WELCOME TO THE ROOM: Satya Nadella's Lesson in Executive Accountability

Most people treat a senior promotion as a destination; in reality, it is an invitation to a higher level of pressure where excuses are considered a form of professional failure. In "The Room," the distance between a "theory of success" and "actual success" is measured by one thing: Intellectual Honesty.

If you are waiting for more resources, more time, or more favorable conditions to win, you aren't leading—you’re whining. True leadership is the act of "manufacturing success" within the constraints of reality. It requires the scientific rigor to align your resources to your theory, the telemetry to admit when that theory is failing, and the courage to pivot before the runway disappears.

The Bottom Line: You are either a generator of clarity or a creator of confusion. If your "dots don't connect" from your current headcount to the final result, you are just managing decline. Stop talking, get the telemetry, and operationalize the win. Anything else is just noise.

https://t.co/T3JQrXRrDu

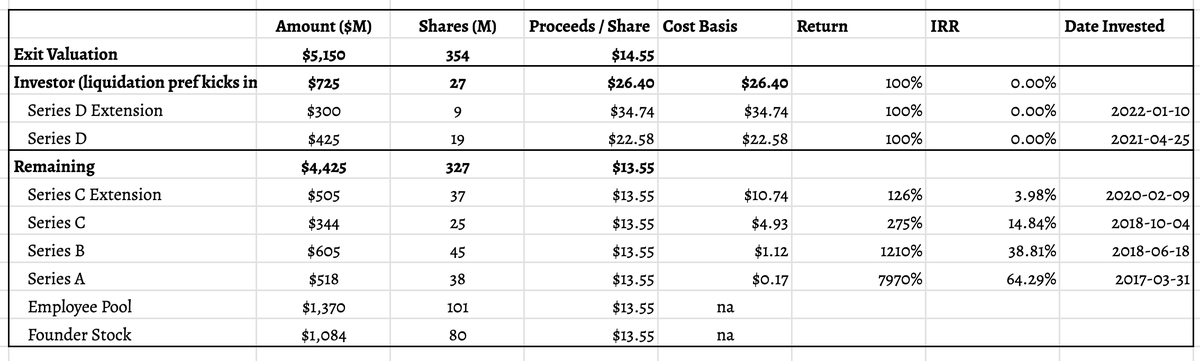

Put together a quick analysis of the Brex exit based on an analysis of their cap table.

Done relatively quickly, so pardon any errors! Funding history sourced from @CaplightData.

Overall, it's a pretty big win.

— The company probably minted well in excess of 100 millionaires.

— Everyone who joined or invested in 2018 or earlier is probably pretty happy, some even ecstatic.

— Those who invested / joined in 2020-21 probably aren't but that is a story that is true of almost every employee or investor in that period (private / public market).

— Those who joined in late 2022 through today is probably doing reasonably fine.

Common Stock TL;DR — liquidation Preference took a bit of a bite, but only for those who joined in 2021-22. Everyone else either did fine or really well.

- Founders did very well (~$1B in total). There was a decent bit of dilution, particularly from healthy option pools over the course of 8-9 years.

- Employees joining 2023-2025 would probably be roughly breakeven — they probably received RSUs priced in the $4-6B.

- Employees joining 2021-2022 got stock at the peak. These would have been underwater RSUs or options. Most companies issued additional make-whole shares to those who stuck around. I'm sure Brex did this. However, those who joined then and left after a couple of years probably lost most of the value to their equity.

- Employees joining 2020 did okay -- slightly above where they joined. Not commensurate with the risk, but honestly way better than most companies who raised at peak valuations in the COVID era.

- Employees joining earlier did VERY well. I'd estimate 3-10x if they joined in 2018-19; and 10-100x if they joined in 2017-18.

Investor TL;DR

- Series D/D+ investors in 2021-21 (Tiger, Greenoaks) get money back but 0% IRR. TBH this is a win since most late stage investments in that vintage are tough.

- Series C+ investors in 2020 (Kleiner, DST) get a modest return (1.3x) but suboptimal IRR (4%). Again, tough vintage.

- Series C investors in 2018 (DST) get a decent return (2.75x) and 15% IRR.

