Giving the digital asset industry the commonsense rules it needs to thrive isn't a Republican issue or a Democrat issue. It's an American competitiveness issue. Pass the Clarity Act.

My beliefs: Retweets are notifications, not endorsements. Constructive dialogue leads to better outcomes. Bitcoin is hope and economic empowerment for everyone. Every good-faith effort to strengthen the network should be welcomed.

Saturn Credit (@saturn_credit) is quietly building one of the cleanest structured yield products in DeFi right now. Here are the 3 core investment theses that stand out. No hype — just the financial logic

Superior Risk Management via Real Structured Tranches

Saturn uses classic senior/junior tranching onchain. The junior tranche absorbs first-loss capital, protecting srUSDat. When $STRC recently traded below par (~92), the junior buffer took the hit while senior holders kept accruing yield uninterrupted. This is the resilience Luna’s algo peg and Ethena’s synthetic never had

Real Dividend Yield Backed by Bitcoin Credit

Yield on sUSDat comes from actual STRC dividends — preferred equity backed by Strategy’s Bitcoin treasury (3x BTC coverage, large cash buffer). Unlike Ethena’s funding-rate yield that can flip negative, this is contractual cash flow from a high-quality credit instrument

Dual-Token Model + Explosive Product-Market Fit

USDat = 100% Treasury-backed stable for liquidity, payments and collateral

sUSDat = staked version that captures STRC yield

Clean separation, no complex looping needed. Result: $245M TVL in just 6 weeks, strong integrations (Chainlink, Pendle, M0, Strata) and top-tier backers

Saturn isn’t another algo experiment or funding-rate casino. It’s the first credible onchain structured digital credit layer — real RWA backing, TradFi risk tranching, and Bitcoin-native yield in one clean package

We have acquired 16,055,121 satoshis for ~ $10,000 at ~$61,920 per Bitcoin in our forty-sixth consecutive weekly purchase. As of 6/9/2026, we HODL 1,492,732,441 satoshis acquired for ~$1,260,000 at an average price of ~$84,409 per Bitcoin.

https://t.co/I22NO0wiXw

盤石なバランスシートは、私たちにできることを大きく変えます。40,177 BTC、自己資本比率85%超、低水準の負債。メタプラネットは、アジア最大、そして世界第3位のビットコイン・トレジャリー企業です。この基盤は、守りに入るためのものではありません。次の成長を築くための土台です。すでにビットコイン・インカム事業は大きな収益を生み出して��り、これから私たちが構築していくすべての礎となります。

A fortress balance sheet changes what’s possible. 40,177 BTC, equity ratio above 85%, low debt. Metaplanet is the largest Bitcoin treasury in Asia, and the third largest in the world. A base like this isn’t built to sit still. It already produces significant revenue through our Bitcoin Income Generation business, and it’s the foundation for everything we build from here.

Late night stacking session. Busy day, but the orange dot never sleeps. 🟠

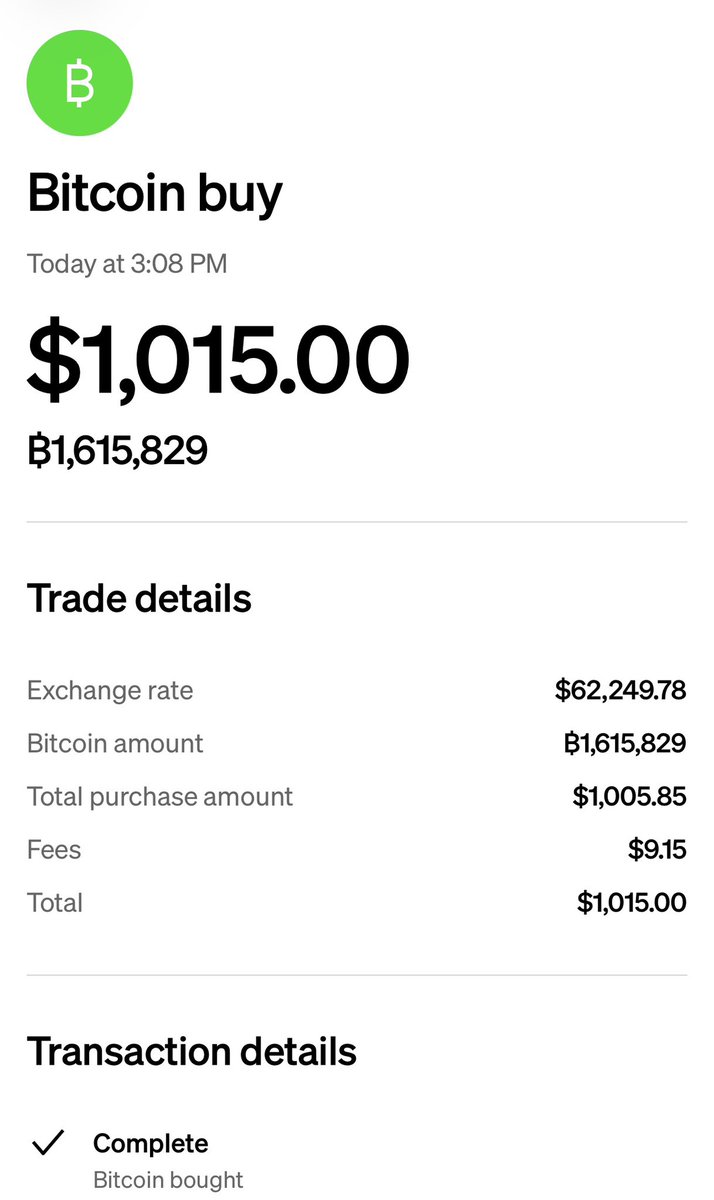

0.005 BTC purchased for $308.91 USD at $61,782.

This is purchase #89 of my HodlHabit DCA fund.

Total stack: ₿0.7434 ($45,673 USD). Fund is currently -17.38% ($9,605 loss).

Another dot on the chart, another step closer to that whole coin. More stacking tomorrow! See you then, orange army!

@mattkratter BTC Yield measures the increase in BTC per share, not total shareholder accretion. Last week Strategy added ₿1,550 of BTC and $100 million of USD Reserve. When both assets are included, the transaction was accretive to MSTR shareholders.

The document you cite clearly states that BTC Yield is a narrow KPI used to assess per-share accretion solely as it pertains to bitcoin holdings. It is not a measure of financial performance, valuation, liquidity, ROI, book value, or stockholder return. Full financial analysis requires a more comprehensive review of our financial statements and SEC disclosures.