I’m joining @USDai_Official as Growth Lead.

Since my wife’s stroke in May, I’ve been in a holding pattern; focused on family, helping her recover, and spending a lot of time researching for @leviathan_news.

A month ago I stumbled on https://t.co/4T3U9aCdLN. At first it looked like “just another stablecoin.”

Then I interviewed @0xZergs.

Halfway through, it clicked. The vision was waaay bigger than I realized.

https://t.co/4T3U9aCdLN is building @aave for GPUs, a fully on-chain loan book for off-chain collateral.

It’s a new way to finance the AI infrastructure boom using the best of DeFi and stablecoins.

I spoke with one of their customers, Kai Golden of @get_hydrahost. He confirmed everything in this quote from the video below:

" there is so much legal bullshit that is done over and over in this industry and paid for redundantly over and over in this industry that using USDAI allows you to just completely bulldoze through."

After that, I met with @0xZergs and @_ConorMoore in person. I pitched myself to join the team. And today, I’m officially starting.

I feel lucky to be working on this. https://t.co/4T3U9aCdLN is building the future of onchain GPU financing, better, faster, and more transparent than anything on the market today. It's a true innovation.

Here’s the video I made that started it all:

He's talking about the GPU's specifically.

JPM will finance the land, shell, utilities, but they will not fund the chips. Private Credit can and is funding massive GPU purchases, but the long tail of neoclouds cannot find decent funding. If you are sub-billion its extremely difficult finding financing.

the current dynamic is simple:

☁️long neoclouds, short crypto

🏭 crypto miners becoming AI token factories

🪙 long token factories, short crypto tokens

margin traders, vol hunters, and momentum chasers have exited crypto for compute, this will only accelerate IMO

A new record loan size for USDAI.

$98.1M facility.

288 NVIDIA B300 servers, 2,304 GPUs.

12% APR.

3-year term.

$84.1M is now escrowed and earning 7% until the GPUs are installed and online.

@VechainWhale Nothing is wrong with the contracts.

sUSDai maintains separate share prices for deposits and redemptions.

The front end was showing the deposit share price for withdrawals, but the actual realized price was the redemption price.

Will have an article about it soon.

A mistake I see over and over is conflating backing with reserves. Backing ≠ reserves.

Reserves are for managing liquidity. A fully reserved stablecoin or bank can meet 100% of possible withdrawal requests within a few days.

In practice, I think the Reservoir unwinding half a year ago is one of the only times I’ve seen a stablecoin unwind ~100% as designed.

So being fully reserved is typically seen as overkill, and usually it exists mainly to remove the temptation of an asset issuer to accept low-quality backing. You can’t engage in bad underwriting if you don’t engage in any underwriting at all.

Backing is what determines solvency. The assets may be worth a given dollar amount, but be illiquid, making them unsuitable as reserves. Real estate is a good example.

Giving out a secured loan is another. The loan may very well be worth a given sum of money, but unless that loan is very short term (e.g. repo) or you have a way to put the loan to a solid counterparty, it’s not really a reserve asset.

It should be obvious to readers at this point that fractional reserve lenders are not in any way insolvent by definition (it depends upon whether they make good loans), although they are less liquid by definition.

Crypto has an obsession with liquidity - as a lender or depositor, more liquid is always better than less - but liquidity isn’t everything.

Moral of the story is: journalists and analysts please stop calling all backing assets for a stablecoin “reserves”

The best DeFi yields are outside of crypto.

The most interesting opportunities I'm seeing aren't loops or points farming. They're protocols using DeFi capital to finance real businesses.

If you're sitting in USDT, you're already financing US government debt. But you take nothing.

A few examples other examples:

> @USDai_Official is financing the AI economy. Yields are competitive because the sector is growing quickly and the demand is there.

> @3janexyz is providing liquidity to LendSwift, a short-term consumer lending company. Similar model as Klarna.

Klarna became one of the fastest-growing fintechs ever because it needed constant fresh capital to keep extending credit to new users. That's what 3jane is underwriting on-chain.

Then there's what my colleagues @0xBobdbldr and @Wajahat are building, which goes even further; industries where traditional finance has never really shown up.

Can't say more yet, but this could be huge 🚀

We run this exact setup just at smaller scale for GPU operators.

It’s an opco/propco relationship. Valor holds the title cause in case of liquidation or default it makes it easier to seize.

There’s nothing extraordinary about this deal and I’m happy to walk you through how these deals work.

