THIS IS EITHER THE NEXT INTERNET BOOM OR THE BIGGEST TECH BUBBLE EVER.

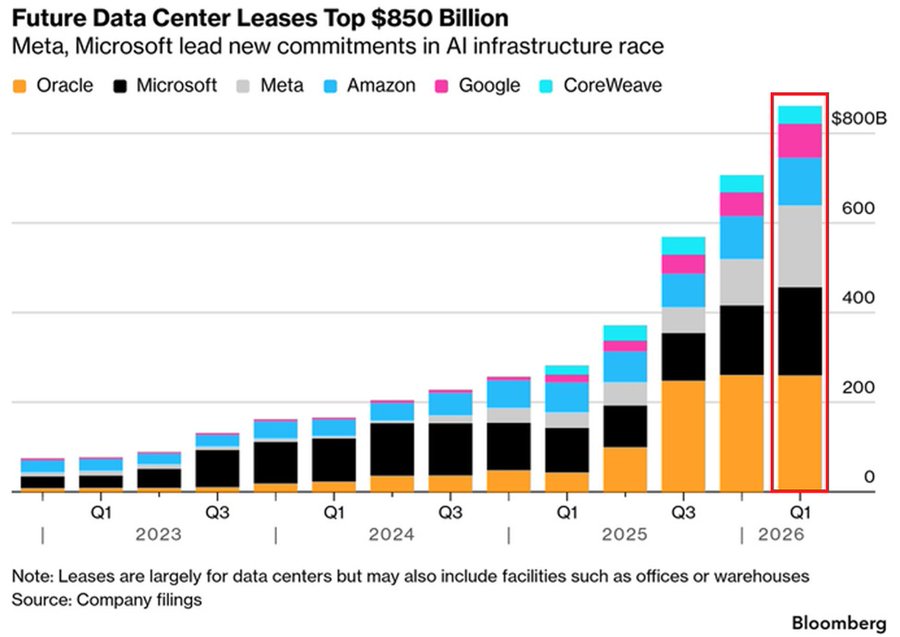

US tech companies just committed $850 billion to data center leases, a 204% increase year over year and a 31% jump in a single quarter.

Oracle leads with $250 billion in total commitments, largely to fulfill its contract with OpenAI.

Microsoft sits at $197 billion.

Meta added $79 billion in Q1 2026 alone, a 76% quarterly jump, bringing its total to $183 billion.

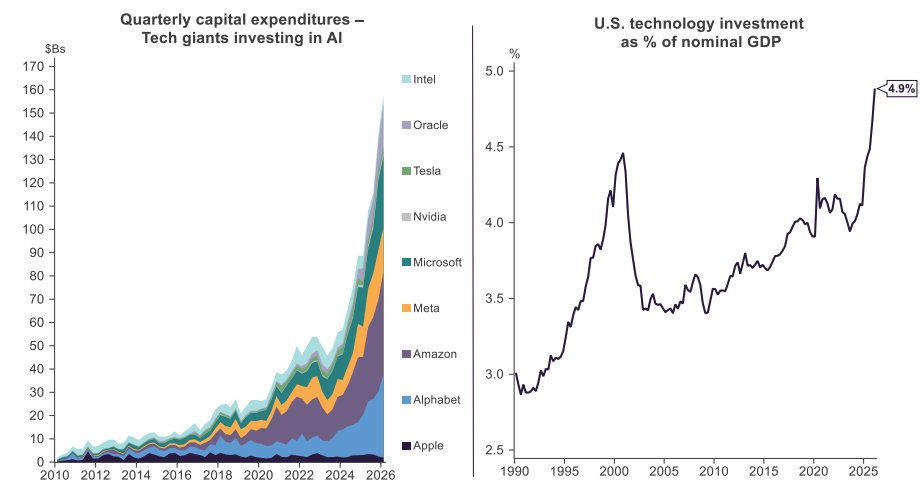

Most of this money hasn't been spent yet.

The chips haven't been installed. The facilities haven't been built. The electricity hasn't been contracted.

This is forward commitment.

$850 billion in lease commitments with no clear revenue model to match it is either visionary or reckless.

John Authers: Investment bubbles sow the seeds of their own destruction if they attract more capital than they can productively use, and starve other areas that need it.