- Series B investors in 2018 (YC Continuity) gets an excellent return (12x) and IRR (39%)

- Series A investors in 2017 (Ribbit) did fantastic (80x and 64% IRR)

- YC worth calling out — the regular YC check probably netted out close to $100M, on an (I think) $120K check at the time. 800x in 9 years = 110% IRR ain't half bad. If you bake in YC continuity, a total of $600M on probably ~$40M invested.

The best definition of success is "Optionality."

You have options - in how you spend your time, your money, what healthcare you receive, how you pace your work, how you help those you care about...and generally how you live your life.

Success is Optionality, full stop.

I know the Discourse™ has moved on already, but just in case - no, Austin will not be replacing SF as the tech capital.

This year there was a 9x gap between capital invested into SF startups vs Austin startups (just in seed + Series A rounds).

One stat of many.

@bhalligan@PeterJ_Walker has some interesting data suggesting that Boston is still a top 3 geo for seed/A startups by $ funded (though still lagging SF/NYC by a long shot). Suggests companies are getting started, but perhaps not staying in Boston?

The biotech sector has been struggling for some time.

The problem is largely macroeconomic, driven by a business model that is poorly suited for current market conditions.

In the 2000s and 2010s, interest rates were low and equity markets were uneven, so investors looked elsewhere for long-horizon, high-reward bets. Biotech fit that profile. Most companies failed to produce a product, mostly failing somewhere along the FDA process, but the few successes delivered very expensive healthcare products very late.

As rates rose and equity markets strengthened in the 2020s, the incentive to fund biotech collapsed. Investors could earn ~5% with no risk or achieve reliable returns in public markets, leaving little appetite for decade-long risk in biotech.

The fallout, as this article highlights, is visible: PhDs unable to find work, excess lab space, and biotech hubs noticeably diminished — in Boston, in Research Triangle Park in North Carolina (which now feels like a ghost town), and elsewhere.

China and the overtraining of scientists are major factors, but they are not the full explanation. At its core, this is a business-model problem.

A viable path forward requires changing how biotech operates - toward cheaper, faster, more abundant, and less regulated healthcare products - not simply waiting for market conditions to reverse.

https://t.co/axe8cQl2Yq

in an era where it’s more tempting and possible to build your own tailor-made software solutions to solve problems, the litmus test: build the apps you want to maintain in the future (stuff that is differentiating), don’t build stuff you don’t want to maintain.

This happens at large companies too, especially those undergoing transformation! Most bigcos observe metrics reflecting the health of their business today, rather than observing metrics that reflect future health.

This is a great post

Stage adjustment from @sbensu's guidance: at Series A/B nobody who's been at your company and in their current role 6-8+ weeks should be blind.

https://t.co/DbCVgXdrah

At this point in my career, I’ve seen deals lost for just about every reason you could possibly imagine.

So I can recognize “trouble” immediately.

Now, I refuse to forecast a deal if any of these 3 things are true:

FAANG software engineer tells how they vibe code at FAANG

---

"You still always start with a technical design document. This is where a bulk of the work happens. The design doc starts off as a proposal doc. If you can get enough stakeholders to agree that your proposal has merit, you move on to developing out the system design itself. This includes the full architecture, integrations with other teams, etc.

Design review before launching into the development effort. This is where you have your teams design doc absolutely shredded by Senior Engineers. This is good. I think of it as front loading the pain.

If you pass review, you can now launch into the development effort. The first few weeks are spent doing more documentation on each subsystem that will be built by the individual dev teams.

Backlog development and sprint planning. This is where the devs work with the PMs and TPMs to hammer out discrete tasks that individual devs will work on and the order.

Software development. Finally, we can now get hands on keyboard and start crushing task tickets. This is where AI has been a force multiplier. We use Test Driven Development, so I have the AI coding agent write the tests first for the feature I’m going to build. Only then do I start using the agent to build out the feature.

Code submission review. We have a two dev approval process before code can get merged into man. AI is also showing great promise in assisting with the review.

Test in staging. If staging is good to go, we push to prod."

---

reddit. com/r/vibecoding/comments/1myakhd/how_we_vibe_code_at_a_faang/

M&A is back. Yea for startups!

Unfortunately so is the bad behavior.

Founders, beware of the M&A bait and switch. This happened to a portco recently.

Company signs an LOI for an acquisition. Yea!

Exclusive agreement for 4 months to close.

Company stops fundraising, runs down cash in expectation of closing.

