A few weeks ago @nerdalert put his foot in his mouth on a call with the team at $LMND.

One throwaway comment turned into a much bigger question:

Are investors looking at Lemonade the wrong way?

🚨 FORMER TESLA PRESIDENT ADMITS ELON USED THE DOMINO’S PIZZA APP TO REINVENT HOW PEOPLE BUY CARS — AND THE STORY IS BLOWING PEOPLE’S MINDS

Former Tesla president Jon McNeill is going viral after revealing the bizarre moment Elon Musk pulled up the Domino’s pizza app during a meeting… because Tesla customers needed 64 CLICKS just to buy a car online.

Elon’s reaction?

“How many taps does it take to get a pizza?”

Answer:

• 10 taps

Buying a Tesla at the time?

• 64 clicks

• endless loan documents

• nonstop forms

• massive friction

Elon became obsessed with stripping the process down after realizing most of the paperwork wasn’t even legally required.

So Tesla started going bank-to-bank asking:

Why does buying a car need to feel harder than ordering dinner?

Most banks reportedly refused to cooperate.

Then one Midwest bank CEO finally agreed to test a radically simplified system… and Tesla allegedly eliminated around 40 clicks from the process almost overnight.

Now people online are saying this perfectly explains why Tesla disrupted the entire auto industry while traditional dealerships kept drowning customers in paperwork, waiting rooms, and sales tactics.

Did Tesla accidentally expose how outdated the entire car dealership model really was?

📹: kencoleman

Investing in growth stocks and early companies would need strong stomach. One needs to stay focused on the fundamentals and focus on the long-term trajectory.

For all the $LMND investors 🍋📊

My take on Q1: great numbers, long-term story evolving perfectly, Pet insurance now the #1 business

Why the stock doesn't care? These results were baked in. @Lemonade_Inc chugs along at ~30% growth in it's core biz every quarter

Lowkey boring. A great all-time business in the making, but insurance is not like AI coding, it's a slow and steady book of business build. Exponential growth won't happen

I've been using Lemonade car insurance for 2 months now and loving it. That could be a huge business long-term

I think 2027 is going to be a breakout year for profits and cashflow. Proving the durability and operating leverage of the business. Until then we build, brick by brick 🧱

@Lemonade_Inc Here is a graph of all products' IFP over time. Note how nicely Pet (green) is climbing as well as Car (purple) is just starting to ramp. Pet is a significant and growing market and Car market is enormous (~$300B in US alone).

Lemonade’s Q1 results are 🔥. So much to share, where do I start?

First, get into the AI mood, click this, + volume ⏫

https://t.co/IDPCvrTHge (by @kidfrancescoli)

🚀10th consecutive quarter of accelerating IFP growth

🔥 Topline at $1.33 Billion (IFP +32%)

🔥 Revenue grew 71% to $258M

🔥 Gross Profit increased 159% to $100M

🔥 3.14M Customers

🔥 Adj. Free Cash Flow $17M

Lemonade Pet exploding!

✅ Surpassed $500M top line early in Q2

✅ #1 most searched pet insurance brand in the U.S.

✅ @lemonade_inc is now the 4th largest pet carrier in the U.S.

✅ AI-powered automation drives record claim handling efficiency (LAE: ~4%)

