Some personal news: I've joined Framework Ventures (@HiFramework) to invest where finance, AI, and the real economy are being rebuilt from the ground up.

Framework has been the fund I've measured my own thinking against for years. Across multiple cycles, @pythianism and @im_manderson have been early to where new financial infrastructure actually meets the real world: tokenization, AI, fintech, energy, compute, robotics, and more. They aren't shying away from re-inventing how a venture capital firm operates in this market.

I'm spending my time with founders pulling the future forward: founders building credit, payments, and settlement for the next economy. Founders building the energy and compute infrastructure that AI demands. Founders running toward the hard problems that define new categories.

If that's you, I'd love to hear from you.

—

Closing out 4+ years at @PanteraCapital, I'm grateful beyond words to @veradittakit , @dan_pantera, @FranklinBi , @cosmo_jiang , and the founders who trusted us to back them.

@pythianism led our latest round when we were down to our last few dollars after several pivots, from NFTs to Watches to other esoteric loans

We were still early in our search for PMF. But because @hiFramework is based in SF & invested early in AI HPC biz like @corescientific, they had a direct view into how companies were being boxed in by Wall Street players offering predatory loans

Today, @USDai_Official has seen $15bn in traded volume, built a >$1.4bn loan pipeline, and continues to receive multiple new loan inbounds everyday.

Framework is the kind of partner you should talk to if you have a radical idea about how the world should work & should be rebuilt. For us, that idea was using stablecoins to help solve AI financing, or using the fastest horse for the AI arms race.

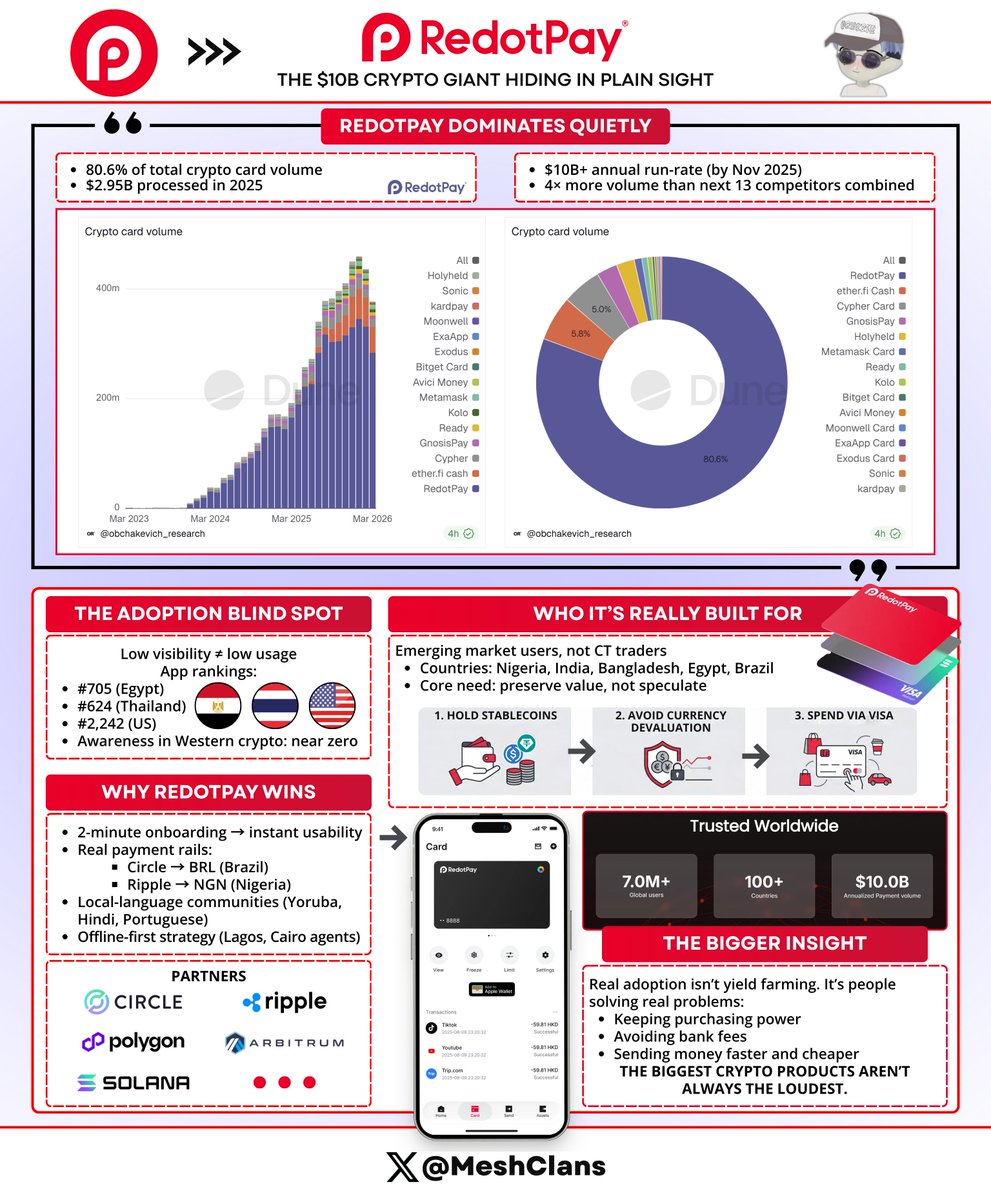

RedotPay controls 80.6% of crypto card volume. Ask 100 people in crypto if they've used it, maybe 2 have even heard of it. I hadn't either until I saw this chart.