Two days before close acquiring CEO says board did not approve and deal off.

Company goes bankrupt (out of cash)

Acquiring company buys IP out of bankruptcy for $0.05 on the dollar of acquisition price. Gets 95% off the acquisition. Even hires a couple unemployed people.

Founders: keep operating the company as if the LOI won’t close. Keep optionality.

Just met a company that vibe coded an entire CRM to avoid paying for HubSpot or SFDC over the last year.

It’s now become a burden to maintain and missing key functionality / third-party interoperability as they scale…

They’re now migrating to HubSpot.

App layer is fine.

As venture capital scales, the balance tips from idiosyncratic risk to systematic risk.

- Idiosyncratic risk / generating alpha via investments with high levels of inherent/specific risk.

- Systematic risk / generating beta via exposure to categories derisked by momentum.

Therefore, the strategies are very different:

Small VCs seek out idiosyncracy through novel approaches to origination, and manage the associated risk with portfolio design. Operating outside the wire.

Large VCs aim to dominate obvious categories via brand and network advantages which increase their access to deals. Dominating inside the wire.

Obviously, the expectations are also different:

Small VCs need to deliver impressive cash-on-cash multiples (e.g. >5x is good) on a reasonable timescale. The smaller your fund, the easier that becomes.

Large VCs need to deliver reasonable IRR, where the larger the fund the lower the expectation will be (e.g. >14% is acceptable on multi-billion dollar funds).

To an extent, the risk balance and the return expectations are a spectrum. However, firms tend to build human capital around a strategy, which is therefore more binary in nature.

It is impossible to be a small and outlier-oriented, and simultaneously win competitive deals.

It is impossible to be large and momentum-oriented, and simultaneously find genuine outliers.

The most wretched behavior comes from VCs that are seduced by the lifestyle and status of the large VC playbook, and try to attain it with small VC resources.

More often than not, they are used by the big VCs for dealflow and cast aside like worn-out husks when they can't raise a fund 2.

Dr. Fei-Fei Li’s latest article, “From Words to Worlds: Spatial Intelligence is AI’s Next Frontier".

The next big step for AI is the spatial intelligence, built by world models that create consistent 3D worlds, fuse many signals, and predict how those worlds evolve.

LLMs are great with words but weak at grounded reasoning, so models that can represent and interact with space are needed.

Current multimodal models still fail at basics like estimating distance, maintaining object identity across views, predicting simple physics, and keeping video coherent for more than a few seconds.

The proposed answer is world models with 3 core abilities, generative, multimodal, and interactive, so the model can build consistent worlds, take many input types, and roll the state forward after actions.

These models have to keep physics and space consistent so objects act like they would in real life, not just sound correct like text from a chatbot. They need to work with many data types at once—images, sounds, text, and actions—and then decide what to do next in a fast perception to action loop.

They also need to understand how time flows, so they can guess what will happen when things move, like when a robot reaches for something or a person walks through a room. World Labs, the startup Li co leads, is building these Large World Models and their Marble tool is incredible. Its a creator tool that keeps consistent 3D environments that can be explored and edited, lowering the cost of world building.

Training such models needs a universal task function that plays a role like next token prediction but bakes in geometry and physics.

Data must scale beyond text using internet images and videos, plus synthetic data, depth, and tactile signals, with algorithms that recover 3D from 2D frames at scale.

Architectures need 3D/4D aware tokenization, context, and memory, since flattening everything to 1D or 2D makes counting objects or long-term scene memory brittle.

World Labs points to a real-time generator called RTFM, which uses spatially grounded frames as memory to keep persistence while generating quickly.

The near term use is creative tooling where directors, game designers, and YouTubers can block scenes, change layouts, and iterate with natural prompts inside physically coherent sets.

The mid term path is robotics, where the same models give robots a predictive map to plan grasps and navigation in homes and warehouses, cutting trial and error. The long term bet is science and simulation, where controllable worlds accelerate testing of designs in materials, biology, and climate by running fast “what if” experiments before real trials.

AI’s next frontier is Spatial Intelligence, a technology that will turn seeing into reasoning, perception into action, and imagination into creation. But what is it? Why does it matter? How do we build it? And how can we use it?

Today, I want to share with you my thoughts on building and using world models to unlock spatial intelligence in this essay below. 1/n