✅ Our data + tech edge lets us lower prices while boosting profitability

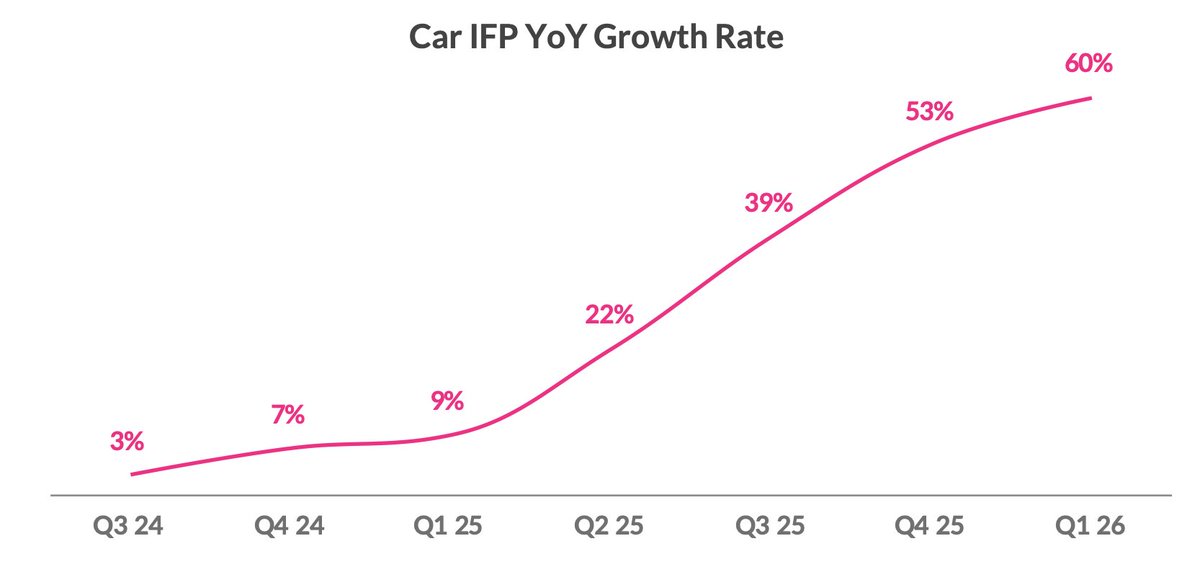

Car picking up speed

✅ Now at 60% YoY growth, $214M IFP

✅ Loss ratio improved to 74% (14 pts better YoY)

✅ Autonomous Car for @Tesla FSD conversion rate 70% higher than standard

And more...

↗️ Raising 2026 top & bottom line guidance

↗️ IFP per employee > $1M (3x improvement in 4 years)

↗️ Positive Adj. EBITDA in Q4

↗️ Investor Day in NYC November 17

For 1,800 of the last 2,000 years, China or India was the world's #1 economy. America has held the title for about 150.

The chart is 2,000 years of mean reversion.

In year 1 AD, Han China and the Indian subcontinent together produced more than half of world economic output. In 1500, still around half. In 1700, on the eve of the Industrial Revolution, China alone was 22% and India was 24%. Two countries, half the world's GDP, for 17 straight centuries.

Then a 200-year glitch began.

Britain mechanized cotton in 1780. Steam engines, railroads, iron smelting, the factory system. Per capita output in northwest Europe doubled, then quadrupled, then went 10x while Asia stayed agricultural. India was actively deindustrialized by British trade policy. The Qing Dynasty got carved up by foreign concessions. Japan's Meiji Restoration in 1868 was the only Asian economy that industrialized in time to defend itself.

By 1950 the chart is unrecognizable. The United States alone was nearly 28% of world GDP. The combined share of China and India had collapsed below 9%. A civilizational baseline of 50%+ went to single digits inside four generations.

Then it started reverting.

China's reform and opening launched in 1978. India's liberalization came in 1991. The two countries that defined economic gravity for most of recorded history started compounding at 6-10% a year while the developed world settled into 2%. By 2017 China was back to 18% and climbing.

The story of the 21st century gets framed as a rising challenger threatening the established order. The chart says the established order was the threat. The 200-year window from 1820 to 2000 is the deviation. Everything before and after is the mean.

Industrial Revolutions don't happen in the country with the largest economy. They happen in the country that breaks the agricultural ceiling first. Britain did it once. The United States did it second.

Whoever does it next sets the next 200-year baseline.

Paul Graham spent 20 years watching founders and found the visionary model was backwards.

Bill Gates built a BASIC interpreter for a machine with a few thousand users. Mark Zuckerberg built a website so Harvard undergrads could stalk each other. Neither one knew what they were going to become.

That is the opposite of how every startup school, pitch deck, and vision statement tells you to operate. You're supposed to walk in with a 10-year roadmap. TAM charts. A precise picture of the future you're building.

The people who built the biggest companies didn't have a precise vision. They had a direction. Gates had "microcomputers are interesting." Zuckerberg had "Harvard undergrads will use this." That was the entire thesis.

The math explains why. If your target is 10 years out and 100x bigger than anything that exists, every assumption in your model compounds error. Interest rates move. Hardware costs collapse. A competitor pivots. By year three the roadmap is a museum piece and you're optimizing for a world that never arrived.

Graham's analogy is Columbus. Columbus didn't have a map of the New World. He had "there's something to the west" and a boat. The destination was wrong, the continent was wrong, the math on how far was wrong. The direction was right, and the direction was enough.

The inversion every founder gets wrong: the popular image of the visionary is someone who sees the future precisely. Empirically, it's someone who sees it blurry and walks toward the blur while everyone else is drawing detailed maps of imaginary places.

Gates didn't set out to dominate microcomputer software for four decades. Zuckerberg didn't set out to build a universal vacuum for human time. They started with something small that worked, and the opportunity to move came later.

