Yup. We agree.

That’s why we keep pushin’

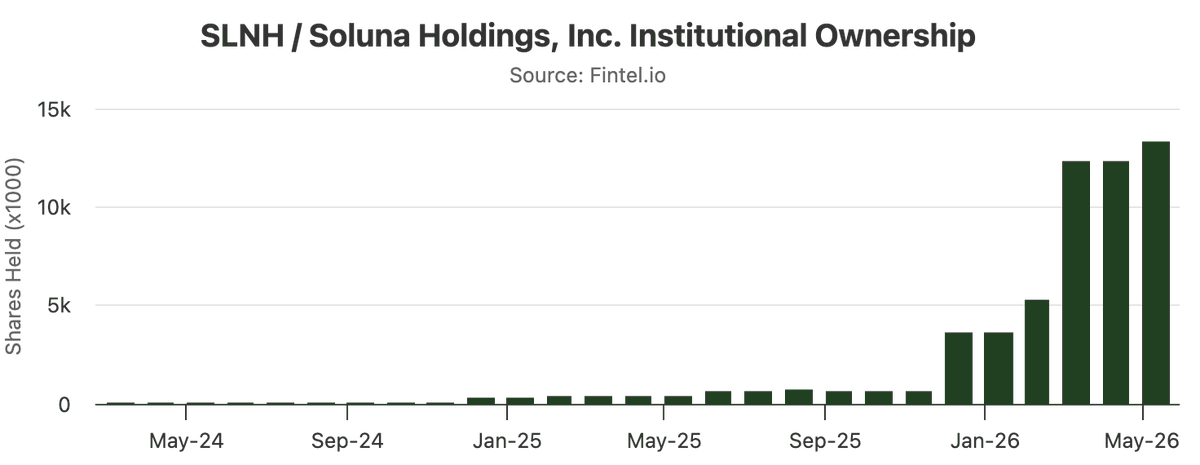

$SLNH @SolunaHoldings

This is from a WSJ article on @GoogleAI strategy to build data centers in a crowded market. Sound familiar? :)

@disruptorinvest@McnallieM

I've analyzed every stock in Leopold Aschenbrenner's most recent disclosure.

There are 2 that got my attention.

He's 25 years old, and his fund grew from $250 million to $13.6 BILLION in less than two years.

He outperformed every fund over the last 12 months.

Check this out:

SHAZ: Australian GPU neocloud

IPO'd on NASDAQ in February 2026.

Market cap around $966 million.

Already sitting on $2.2 billion in total contracted value.

Anchored by a $1.25 billion ESDS deal and a $950 million Asia Pacific contract.

Both ramp in H2 2026.

$2.2 billion contracted on a sub-$1 billion market cap.

TE: T1 Energy

The only US pure-play in domestic solar module and battery manufacturing.

Aschenbrenner initiated a brand new 10 million share position worth roughly $44 million.

T1 just hit its first profitable quarter ever.

Q1 revenue beat expectations by 34% ($177M vs $132M).

First US factory already online. Second one under construction in Texas.

If they close the Q2 financing for the Austin fab, the path to $375 to $450 million in annual EBITDA by 2027 becomes the base case.

That puts TE at roughly 4x forward EBITDA versus peers at 8 to 12x.

The thesis is the same on both names.

Long the bottlenecks of AI.

T1 is the domestic energy bottleneck.

SHAZ is the GPU compute bottleneck.

Both are still under $3 billion in market cap.

These are two of the smallest, earliest bets in his entire book.

We track and analyze insider trades so you don’t have to.

Turn on notifications so you don’t miss our next alert. This is EXTREMELY important.

If you don’t follow us right now, you might regret it later.

As you may know, $SLNH is planning a buildout of its 4.3 GW facility. Currently priced at a ~$207M MC, that would put it's value at ~$48.1M/GW, or $0.048B/GW.

Meanwhile, adjacent names are valued much higher for about the same capacity or even less:

$CIFR: plans to have 3.4 GW by 2029

- $7.69B MC / 3.4 GW = 2.261B/GW

$IREN: plans to have 5+ GW by 2028

- $17B / 5 GW = 3.4B/GW

$NBIS: will (allegedly) have 4 GW by EOY

- $49.76B / 4 GW = 12.44B/GW

Something is definitely wrong here. Either the market has overpriced every neocloud/data center name, OR $SLNH is being severely overlooked amongst its peers...

