@tyler@Gemini Sure, Bitcoin was first - but calling it a Strategic Reserve is like insisting that your old Nokia 3310 is the future of smartphones. XRP, SOL, and ADA may not be your Rolls-Royce, but at least they’re not running on Stone Age engines.

It’s official: Ripple has received its EU CASP license. We are now fully MiCA-compliant and ready to meet growing European crypto demand https://t.co/I9GRgvfGzH

🔥NEW: RIPPLE'S BRAD GARLINGHOUSE GOES OFF ON JP MORGAN-CHASE CEO

"Jamie Dimon has been dismissing this industry for a DECADE. He’s called it a Ponzi scheme, he’s called Bitcoin a pet rock.”

"JP Morgan generates $20 BILLION of revenue from their payments business.. So its clear he is trying keep them extremely profitable”

"He did a DISSERVICE when representing that Clarity Act makes it easier to do bad things. And that’s just not true"

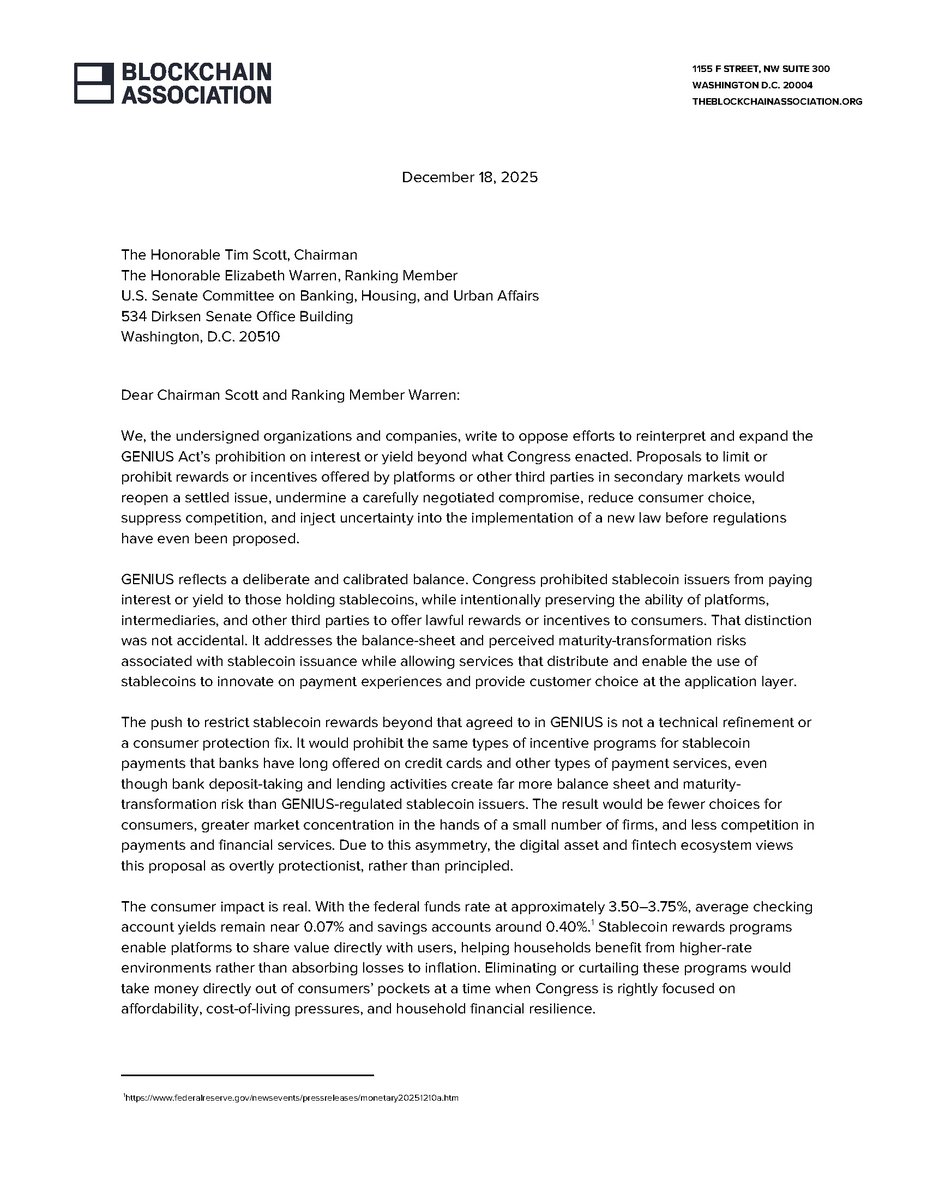

Banks earn 4.4% on reserves parked at the Fed...