I spent some time digging into this anomaly, and what I found changed how I think about crypto adoption.

The data from @obchakevich_ 's Dune dashboard shows @RedotPay processed $2.95B in card transactions during 2025, over 4x what its next 13 competitors did combined, and they hit a $10B+ annualized run-rate by November 2025.

But here's the weird part the app ranks #705 in Egypt's Finance category and #624 in Thailand, while sitting at #2,242 in the US. I asked 30+ people in Western crypto circles about RedotPay. Two had heard the name. Zero had actually used it.

So how does a platform almost nobody on crypto Twitter knows about hit $10B+ in annual run-rate?

Turns out we've been looking at the wrong map.

RedotPay built for people in Bangladesh, India, Egypt, Nigeria, and Brazil who don't have reliable banking, and the actual use case is straightforward: hold USDT so your savings don't get destroyed when your local currency tanks, then spend it via Visa card for everyday stuff like groceries and bills.

They're not chasing airdrops or staking yields. They just want their money to hold value.

Instead of burning cash on Facebook ads, RedotPay recruited local crypto traders, community leaders, and OTC merchants as agents who earn up to 40% commissions when someone activates a card. The $100 physical card fee and $10 virtual card fee fund the whole thing, and most of their 2025 growth came from people searching for them organically through pure word of mouth in communities we never see.

Getting started takes two minutes: download app, send some USDT, spend anywhere Visa works.

Why is RedotPay so far ahead?

- Two-minute onboarding from download to spending, versus hours learning DeFi protocols

- Real infrastructure through partnerships with Circle (June 2025) for instant BRL payments to Brazil and Ripple (December 2025) for NGN to Nigeria, moving money in minutes instead of days

- Local communities built on Telegram groups in Yoruba, Hindi, and Portuguese, generating massive engagement in languages most of CT doesn't read

- Offline-first distribution with agents on the ground in Lagos and Cairo beating online ads every time

What people actually do with it:

- Deposits are 98%+ stablecoins (USDT/USDC)

- Spending happens in small amounts multiple times per week

- Real uses include buying food in Cairo, sending money to family in Lagos, and protecting savings from currency collapse in Nigeria

The numbers back it up: they hit 5 million users by August 2024, got to 6M+ users by November 2025 while adding 3M+ just last year, tripled their volume in 2025, and they're profitable.

They built it for specific people with specific problems we don't face, and actual adoption looks like a guy in Nigeria making sure his paycheck still buys groceries next month, a family in Egypt paying bills without bank fees, or someone in Bangladesh sending money home without losing 8% to Western Union.

Utility beats speculation when it comes to real volume. Needs drive actual scale. Sometimes the biggest things happen where we're not looking.

Makes me wonder what else is out there that we're completely missing.

Claude is unreal. 2017 me at BCG would have been a superhuman. Just one shotted an entire dashboard on LATAM lending and bank rates in ~5 minutes. That used to be a full analyst day.

Congrats to @Figure for this consequential and monumental transaction. Onchain IPOs are here to stay. Its always a pleasure working with @mcagney and @MBTannenbaum.

FGRD is now available on OPEN! 🎊

FGRD is Blockchain Common Stock of Figure Technology Solutions, Inc., and a demonstration of how Figure’s end-to-end tokenized stack works in a live environment.

Token features and utility:

• Fully regulated, via Figure’s OPEN infrastructure

• Illustrates how on-chain equities can be issued, traded, and used within a single integrated system

• Serves as a reference model for issuers and institutions

Public equity is changing. FGRD is proof.

History is made.🛎️

We’re proud to announce that pricing has officially closed for FGRD, the first public equity to be natively listed, traded, and settled entirely on blockchain infrastructure, leveraging Figure’s ATS for instantaneous settlement.

Thanks to the OPEN (On-chain Public Equity Network), we've eliminated the legacy intermediaries (DTCC, we hardly knew ye) and built something incredible: equities that live natively on-chain, are tradeable 24/7, and are composable from Day One.

Secondaries are coming. Be ready.

@USDC For more on how we’re thinking about building onchain and the types of startups we’re excited to fund, check out our Request for Startups: https://t.co/4LDGzKeRBH