While $NBIS should be accounted for slightly differently since its facility will be up and running by EOY, you can see how much differently these names are valued in comparison.

$SLNH should be no exception as it plans to have a larger pipeline than both $CIFR and $NBIS, while being valued at a percentage of these names. Even $TE is valued almost 10x higher than $SLNH with a similar roadmap...

Now, this isn't an exact apples to apples comparison. You have to consider execution risk, management, form of energy used, macro factors, etc. However, the theme is there, and the asymmetry is obvious. You can see by the recent volume and the PA over the last couple months that people are catching on.

For clarification, I am not bearish on $CIFR $IREN $NBIS or other adjacent names. I do believe that this sector will be leading the markets in the coming quarters or even for a few years to come. However, the play for $SLNH is more than asymmetrical.

$SLNH has some serious catching up to do, especially once execution stops being a question of "if" and begins being a question of "when"...

$SLNH Soluna Holdings CFO just bought 100,000 shares on the open market at $1.63.

Not options. Not grants. Direct purchase with real money.

Total insider holding now 1.38M shares.

Soluna runs green energy compute infrastructure for Bitcoin mining and AI workloads powered by stranded renewable energy.

CFO putting money in at current levels is worth paying attention to.

Not financial advice.

$SLNH Big visibility catalyst:

@SolunaHoldings appears on the preliminary Russell 3000 additions list for the 2026 Russell reconstitution. Next to $IREN $CRW $NUAI $KEEL

For a microcap transitioning from BTC hosting into AI/HPC power infrastructure, Russell 3000 inclusion can bring:

• more institutional visibility

• potential index-related buying

• broader market awareness

• higher credibility with investors

And the timing is interesting.

Soluna is entering H2 2026 with several key catalysts still ahead:

▪︎ Kati 2 AI/HPC announcements

▪︎ Dorothy 3 AI campus development

▪︎ Briscoe/Dorothy power integration

▪︎ BTC hosting growth

▪︎ 4.3 GW pipeline progression

The market has mostly valued $SLNH like a small crypto infrastructure company.

But management is clearly building something much larger:

a power-backed AI infrastructure platform.

Russell inclusion can help put more eyes on the story right as the most important catalysts are approaching.

LLM Knowledge Bases

Something I'm finding very useful recently: using LLMs to build personal knowledge bases for various topics of research interest. In this way, a large fraction of my recent token throughput is going less into manipulating code, and more into manipulating knowledge (stored as markdown and images). The latest LLMs are quite good at it. So:

Data ingest:

I index source documents (articles, papers, repos, datasets, images, etc.) into a raw/ directory, then I use an LLM to incrementally "compile" a wiki, which is just a collection of .md files in a directory structure. The wiki includes summaries of all the data in raw/, backlinks, and then it categorizes data into concepts, writes articles for them, and links them all. To convert web articles into .md files I like to use the Obsidian Web Clipper extension, and then I also use a hotkey to download all the related images to local so that my LLM can easily reference them.

IDE:

I use Obsidian as the IDE "frontend" where I can view the raw data, the the compiled wiki, and the derived visualizations. Important to note that the LLM writes and maintains all of the data of the wiki, I rarely touch it directly. I've played with a few Obsidian plugins to render and view data in other ways (e.g. Marp for slides).

Q&A:

Where things get interesting is that once your wiki is big enough (e.g. mine on some recent research is ~100 articles and ~400K words), you can ask your LLM agent all kinds of complex questions against the wiki, and it will go off, research the answers, etc. I thought I had to reach for fancy RAG, but the LLM has been pretty good about auto-maintaining index files and brief summaries of all the documents and it reads all the important related data fairly easily at this ~small scale.

Output:

Instead of getting answers in text/terminal, I like to have it render markdown files for me, or slide shows (Marp format), or matplotlib images, all of which I then view again in Obsidian. You can imagine many other visual output formats depending on the query. Often, I end up "filing" the outputs back into the wiki to enhance it for further queries. So my own explorations and queries always "add up" in the knowledge base.