They pay you 0.01% on your savings account.

And now they're lobbying Congress to make sure stablecoins can't offer you anything better.

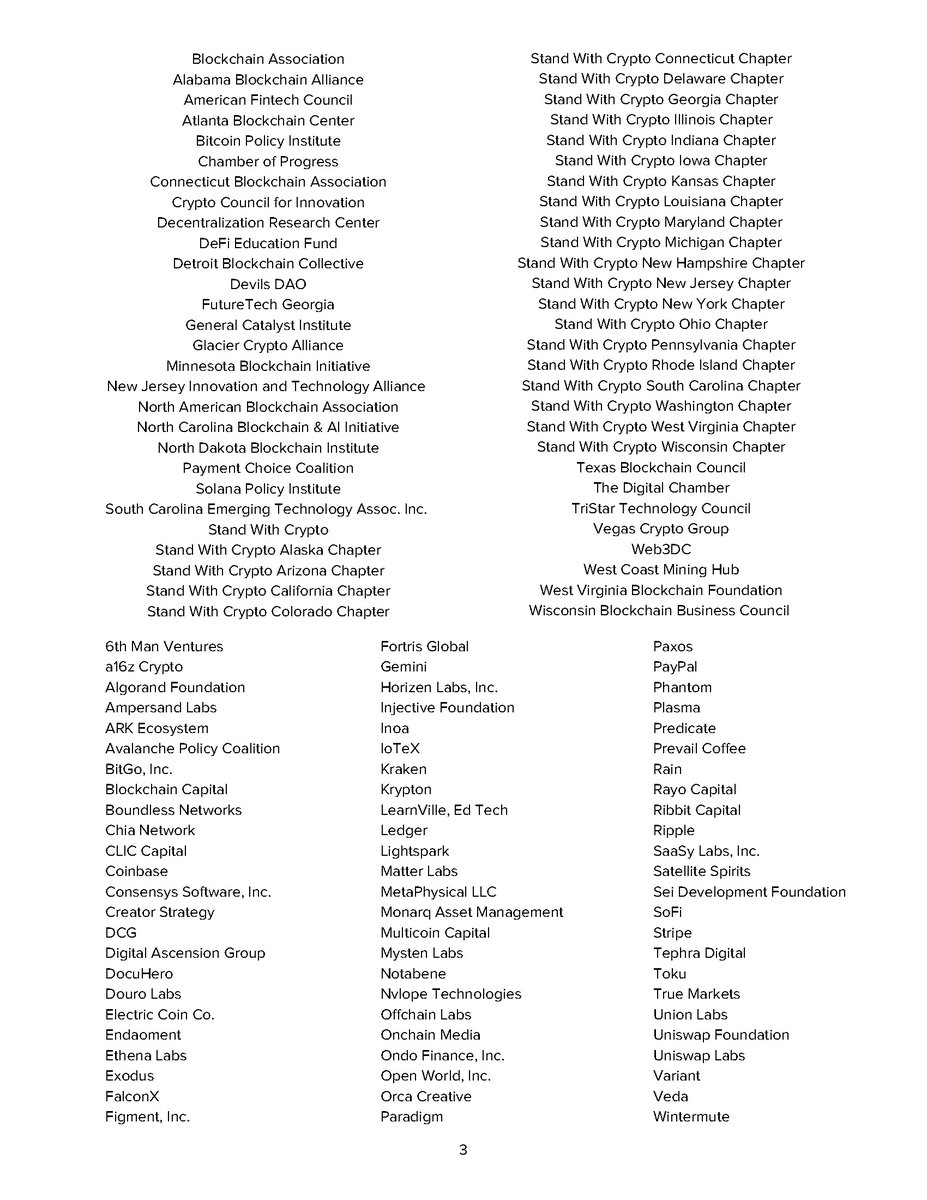

The GENIUS Act already settled this. Congress spent months hashing out a compromise. Stablecoin issuers can't pay interest directly, but platforms and third parties can offer rewards. Done. Finished. Everyone shook hands.