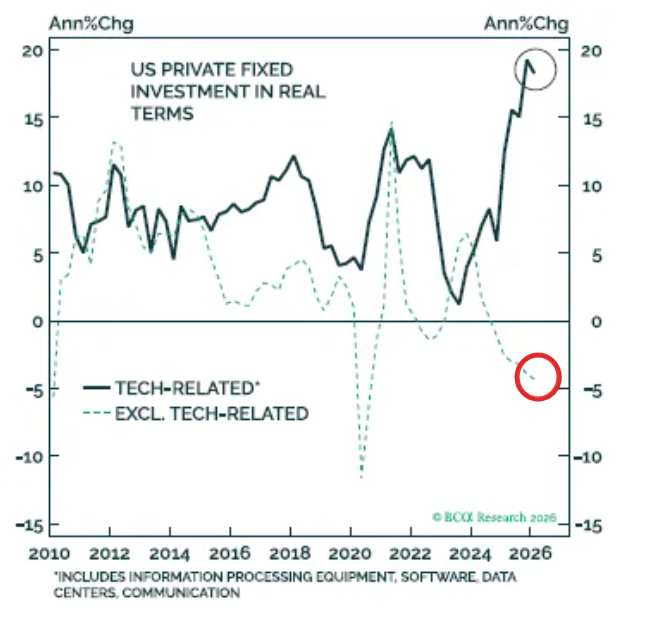

That point might be approaching. Arthur Budaghyan of BCA Research argues that capital expenditures are overshooting. In the US, he points out, capex on everything other than tech is actually falling.

Foreign investors now hold 62% of their US financial assets in equities. The highest allocation in 70 years of data.

Higher than 2000, when the number peaked at 53% and the Nasdaq lost 78%.

Foreigners were at 25% in 1974. 25% in 2009. Both generational bottoms. Nobody wanted US stocks at the exact moment US stocks were the trade of a lifetime.

Now everyone on earth is all in. At all-time highs. In the most concentrated market since 1929.

Is it really a good idea when the whole world is long US assets to the tits?

Asking for a friend.

This chart covers 225 years of the S&P 500, adjusted for inflation.

Every crisis you were taught to fear is on it. Look how small they are.

The Napoleonic wars took markets down for 12 years. On the chart: a dent. The Civil War: 5 years down. A wiggle. Post-WWI inflation, 11 years. The oil shock and Vietnam, 13 years. Each one felt like the end of the world to the people living through it. Each one is now a footnote on a rising line.

Three lessons from two centuries:

– The market spent roughly a quarter of the last 225 years going nowhere. Investors who quit during those stretches missed everything that followed.

– The worst drawdowns came from wars and inflation, not valuations. What kills a generation of returns is rarely what investors are watching.

– Every secular bear market had a start date and an end date. Nobody living through one knew either.

Your investing life is maybe 50 years. This chart contains four and a half of those lifetimes. In every single one, the patient owner of American businesses came out ahead.

The hard part was never finding the right chart. It was staying in it.

@BenBajarin You haven’t met me. I know how it is being deployed and its limitations. It is a great technology. Doesn’t make it a good investment for those building it. Indeed consumers of fibre optic cable benefited from reckless over investment. Ai will be the same.

@ThierryBorgeat Classic hindsight bias. Including the prior 100 years the conclusions changes. Including returns from all global markets.

The starting point is very different - us is not an emerging powerhouse. It is in decline and will be overtaken by china.

For the record.

The Market Has Already Moved On

A leadership change is already

underway, but most investors are still clinging to the last trade. Everyone is crowded into semiconductors and memory, propped up by passive flows and a sell-side still extrapolating an era of outsized earnings surprises that is now behind us. The big earnings revision cycle in semiconductors and AI power is over.

