VC investor at Antiportfolio Ventures investing in LegalTech. Formerly at @DFJgrowth, Crossbeam VC, @DormRoomFund, and angel investor in several startups

1. Still buzzing from Blooming Day 2025! We celebrated our Series A, launched some incredible new tech, got a message from President @BillClinton and Senator @SenGillibrand, and shared hugs, laughs, and big dreams.

@AlmostMedia@WillManidis Old City Tavern sadly shut down! Was a classic - would always bring friends visiting the city there for a pit stop between historical sites for a quick drink / bite

How to prove your business is valuable even before generating revenue

When evaluating pre-seed startups with little to no revenue, the ‘Crossbeam process’ entails reverse-engineering characteristics of a ‘good business’ and trying to back into early indicators. Here are five common factors we focus on:

(1) Utilization data (churn, product extension): if end-users on a b2b platform are logging in multiple times a day, or time in-session and the number of clicks are increasing – even if the revenue isn’t there yet, you can underwrite the probability of low churn and/or product extension.

High levels of usage = product-market fit

This is the most powerful one we work with founders on. Tools like Hot Jar (no affiliation) can make it easy to pull this data.

(2) Position in value chain relative to costs (pricing power): pricing power is strongest when a tool is demonstrably mission-critical, but only takes up a small percentage of overall spend. If the number of times your product is used in a day / week increases over time (progression is key), this becomes even more compelling. Not only can you gain confidence in your gross margins, but also likely has secondary effects on runway for revenue or market size.

(3) Ability to intercept the exact moment demand kicks in (ability to grow quickly): if customers have a specific time they face the pain point, and you have one or two ways to observe that and reach them with an effective solution, it becomes easier to bet on rapid growth. Side note: when it comes to aligning on growth expectations, this recent Jason Lemkin tweet is helpful.

(4) Imperfect comparables that signal adoption or monetization (TAM expansion): if businesses or users are relying on a makeshift solution, showing how they stick with it despite hurdles can validate untapped demand for the product (e.g. people using Craigslist before Airbnb). Similarly, if a comparable business model is monetizing businesses or users at $X per year, you can build a case for achieving a fraction of that early on, with structural reasons as to why your product can match or exceed these numbers over time. Note 'imperfect' comparables are often more compelling, as obvious opportunities may have already been exploited or arbitraged away.

GTM velocity relative to burn (potential for high ROIC): if you can prove that you achieved certain GTM milestones (e.g. shortening cycles from demo to trial periods, word of mouth driving pipeline) while burning minimal cash, you can create an operating model where small investments can lead to outsized results over time.

While we highlighted a few here, additional drivers can also indicate a strong business foundation, including founder track record / market fit, strategic partnerships, proof of a growing market and/or operating in a niche with limited competition to name a few. The problem, however, is many of these are fleeting or difficult to observe/quantify. In contrast, it’s hard to argue against clear data that show users are logging on, spending x minutes and/or finishing y ‘jobs’ on a given platform. Once you generate revenue, you can layer on more traditional metrics such as payback periods, retention/expansion, and margin profile over time.

Ultimately, when you’re super early, it’s crucial to highlight various forms of leading indicators that show your business is being built on a strong foundation. By providing clear, measurable metrics of value, you’ll help investors get to a “yes” quicker and with more conviction.

If you are building anything in LegalTech (or even adjacent, e.g. RegTech or GovTech) or want to connect - ping me at [email protected], I'd love to chat

Now that we have 8+ LegalTech investments, I figured it was time to write about what makes the category special in our minds, and mention 5 specific business strategies that we're excited about. Read more at the link here: https://t.co/LgbmgZFf9i

If you or someone you know is building something that helps enable Government Relations as a Service (GRaaS), get in touch. I’d love to talk and hear more.

Sure, consolidation is one reason there are fewer companies in the defense industrial base.

But a bigger issue facing companies today is actually bureaucracy / some of the struggles that come with working with a government entity.

I imagine a GRaaS provider will help with a few things - Help win government contracts

- Potentially creating an insurance pool for contracts (reducing reliance issues)

- Group purchasing for discounts

- Centralized PEO / benefits

- Helping with other compliance tasks

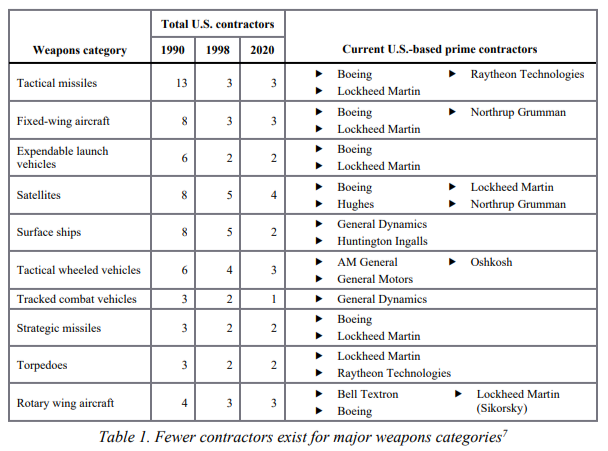

Suppliers of tactical missiles dropped from 13 to 3 since 1990. Surface ships from 8 to 2. Aircraft from 8 to 3.

The total number of A&D primes fell from 51 to 5. Competition is good for the ecosystem and good for America.

DoD spend is massive - in the range of ~$350 billion. But partly because the number of suppliers is decreasing, 52% of the dollars going out the door are to contracts for which there was no competition. That’s roughly $200 billion dollars for contracts that had no competitors.