That was a few months ago.

Now the banking lobby wants to reopen it. They're calling it a "safety concern." They're worried about "community bank deposits."

Independent research shows zero evidence of disproportionate deposit outflows from community banks. Meanwhile, the big banks are sitting on trillions in reserves, collecting interest from the Fed, passing almost none of it to customers.

How this plays out for the most part is that your bank takes your deposit, parks it at the Federal Reserve, earns 4%+ on it, gives you basically nothing. A stablecoin platform wants to share some yield with you and suddenly that's a threat to financial stability?

We saw three different lobbying pushes on this bill in the last year & every single time, the framing is consumer protection, but in reality, every single time, the actual effect would be protecting big banks and incumbent margins.

What you should actually watch for:

-Any amendment that bans "rewards" broadly rather than just direct interest payments from issuers.

-Whether the same legislators worried about stablecoin yields have ever questioned why bank savings rates haven't moved in fifteen years.

-Who's funding the "community bank protection" messaging (Usually not community banks lol)

If Congress caves on this, it sets a (not good) pattern. Pass a framework, let the incumbents lobby it back open, chip away until the new entrants can't compete, and crypto companies aren't the only ones watching. Every fintech considering U.S. markets is taking notes on whether legislation here actually sticks.

We signed on to this letter to show our support and conviction in moving the industry forward in the United States. The next six months will show whether the U.S. wants competitive payments infrastructure or protected banking margins under the guise of "stability"

as always, thanks to @BlockchainAssn for their hard work in the industry alongside @standwithcrypto & @na_blockchain

special shoutout to @TBC_Jessi@512mace & @wadepreston for pushing this along as well

Not entirely true. ESC2 relies on the attacker being able to manipulate the certificate identity.

If the Subject Name is AD-controlled, Supply in the request is disabled, and only machine/low-privileged objects can Enroll, the attacker can only obtain a cert for their own object.

They can’t impersonate other accounts, request admin certs, or leverage “Any Purpose” EKU for privilege escalation.

In that configuration, ESC2 is effectively neutralized.

If SEC itself no longer treats #XRP under the old "security" lens (dropping 19b-4), why should #Ripple remain stuck with an S-1 straitjacket?

Precedent is only as strong as the policy it’s built on.

SEC just shifted #XRP into generic ETF standards, a move likely nudged by the Trump era’s policy tilt.

Yet Ripple is still bound by a judge’s S-1 requirement based on SEC’s old stance.

If the regulator rewrites the rules, shouldn’t the ruling be revisited? ⚖️

Logic > legacy. Paradigm shift in motion.

at risk of angering a few maxis, i will say that i believe $MSTR may be on its last legs.

in a week where $BTC broke ATHs, $MSTR is down ~20% from its highs.

for a company that claims to provide leveraged bitcoin exposure, this is exactly what @strategy investors don't want to see.

if this price divergence continues (which looks likely), investors will no longer buy microstrategy stock and the new money that @saylor relies on to continue buying bitcoin will stop flowing in. fast.

unlike when saylor began his "strategy", there are now several safer ways for investors to get bitcoin exposure (eg ETFs, buying directly on Coinbase / Robinhood etc).

if i were an investor in @strategy, i would monitor this situation very closely.

nfa.

RIPPLE

In a world where financial infrastructure hasn’t kept pace with the digital age, we set out to modernize global value exchange.

By building a real-time, borderless system for money movement - an Internet of Value - we challenge legacy systems and unlock new efficiencies.

But innovation meets resistance. As our technology scales, we stay committed to growth with trust, transparency, and global collaboration - redefining not just payments, but the very fabric of how value moves in a digital world.