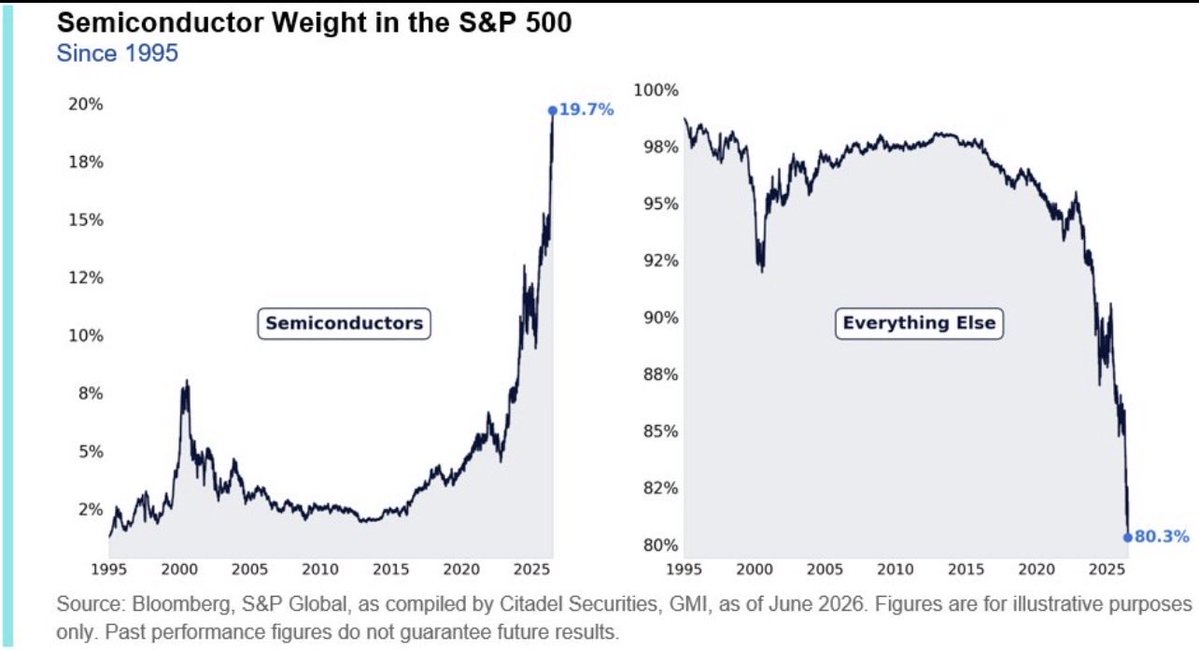

The bottleneck trade is crowded and over-owned, and that playbook is exhausted. Semis now represent 20% of the S&P 500. A period of digestion is needed.

The market is broadening. Beneath the surface, the median stock is delivering double-digit earnings growth, with second-quarter earnings tracking toward 25% year-over-year. This is a rolling recovery, not a narrow AI story.

The AI cycle is not over, but it is evolving. Hyperscalers may be near a bottom and are beginning to convert capex into revenue, extending the cycle. But the bottleneck trade, owning semiconductors and AI Power, is no longer sufficient.

The era of massive upside earnings surprises is over IMHO

These stocks are crowded, expectations are elevated, and future earnings beats are unlikely to surprise as they have.

Leadership is rotating. Equal-weight indices, small caps, and domestic cyclicals are gaining traction, supported by improving earnings and still-muted positioning. Policy is reinforcing the shift, with a more Hamiltonian focus on domestic investment and productive capital.

Liquidity is also changing. Credit creation is moving from the Fed to the private sector, with bank deregulation playing a key role.

This is a more selective regime.

Investors can wait, or adapt. The market has already decided.

@ThierryBorgeat 1920s was Vibe Investing. 2020s is Vibe Investing. 1930s was depression and the rise of extreme politics. The political fallout of what is coming scares me.

@sophie_devil_r@FT the answer to this question should be known before $2tn is spent. The spend was committed in hope - we no longer talk about AGI and only on a small subset of the original promise. 1GW of compute has doubled in price thanks to memory and there is no reutrn being made

@FT The end of the era of Vibe Investing is near - get out now unless you really know what you are doing. The political fallout from this is going to be fascinating but also poses the biggest risk to the US's next 100 years. A big swing to the left is likely.

@DemzDeliver Space X holders - just remember how emphatic Musk was on DOGE and what he could achieve - history will repeat itself with Space X - on par with behaviour in the South Sea Bubble

@ThierryBorgeat We will know this one is over when Bitcoin is <$20k - Crypto started the excesses in the market, NFCs followed, meme stocks/SPACs next wave - AI and Semis the final wave. All speak to the approach of retail - Vibe Investing with now regard for fundamental work

The Nasdaq fell 78% from 2000 to 2002. But that's not how anyone experienced it.

They experienced this:

– A 35% rally. Then new lows.

– A 12% rally. Then new lows.

– A 25% rally. Then new lows.

– A 41% rally. Then new lows.

– A 45% rally. Then the bottom, 30 months after the top.

Five times the market screamed "it's over." Five times it lied.

Former colleagues of mine lived through it on a trading floor. They told me what the routine became: by Thursday, you started praying for Friday afternoon. Not for the weekend. For the close. Two days where you couldn't lose money.

Then you walked out of the office with your head down.

That is what a real bear market does. It doesn't scare you out at the bottom. It exhausts you out, one false dawn at a time.

Bear markets don't end when the sellers are done. They end when the buyers are.

@ViktorShvets@PeterBerezinBCA I really struggle with your comment about timing. Investing is making reasoned judgments where the risk v return equation is attractive. Even if you thought it was 50/50 between your two bookends - how can you justify the risk today of being long semis?

The internet is a good example here. We managed to achieve massive growth in internet traffic without having to spend much more on internet infrastructure because the transmission technologies became much better. Why won’t there be similar technological innovations that dramatically lower the cost of producing memory?

@R1bYamnayaW@MartinShkreli When you have SRMC low and demand falls - no oligopoly withstands that. Very similar characteristics to airlines - essentially fixed costs for a given level of capacity - cyclical - largely a commodity. Very low multiple business and capitalising peak earnings is crazy.