photonics Panic."

$LITE CEO Michael Hurlston just delivered a seismic warning: if current order rates for US hyperscalers persist for just two more quarters, their production capacity will be completely sold out through the end of 2028.

This isn't just a corporate milestone; it’s a structural ceiling for AI growth.

When the market leader closes its books for the next three years, the "Optical Nervous System" of AI becomes the most valuable commodity on Earth.

1⃣The Direct Capacity Alternatives (Primary Laser & Module Sources)

As hyperscalers scramble for slots that Lumentum can no longer provide, they are diverting billions to the only other firms with high-volume production lines:

➡️Applied Optoelectronics $AAOI:

The primary beneficiary of the spillover. Their strategic partnership with Microsoft and massive Texas-based manufacturing capacity makes them the immediate "Plan B" for 800G and 1.6T modules.

➡️Coherent $COHR:

Lumentum’s most formidable rival. They hold a massive share in EML (Electro-absorption Modulated Laser) technology.

With LITE full, Coherent becomes the default gatekeeper for high-end optical capacity.

2⃣The Foundry & OSAT Layer (Manufacturing & Advanced Packaging)

These firms provide the physical fabrication and specialized assembly services for the industry's biggest players:

➡️Tower Semiconductor $TSEM:

A crucial "Foundry" player. They specialize in Silicon Photonics (SiPh) fabrication, acting as the factory floor for fabless designers who need to integrate light onto silicon at scale.

➡️Fabrinet $FN:

The "Gold Standard" of optical contract manufacturing.

They physically assemble the complex modules for Nvidia, Cisco, and Lumentum.

A sold-out industry means Fabrinet’s high-precision lines are the most contested real estate in tech.

3⃣The "Intelligence" Layer (DSP & Architecture Control)

Hardware is useless without the silicon that manages the signals.

This layer dictates the efficiency of every photon:

➡️Marvell $MRVL & Broadcom $AVGO:

The duopoly in DSP (Digital Signal Processors). Every laser module requires their silicon to "talk" to the GPU.

Marvell’s TERA platform is the mandatory brain behind the 1.6T era.

➡️MACOM Technology $MTSI:

The pioneer of LPO (Linear Pluggable Optics). By removing the power-hungry DSP in specific short-reach links, MACOM offers a "power-saving" escape hatch for data centers hitting their electricity grid limits.

4⃣The Innovation Accelerators (Bridging the Supply Gap)

With traditional capacity blocked, these innovators are accelerating "Next-Gen" architectures to bypass the bottleneck:

➡️Sivers Semiconductors $SIVE:

A leader in external light sources (CW-WDM) for CPO (Co-Packaged Optics).

Sivers is essential for moving the laser from the pluggable module directly into the processor package - the holy grail of efficiency.

➡️Alumea $ALMU:

A specialist in high-efficiency silicon photonics engines, streamlining the transition to 1.6T and 3.2T speeds where traditional optics fail.

➡️POET Technologies $POET:

Their "Optical Interposer" is a motherboard for light, allowing for radical miniaturization and lower-cost assembly compared to traditional "active" optical alignment.

➡️Lightwave Logic $LWLG:

Developing proprietary electro-optic polymers. These materials modulate light at speeds (200G+ per lane) that standard inorganic crystals struggle to achieve.

5⃣The Transport Giants (DCI & Global Infrastructure)

Data must move between clusters and across continents. These firms control the "Inter-City" light:

➡️Ciena $CIEN: Their WaveLogic coherent optics are the global standard for long-haul Data Center Interconnect (DCI).

➡️Nokia $NOK - Optical Networks (NOC):

They provide the high-capacity optical transport and carrier-grade routing that form the literal backbone of the global AI internet.

6⃣The Quality Gatekeepers (Testing & Validation)

In a world of scarcity, a single "dud" laser can take down a $10B cluster.

Yield is everything:

➡️Aehr Test Systems $AEHR:

The kings of wafer-level "burn-in."

Their FOX-XP systems test thousands of lasers simultaneously under extreme stress to ensure they don’t fail after installation.

➡️FormFactor $FORM:

They provide the ultra-precise "probes" and test systems that validate optical performance on the wafer before it is even cut into chips.

7⃣The Atomic Foundation (Raw Materials & Substrates)

The "Bottleneck of Bottlenecks."

No substrate = no laser.

Period.

➡️AXT Inc $AXTI:

A critical supplier of Indium Phosphide (InP) wafers—the physical medium required for the high-performance lasers that drive AI.