Linting:

I've run some LLM "health checks" over the wiki to e.g. find inconsistent data, impute missing data (with web searchers), find interesting connections for new article candidates, etc., to incrementally clean up the wiki and enhance its overall data integrity. The LLMs are quite good at suggesting further questions to ask and look into.

Extra tools:

I find myself developing additional tools to process the data, e.g. I vibe coded a small and naive search engine over the wiki, which I both use directly (in a web ui), but more often I want to hand it off to an LLM via CLI as a tool for larger queries.

Further explorations:

As the repo grows, the natural desire is to also think about synthetic data generation + finetuning to have your LLM "know" the data in its weights instead of just context windows.

TLDR: raw data from a given number of sources is collected, then compiled by an LLM into a .md wiki, then operated on by various CLIs by the LLM to do Q&A and to incrementally enhance the wiki, and all of it viewable in Obsidian. You rarely ever write or edit the wiki manually, it's the domain of the LLM. I think there is room here for an incredible new product instead of a hacky collection of scripts.

We just wrapped one of the most active quarters in $SLNH history 🚀

Q1 2026 highlights:

→ 147 MW under management, up from 123 MW

→ Bitcoin hosting revenue up 178% year over year.

→ Revenue up 58% YoY; 4 consecutive quarters of growth.

→ Hash rate exceeding 7 EH/s, a new company record.

→ A 4.3 GW power pipeline that keeps compounding.

But the bigger story is what we're building toward...

(1/2)

Leopold Aschenbrenner's 13F never came on Friday.

Here is the REAL reason why, and what it tells you:

The most likely explanation is that he requested confidential treatment from the SEC.

Confidential treatment is a legal tool that lets large funds delay disclosing positions they are still actively accumulating, sometimes for UP TO A YEAR.

Funds use it for one reason: they are building a position big enough that public disclosure would MOVE THE PRICE AGAINST THEM before they are done.

If that is what happened here, it means Aschenbrenner is quietly accumulating something significant and does not want the market to see it yet.

The 24 year old who turned $225 million into $5.5 billion in 12 months going dark on the one day he was legally required to show his hand is not nothing.

Pay attention to what happens when this position finally becomes public.

We are checking every day, and when it comes, we’ll share it here publicly.

Turn on notifications so you don’t miss the signal, this is VERY important.

Many people will wish they followed us sooner.

Miletus Research covered $SLNH this week via @SeekingAlpha

The numbers from 2025: operating capacity doubled, cash grew from $10.5M to $88.8M, pipeline expanded 54% to 4.3 GW, power cost at $34/MWh.

The argument: trailing revenue doesn't capture what the pipeline represents.

Full analysis: https://t.co/vKo4rDWxSX

My theory on $SLNH price action:

Lately it feels like the same pattern keeps repeating. Weakness during the middle of the day, then a strong push back into the close.

Could be nothing. But with the $500M ATM filed in March, I wonder if the company has been using this momentum to raise capital into strength.

Some people will see that as a red flag. I get it.

But for an early infrastructure company, dilution is often part of the playbook. If management is raising into momentum and using that capital to fund projects, close deals, and accelerate growth, that money can become fuel for the next leg of the story.

The interesting part is timing. We likely won’t know how much was issued until future filings, which means the market has room to speculate before the full picture is clear.

Not saying this is definitely what’s happening. But if $SLNH is running like this while absorbing ATM pressure, imagine what the stock could do once that pressure eases.

Speculative. Risky. But the setup is getting very interesting. @jbelizaireCEO@McnallieM

My theory on $SLNH price action:

Lately it feels like the same pattern keeps repeating. Weakness during the middle of the day, then a strong push back into the close.

Could be nothing. But with the $500M ATM filed in March, I wonder if the company has been using this momentum to raise capital into strength.

Some people will see that as a red flag. I get it.

But for an early infrastructure company, dilution is often part of the playbook. If management is raising into momentum and using that capital to fund projects, close deals, and accelerate growth, that money can become fuel for the next leg of the story.

The interesting part is timing. We likely won’t know how much was issued until future filings, which means the market has room to speculate before the full picture is clear.

Not saying this is definitely what’s happening. But if $SLNH is running like this while absorbing ATM pressure, imagine what the stock could do once that pressure eases.

Speculative. Risky. But the setup is getting very interesting. @jbelizaireCEO@McnallieM