Who owns the assets isn’t important, it’s who is the offtake providing the revenue for the compute

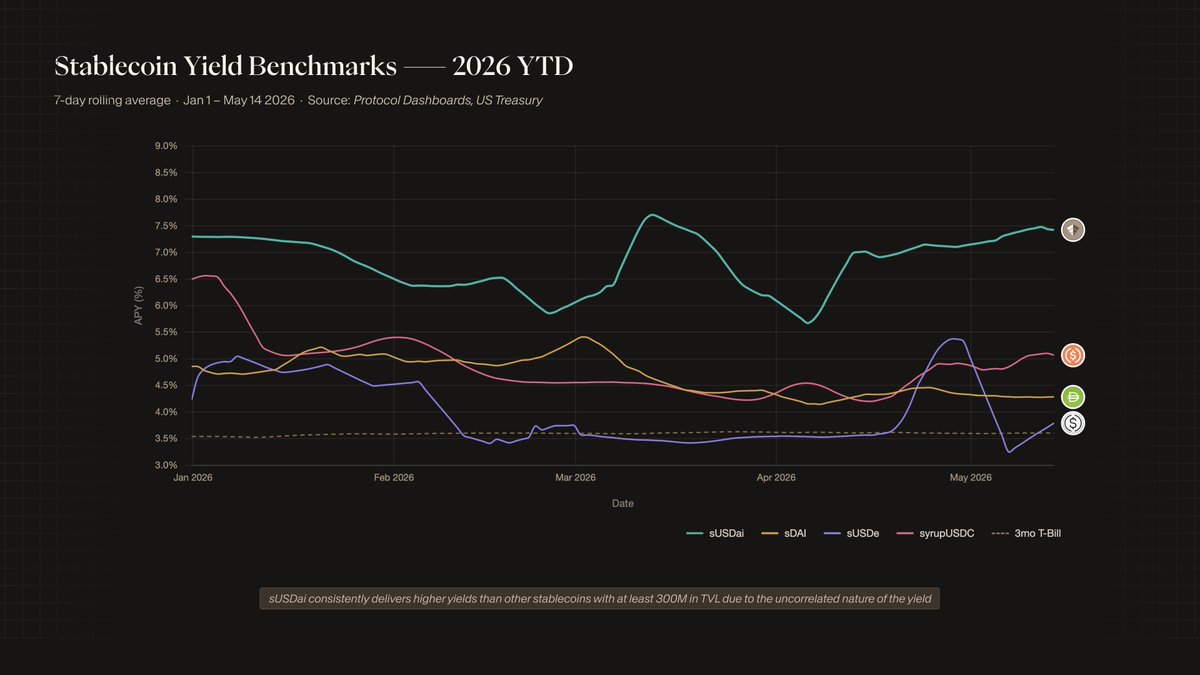

sUSDai has delivered the strongest and most consistent yield among tracked stablecoin benchmarks throughout 2026.

Yield can compress when collateral exits the protocol, but has recovered quickly above 7% as capital stabilizes and new loans are originated.

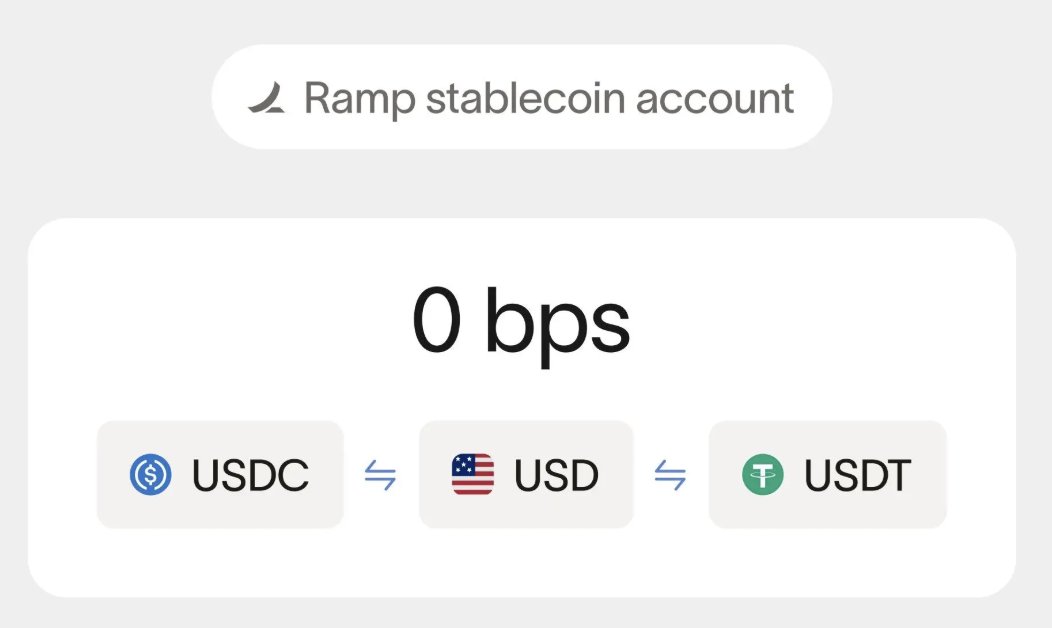

Of all the stablecoin features we've built at Ramp over the past few months - letting businesses convert 1:1 between USD, USDC, and USDT has by far been the most positively received one.

My personal view is that this is table stakes for any kind of B2B remittance, treasury, or bill pay product - and that we'll soon see this as the status quo.

Businesses shouldn't have to worry about how much USDC will ultimately land in their account when they get paid - or need to send 10,001.13 USDC so that their vendor will gets paid exactly 10,000 USDT.

A dollar is a dollar.