The VCs who fund vision decks and the founders who write them are playing the same game. The founders who actually built those companies weren't in the room.

Interesting article on how enterprises see AI adoption. These match with the issues That I see everyday and discuss with my peers from other organizations.

Another week on the road meeting with a couple dozen IT and AI leaders from large enterprises across banking, media, retail, healthcare, consulting, tech, and sports, to discuss agents in the enterprise.

Some quick takeaways:

* Clear that we’re moving from chat era of AI to agents that use tools, process data, and start to execute real work in the enterprise. Complementing this, enterprises are often evolving from “let a thousand flowers bloom” approach to adoption to targeted automation efforts applied to specific areas of work and workflow.

* Change management still will remain one of the biggest topics for enterprises. Most workflows aren’t setup to just drop agents directly in, and enterprises will need a ton of help to drive these efforts (both internally and from partners). One company has a head of AI in every business unit that roles up to a central team, just to keep all the functions coordinated.

* Tokenmaxxing! Most companies operate with very strict OpEx budgets get locked in for the year ahead, so they’re going through very real trade-off discussions right now on how to budget for tokens. One company recently had an idea for a “shark tank” style way of pitching for compute budget. Others are trying to figure out how to ration compute to the best use-cases internally through some hierarchy of needs (my words not theirs).

* Fixing fragmented and legacy systems remain a huge priority right now. Most enterprises are dealing with decades of either on-prem systems or systems they moved to the cloud but that still haven’t been modernized in any meaningful way. This means agents can’t easily tap into these data sources in a unified way yet, so companies are focused on how they modernize these.

* Most companies are *not* talking about replacing jobs due to agents. The major use-cases for agents are things that the company wasn’t able to do before or couldn’t prioritize. Software upgrades, automating back office processes that were constraining other workflows, processing large amounts of documents to get new business or client insights, and so on. More emphasis on ways to make money vs. cut costs.

* Headless software dominated my conversations. Enterprises need to be able to ensure all of their software works across any set of agents they choose. They will kick out vendors that don’t make this technically or economically easy.

* Clear sense that it can be hard to standardize on anything right now given how fast things are moving. Blessing and a curse of the innovation curve right now - no one wants to get stuck in a paradigm that locks them into the wrong architecture. One other result of this is that companies realize they’re in a multi-agent world, which means that interoperability becomes paramount across systems.

* Unanimous sense that everyone is working more than ever before. AI is not causing anyone to do less work right now, and similar to Silicon Valley people feel their teams are the busiest they’ve ever been.

One final meta observation not called out explicitly. It seems that despite Silicon Valley’s sense that AI has made hard things easy, the most powerful ways to use agents is more “technical” than prior eras of software. Skills, MCP, CLIs, etc. may be simple concepts for tech, but in the real world these are all esoteric concepts that will require technical people to help bring to life in the enterprise.

This both means diffusion will take real work and time, but also everyone’s estimation of engineering jobs is totally off. Engineers may not be “writing” software, but they will certainly be the ones to setup and operate the systems that actually automate most work in the enterprise.

Audio of recent conversation between @jimcramer and @daschreiber. Nothing really new, but it was interesting to hear Cramer say all the young people in his office use $LMND insurance. As well it’s always nice to hear Daniel sharing the thesis and vision.

Software engineers figuring out what is best way to develop software. In the loop or outside the loop or on the loop. It depends on the maturity of the organization in this journey.

NEW POST

There's been much talk about how AI agents affect the workflow loops of software development. Kief Morris focuses on the goal of turning ideas into outcomes by building and managing the working loop.

https://t.co/xkjaSzaE1Z

NEW POST

There's been much talk about how AI agents affect the workflow loops of software development. Kief Morris focuses on the goal of turning ideas into outcomes by building and managing the working loop.

https://t.co/xkjaSzaE1Z

I got into LMND when Motley Fools recommended (around 2021?). It has been a tough ride since then. I am a committed investor. I believe in LMND story and I also like to hear counter arguments.

Video by Matt Frankel of @themotleyfool where he brings on a guest to share some bearish takes on $LMND.

His take? Basically that they are paying too much on customer acquisition and that book value is declining.

These are the same reasoning mistakes we see again and again from bears. They only look at customer acquisition cost purely within each quarter and do not consider the long-term revenue and gross profits that a customer cohort acquired this quarter will pay out for many years.

And with book value, once Lemonade flips to profitability, then book value per share will start rising.

Lemonade: Reasons to Buy and Reasons to Sell

https://t.co/HkhZBkQ8I1