➡️IQE PLC $IQE:

The masters of Epitaxy. They "grow" the complex semiconductor layers on wafers atom-by-atom. IQE is the first point of failure in the global supply chain.

➡️Soitec $SOI.PA:

The dominant provider of SOI (Silicon-on-Insulator) wafers, the essential building block for the entire Silicon Photonics movement.

⬇️Executive Summary: The Photonics Supercycle

A situation where a market leader (Lumentum) sells out production nearly 3 years in advance happens once a decade. This means the speculative phase of AI has ended, and the phase of brutal infrastructural execution has begun.

Key Investor Takeaways:

▶️Seek "Available Capacity": If LITE is full, capital and orders will immediately flow to AAOI and COHR.

▶️Watch the Foundations: Without wafers from AXTI and processes from IQE, not a single additional laser can be built. These are the true "Gatekeepers."

▶️Bet on Quality: With such massive production scales, errors are inevitable. Testing companies like AEHR and FORM will benefit from every photon produced.

▶️Innovation is Mandatory: New architectures like LPO (MACOM) or CPO (Sivers/POET) are no longer just curiosities, they are the only way to prevent AI from "suffocating" due to energy and bandwidth limits.

⬇️Question to the Community:

Analyzing the current supply chain and the fact that optical infrastructure is becoming the new "AI bottleneck", which of these companies would you invest in today at their current market valuation?

Which one has the highest potential for a "re-rating" in the coming quarters?

Let us know in the comments by dropping the Ticker! 👇

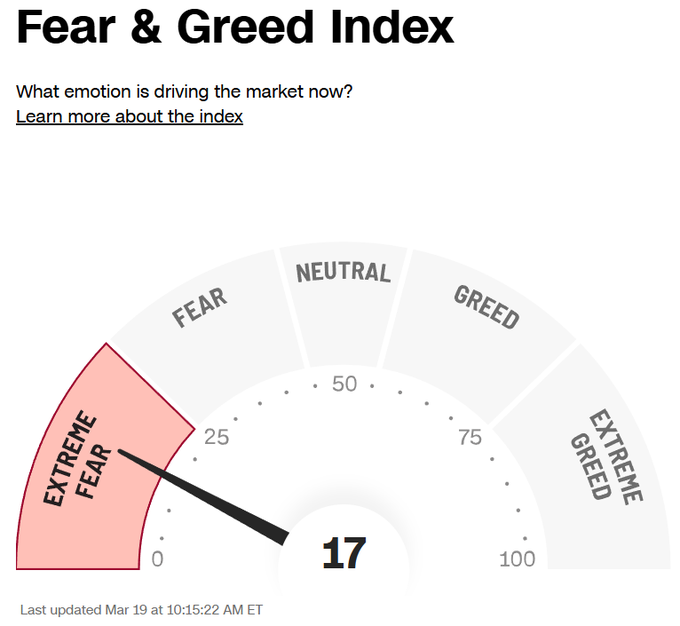

The Fear & Greed Index is back in extreme fear.

Stocks are voting machines in the short term & weighing machines in the long term but what’s being “voted on” right now is emotion.

The real skill is learning how to hold conviction through volatility without emotional sabotage.

🚦 ¿Sabías que puedes girar a la derecha en rojo? Es legal según el Art. 118, pero solo si es seguro.

Ten en cuenta:

👣 Cede el paso al peatón

🚗 Verifica la vía

🚫 Si hay señal que lo prohíbe, no gires

💙 Así recuperamos Cali

FAVORITE 10 NAMES UNDER $10B

1. $ONDS drone connectivity layer

2. $CIFR landlord of the AI utility era

3. $JMIA scaling logistics across Africa

4. $LMND AI-native insurance platform

5. $DOCN AI inference cloud for builders

6. $CLPT navigation platform for neurosurgeons

7. $EOSE zinc storage built for nonstop compute

8. $NVTS powering AI data centers with GaN chips

9. $OKLO modular nuclear power for AI data centers

10. $TMDX expanding organ care with fleet & network effect

To quote the late, great Charlie Munger:

"If all you ever did was buy high-quality stocks on the 200-week moving average, you would beat the S&P 500 by a large margin over time. The problem is, few human beings have that kind of discipline."

$MSFT

Charlie Munger watched Berkshire fall 50% three different times and stayed the course.

Volatility is the toll you pay to be a growth investor and these resets are part of the process where its designed to shake you out before the trend pays you back.

Imagine spending the last five years buying $PYPL because it looked “cheap” only to ride it down over 80% while dismissing $PLTR as “expensive” using traditional metrics in an market that still has no idea what the ceiling on AI actually is.

Don’t be a PainPal investor.